Equipment Appraisal Review vs Second Opinion: Key Differences Explained

The main difference between an equipment appraisal review and a second opinion is that an appraisal review analyzes an existing report for accuracy, methodology, and USPAP compliance, while a second opinion produces a new independent valuation. Reviews validate or challenge a report, while second opinions establish a separate value conclusion.

An appraisal review is a formal USPAP-governed assignment that evaluates an existing report’s credibility. A second opinion is a new, independent appraisal developed from scratch. The two produce different work products, follow different standards, and serve different purposes in lending, litigation, and equipment transactions.

Keep reading because ordering the wrong one can undermine the decision it was meant to support…

What an Appraisal Review Is

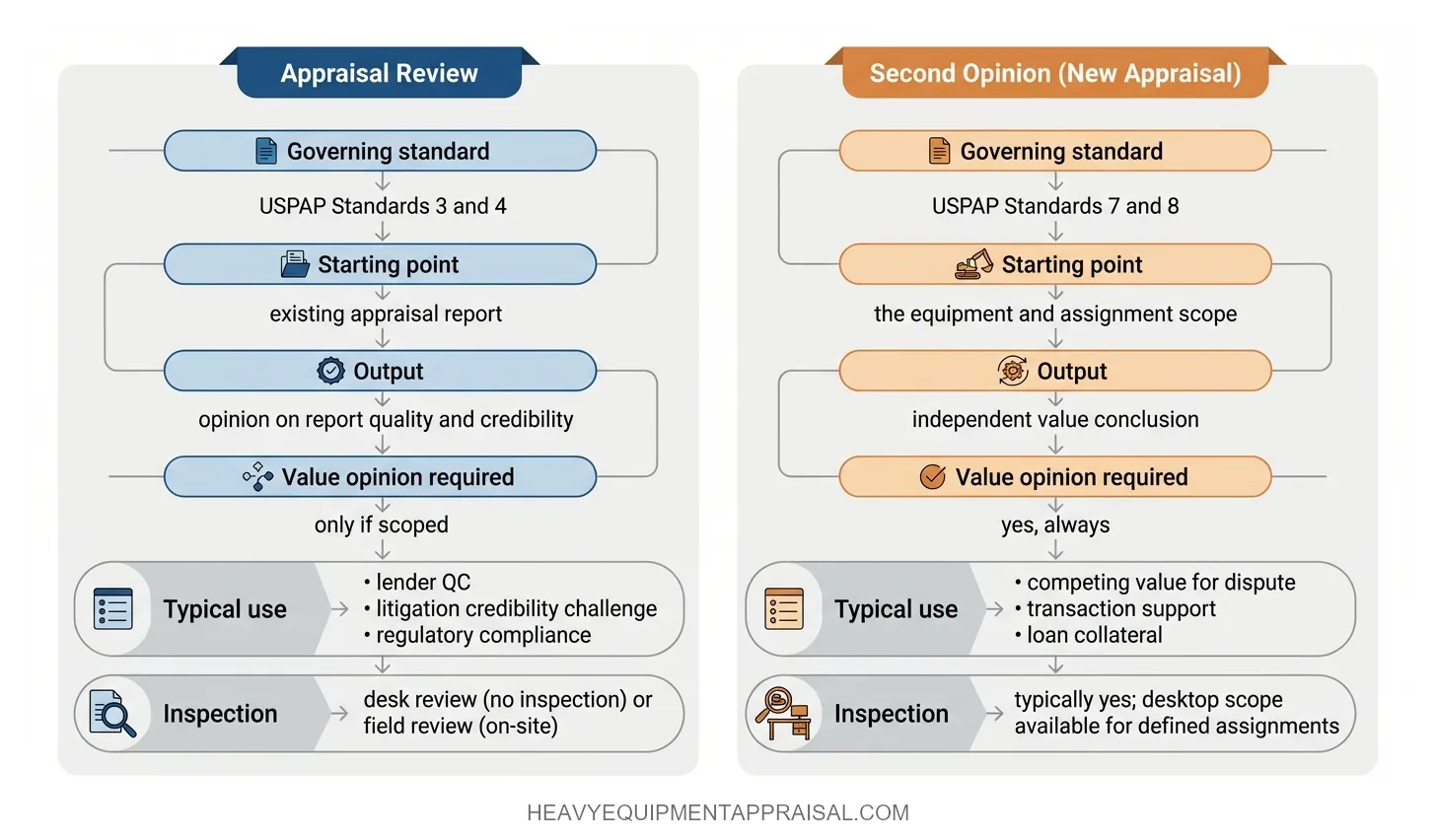

An appraisal review is a USPAP Standard 3 assignment in which a qualified reviewer evaluates whether an existing appraisal report is credible, adequate in scope, and compliant with applicable standards.

The reviewer does not start from scratch. The reviewer examines the original appraiser’s work product: the data selected, the methodology applied, the reasoning documented, and the conclusions reached. The central question is whether the original report supports its own value conclusion, not whether the reviewer would have arrived at a different number.

The reviewer’s role is evaluative, not duplicative. A reviewing appraiser assesses whether the original report meets the requirements of USPAP Standards 7 and 8 for personal property, whether the value type selected matches the assignment’s intended use, and whether the analysis contains errors, unsupported assumptions, or material omissions.

The reviewer may develop their own opinion of value as part of the scope of work, but this is not required. Many review assignments are scoped to address credibility and compliance only.

Two formats exist under Standard 3:

A desk review evaluates the report based solely on the written document and available market data, with no independent inspection of the equipment. A field review adds an on-site component: the reviewer inspects the equipment to verify the original appraiser’s descriptions, condition assessments, and photographs. Field reviews carry more weight in disputes because they independently confirm physical facts that a desk review must take at face value.

Lenders order appraisal reviews when internal quality controls flag a report or when a borrower challenges a collateral value. Attorneys in litigation use them to test the credibility of an opposing expert’s appraisal. Regulatory bodies and auditors may require them as part of compliance oversight.

In each case, the review is the appropriate tool when the question is “Was this appraisal done correctly?” rather than “What is the equipment actually worth?”

That distinction determines whether the resulting work product can resolve the dispute or whether a full independent appraisal is needed instead.

What a Second Opinion Is

A second opinion is a new, independent appraisal assignment in which a separate equipment appraiser develops their own value conclusion from scratch.

The second appraiser does not critique, reference, or build upon the first report. They conduct their own inspection (or desktop analysis, depending on the agreed scope), gather their own comparable data, apply their own methodology, and produce a standalone report governed by USPAP Standards 7 and 8 for personal property. The result is a complete appraisal, not a commentary on someone else’s work.

The distinction from a review is structural:

A reviewing appraiser evaluates an existing report’s credibility. A second-opinion appraiser ignores the existing report entirely. They define the appropriate value type based on the assignment’s intended use, select their own cost, sales comparison, or income approach, and document their reasoning independently. The first appraisal may not even be disclosed to the second appraiser, and best practice in litigation often requires that it is not, to preserve independence.

Two competent appraisers working the same assignment can legitimately reach different value conclusions.

Differences arise from the comparable sales selected, the condition adjustments applied, the depreciation estimates used, or the weight given to each approach. A 10–15% variance between two defensible equipment appraisals is not unusual, particularly for specialized or low-transaction-volume assets like custom fabrication lines or older marine equipment.

Neither report is automatically wrong.

The question is whether each appraiser’s reasoning and data adequately support their conclusion under the standards that govern the appraisal process.

Business owners and attorneys order second opinions when they believe the original value conclusion is too low or too high but need an independent number rather than a critique. A second appraisal produces a value that can stand on its own in court, in a negotiation, or in front of a lender, giving the party a competing data point with full USPAP-compliant documentation behind it.

How the Two Differ in Practice

The core structural difference is the starting point: a review begins with an existing report, while a second opinion begins with the equipment itself.

| Dimension | Appraisal Review | Second Opinion (New Appraisal) |

|---|---|---|

| Governing standard | USPAP Standards 3 and 4 | USPAP Standards 7 and 8 |

| Starting point | The original appraisal report | The equipment and assignment scope |

| Output | Opinion on report quality and credibility | Independent value conclusion |

| Value opinion required? | Only if included in the scope of work | Yes, always |

| Typical use case | Lender QC, litigation credibility challenge, regulatory compliance | Dispute requiring a competing value, transaction support, loan collateral |

| Inspection required? | No (desk review) or yes (field review), depending on scope | Typically yes, though desktop appraisals exist for defined scopes |

The table captures the mechanical differences, but litigation is where the two tools most often work in tandem.

An attorney challenging an opposing expert’s equipment valuation may first order an appraisal review to identify specific deficiencies in the original report:

- Unsupported depreciation assumptions

- Misidentified value type

- Omitted comparable sales data

If the review reveals material problems, the attorney then commissions a second opinion to establish an independent value that can be presented as an alternative.

The review weakens the opposing number. The second appraisal replaces it.

This sequencing matters because each tool carries different evidentiary weight:

- A review alone does not give the requesting party their own value to argue from.

- A second opinion alone does not explain why the original report is flawed.

Used together, they create both the offensive and defensive positions needed in contested proceedings, whether that contest is a divorce settlement involving a fleet of construction equipment, an insurance dispute, or a partnership dissolution.

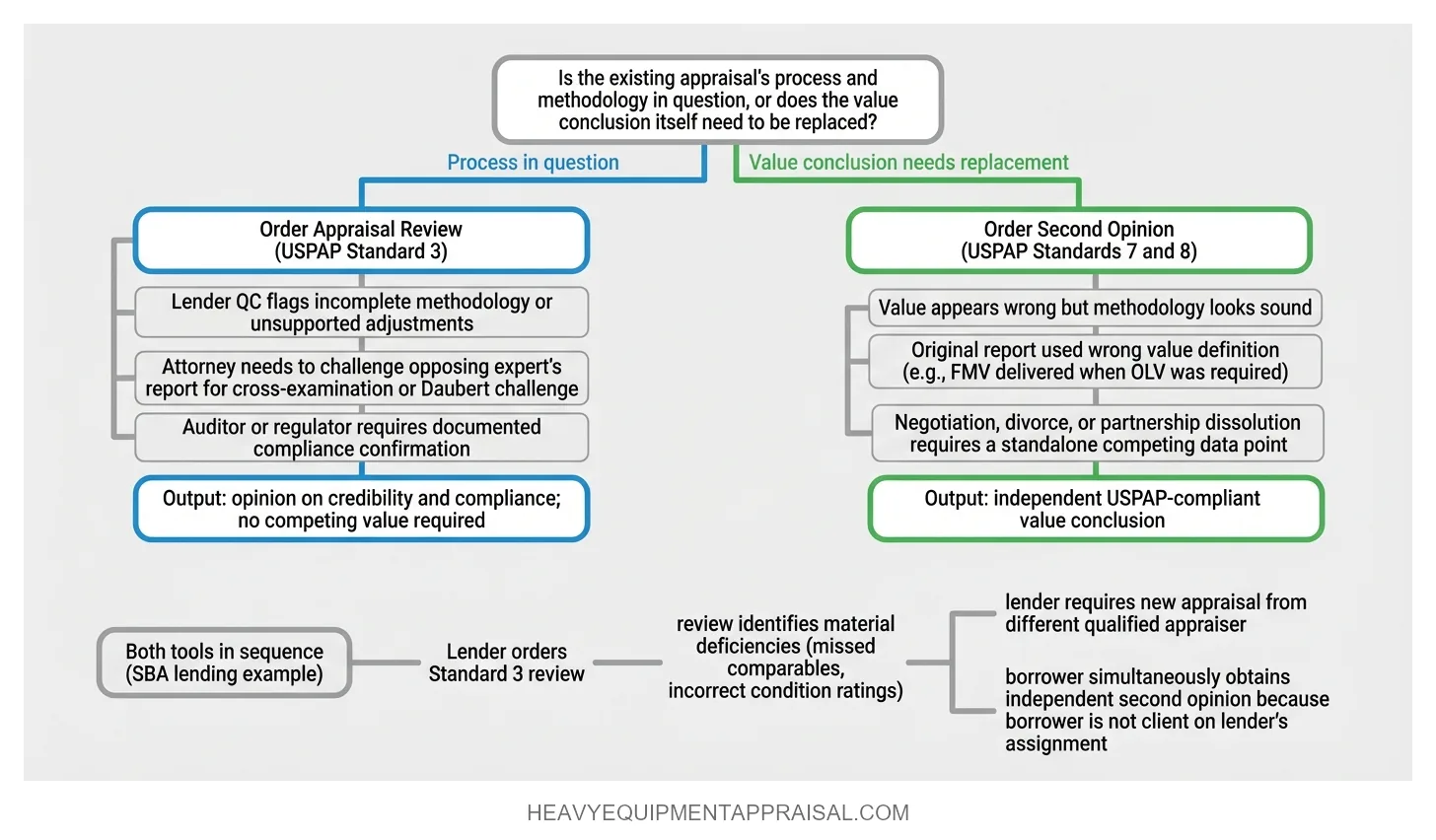

Choosing between them starts with a simple diagnostic: if the existing appraisal’s methodology and compliance are in question, a review addresses that directly. If the conclusion itself needs to be replaced with a defensible alternative, a second opinion is the correct assignment.

Misidentifying which tool the situation requires can leave a party with a work product that answers the wrong question, a gap that opposing counsel or a lender’s underwriting desk will identify quickly.

Which One to Order and When

The deciding factor is whether the existing appraisal’s process is in question or whether its value conclusion needs to be replaced. Each scenario points to a specific tool, and some situations call for both in sequence.

Order an Appraisal Review When

Lender quality control flags a report: Federal banking guidelines, including the FDIC Interagency Appraisal and Evaluation Guidelines, explicitly recognize a USPAP-compliant appraisal review as an acceptable instrument for obtaining a second opinion of market value in lending contexts. When a bank’s internal review process identifies incomplete methodology, missing USPAP compliance elements, or unsupported adjustments, a Standard 3 review documents those deficiencies with regulatory standing.

Litigation requires challenging an opposing expert’s report: An attorney who needs to discredit a valuation presented by the other side starts with a review. The review identifies specific analytical failures (unsupported depreciation, misapplied value type, omitted comparables) that can be raised in cross-examination or a Daubert challenge. The review does not need to produce a competing number to serve this purpose.

Regulatory or audit compliance demands documentation: Auditors, insurance adjusters, and regulatory bodies sometimes require written confirmation that an appraisal meets applicable standards. A review satisfies this requirement without the cost and time of commissioning an entirely new valuation.

Order a Second Opinion When

The value conclusion appears wrong, not the methodology: When an equipment owner believes a fair market value conclusion is too low or an orderly liquidation value too conservative, but the original report appears methodologically sound, a second opinion produces an independent number that can compete on its own merits.

The original appraisal used the wrong value definition: If a lender needed OLV for collateral sizing but the appraiser delivered FMV in continued use, the report answered the wrong question. A review cannot fix a definitional mismatch. A new appraisal scoped to the correct value type is the only remedy.

A negotiation or transaction requires a competing data point: In business sales, partnership dissolutions, or divorce proceedings, each party may commission their own appraisal. The second opinion gives the requesting party a standalone, USPAP-compliant report they can present independently.

SBA Lending Example

A borrower applies for an SBA-backed equipment loan. The lender’s appraiser concludes an OLV of $320,000 on a fleet of wheel loaders and excavators. The borrower believes the value is low.

Under federal lending guidelines, the lender can order a USPAP-compliant review to evaluate the original report’s credibility. If the review identifies material deficiencies (missed comparables, incorrect condition ratings, unsupported depreciation), the lender then requires a new appraisal from a different qualified appraiser. The borrower’s own recourse is to obtain an independent second opinion, because the borrower is not the client on the lender’s appraisal assignment. Both tools may be deployed in the same transaction, each serving a distinct function.

Matching the right instrument to the right question protects the resulting work product’s standing with the specific audience that will rely on it: an underwriter, a judge, or a counterparty across the negotiating table.

Why Two Appraisers Can Reach Different Conclusions Legitimately

Value divergence between two qualified appraisers does not indicate that either one made an error. Equipment appraisal requires professional judgment at multiple decision points, and reasonable practitioners applying sound methodology to the same asset can reach different conclusions. Understanding the sources of that divergence is essential before concluding that an appraisal needs to be challenged through a review or second opinion.

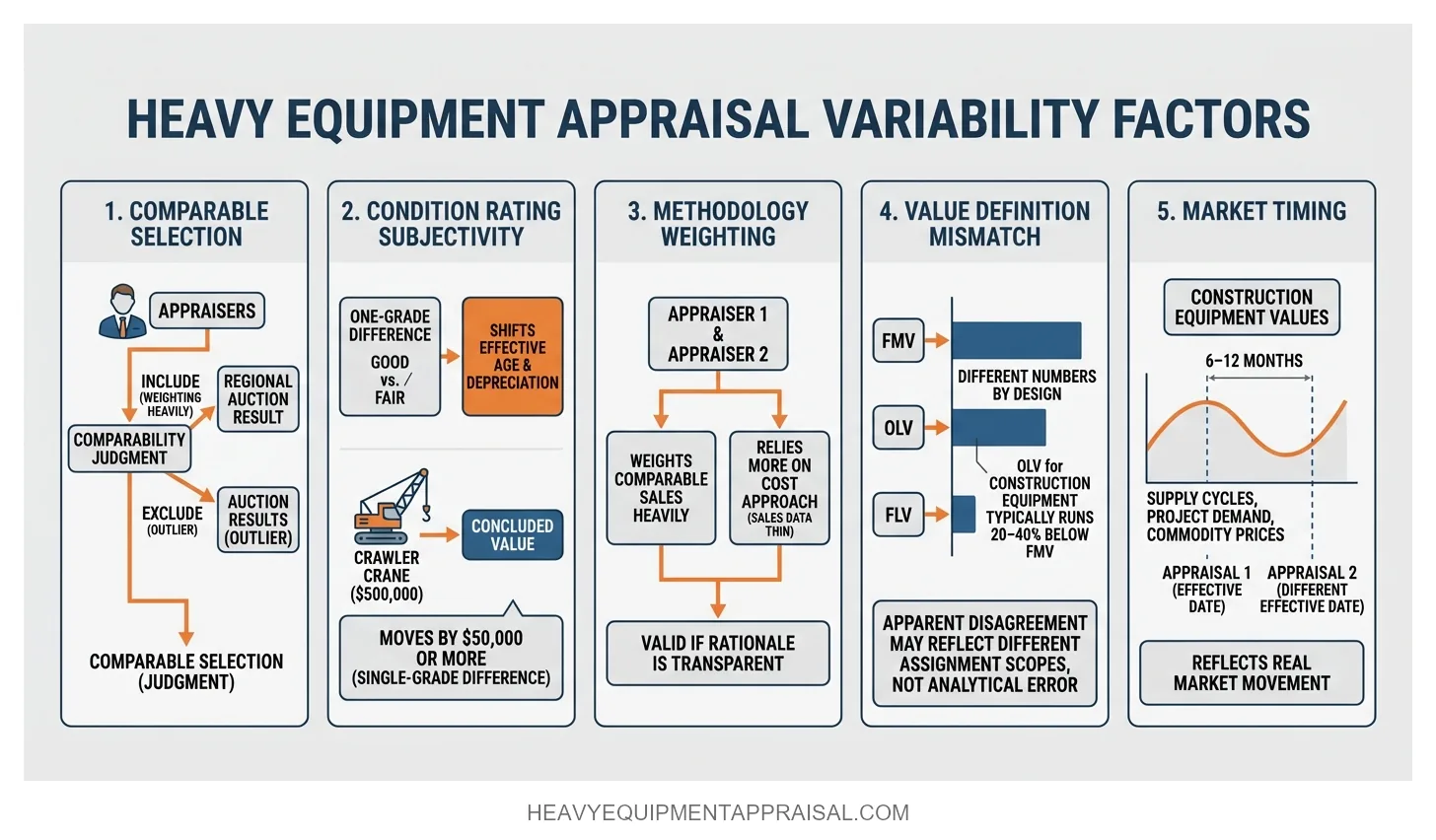

Five factors account for most legitimate disagreement:

Comparable selection. Under the sales comparison approach, two appraisers may include or exclude specific auction results or private sale data based on their judgment about comparability. One appraiser may weight a recent regional auction heavily while another excludes it as an outlier. Neither selection is necessarily wrong if the reasoning is documented and defensible.

Condition rating subjectivity. Assigning a condition grade (Excellent, Good, Fair, Poor) to a specific piece of equipment involves on-site judgment. A difference of one condition grade shifts the effective age calculation, which changes the depreciation percentage applied under the cost approach. On a $500,000 crawler crane, that single-grade difference can move the concluded value by $50,000 or more.

Methodology weighting. When multiple approaches to value are developed, the appraiser must reconcile them into a final conclusion. One appraiser may give primary weight to comparable sales data. Another, finding the sales data thin, may rely more heavily on the cost approach. Both decisions are valid if the rationale is transparent.

Value definition mismatches. This is the most common source of apparent disagreement that is not actually a disagreement at all. FMV, OLV, and FLV produce different numbers for the same asset by design. OLV for construction equipment typically runs 20–40% below FMV. If one appraisal concludes FMV in continued use and the other concludes OLV, the gap reflects the assignment’s scope, not a dispute over the asset’s worth.

Market timing. Construction equipment values can shift materially over 6–12 months depending on supply cycles, project demand, and commodity prices. Two appraisals with different effective dates may reflect real market movement rather than analytical disagreement.

Before ordering a review or commissioning a competing appraisal, checking whether both reports used the same value definition, effective date, and condition methodology eliminates the most frequent sources of perceived error, potentially saving the cost and time of an unnecessary second engagement.

USPAP Standards Governing Each Service

USPAP assigns different standards to appraisal reviews and independent appraisals, and the distinction matters for equipment work because the governing standards differ from those used in real estate.

An appraisal review falls under Standard 3 (development) and Standard 4 (reporting). A new equipment appraisal, including any second opinion, falls under Standard 7 (development) and Standard 8 (reporting). Real property appraisals use Standards 1 and 2, which is why guidance written for the real estate context does not translate directly to machinery and equipment assignments.

Standard 3 requires the reviewing appraiser to identify the report under review, define the scope of the review assignment, and form a professional opinion on the quality and credibility of the original work. The reviewer must also disclose whether they are developing their own opinion of value as part of the engagement.

Standard 7 requires the appraiser developing a second opinion to independently identify the property, define the appropriate value type, select and apply suitable methodology, and produce a report under Standard 8.

These are parallel but separate tracks: one evaluates an existing work product, the other creates a new one.

An informal critique that does not follow Standard 3 carries significantly less evidentiary weight. Without the structured development and reporting requirements of a USPAP-compliant review, the critique is an opinion letter at best. Courts and lenders routinely distinguish between a Standard 3 review and an unstructured letter questioning a value conclusion. The former is an expert work product with defined scope and professional accountability. The latter is not.

The Competency Rule applies to both tracks.

A reviewer must possess the knowledge and experience necessary to complete the review competently for the specific property type. A residential or general commercial appraiser is not qualified to review an appraisal of CNC machining centers or a fleet of hydraulic excavators.

The same rule applies to the appraiser developing a second opinion under Standards 7 and 8. Non-compliance with the Competency Rule exposes the entire work product to challenge, regardless of whether the analysis itself is sound.

Appraiser qualifications are not a formality, they are a threshold requirement that determines whether the report or review is admissible and defensible in the proceeding it was commissioned to support.

FAQ

What is the difference between an appraisal review and a second opinion?

The main difference between an equipment appraisal review and a second opinion is that an appraisal review analyzes an existing report for accuracy, methodology, and USPAP compliance, while a second opinion produces a new independent valuation. Reviews validate or challenge a report, while second opinions establish a separate value conclusion.

When should a lender order an equipment appraisal review instead of a new appraisal?

A lender should order an appraisal review instead of a new appraisal when an existing report is recent, typically within 90–180 days, and appears credible. Reviews verify accuracy, methodology, and USPAP compliance at lower cost. Lenders order new appraisals when data is outdated, incomplete, or materially disputed.

Can two qualified appraisers legitimately reach different value conclusions on the same equipment?

Two qualified appraisers can legitimately reach different value conclusions on the same equipment due to differences in assumptions, data sources, and valuation approaches. Variations in market comps, condition assessments, and highest and best use analysis can produce value differences, typically within a 5–20% range for credible appraisals.

What USPAP standards govern an equipment appraisal review?

USPAP Standard 3 governs an equipment appraisal review. Standard 3 defines requirements for developing and reporting appraisal reviews, including scope of work, reviewer independence, and analysis of the original appraisal’s methodology and conclusions. Reviewers must also comply with USPAP Ethics and Competency Rules.

What is the difference between a desk review and a field review?

The main difference between a desk review and a field review is that a desk review analyzes the report remotely, while a field review adds an on-site inspection to verify the equipment and support the value conclusion.

Why does the value definition (FMV vs. OLV) matter when comparing two equipment appraisals?

The value definition matters because FMV and OLV measure different market conditions. Fair market value reflects a normal sale between willing parties, while orderly liquidation value reflects a timed sale with constrained marketing. Two equipment appraisals using different definitions can produce materially different conclusions, even when they value the same assets.

Can an appraisal review replace a second opinion in litigation?

An appraisal review does not replace a second opinion in litigation because a review critiques an existing appraisal, while a second opinion delivers an independent value conclusion.

How much can two equipment appraisals differ without one being wrong?

Two equipment appraisals can differ by 10% to 30% without either being wrong, and larger differences can be reasonable when market conditions, assumptions, or appraisal scopes are different.

What qualifications must an appraiser have to conduct a USPAP Standard 3 review?

A USPAP Standard 3 reviewer must be competent in the asset type, appraisal methods, and review process, and the reviewer must meet any licensing or certification requirements that apply to the assignment.