Orderly Liquidation Value Equipment Appraisal

Orderly liquidation value (OLV) is the estimated gross amount a piece of equipment would sell for if marketed through normal channels within a defined, compressed timeline, with the seller compelled to sell on an as-is, where-is basis.

OLV sits below fair market value (FMV) and above forced liquidation value (FLV) in the value hierarchy. It is the standard value basis for asset-based lending, SBA loan collateral, bankruptcy proceedings, and most secured finance transactions involving equipment.

What Orderly Liquidation Value Means

OLV is an opinion of the gross amount, expressed in terms of money, that could typically be realized from a liquidation sale given a reasonable time to find a purchaser, with the seller compelled to sell on an as-is, where-is basis. The definition encodes 4 specific assumptions that separate OLV from every other value type.

First, the seller is motivated.

OLV assumes the seller must sell, not that they choose to. This is the compulsion element.

Second, marketing is active.

The equipment is exposed to the market through normal dealer, broker, or auction channels with reasonable advertising.

Third, time is constrained but not arbitrary.

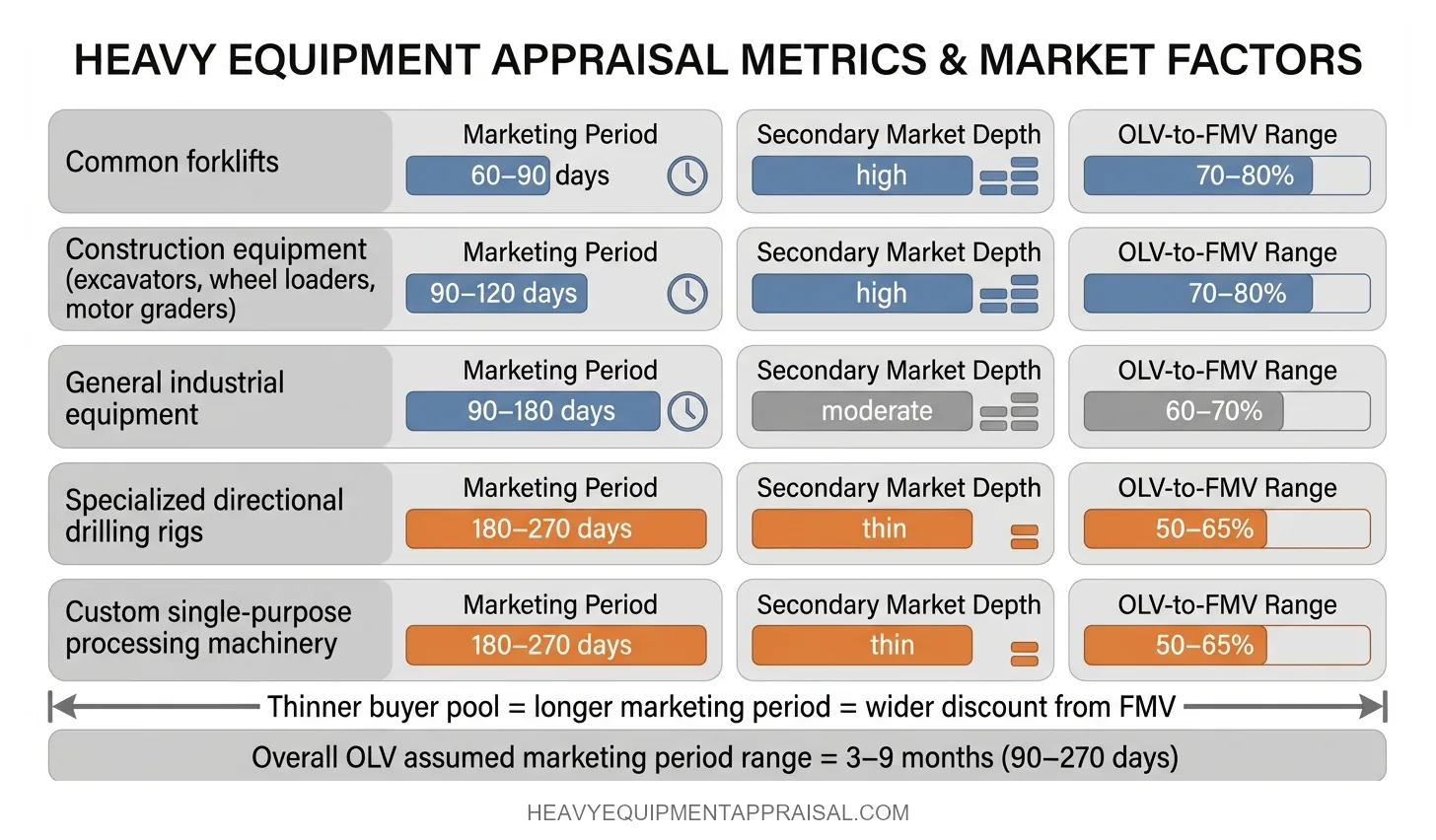

The assumed marketing period typically ranges from 3 to 9 months depending on equipment type and secondary market depth. A fleet of common forklifts may reach full OLV exposure in 60 to 90 days. A specialized piece of directional drilling equipment may need 6 to 9 months to reach the buyer pool capable of paying OLV.

Fourth, the sale is as-is, where-is.

No warranties, no delivery, no refurbishment commitments from the seller. The word “orderly” refers to the sale process, not the seller’s financial condition. An orderly sale means normal channels, appropriate market exposure, and a structured disposition.

Contrast this with FMV, which assumes no time pressure and both parties fully willing with no compulsion on either side. The time constraint is the single variable that separates OLV from FMV. That constraint reduces the buyer pool, which reduces the realized price. An appraiser who does not identify and define the specific value premise in the report has not produced a usable OLV opinion.

How OLV Is Developed in an Equipment Appraisal

An appraiser develops OLV primarily through the sales comparison approach: identifying comparable equipment transactions from auction results, dealer sales, and private transactions, then applying adjustments for condition, hours, configuration, and market timing.

The sales comparison approach is the operative method because OLV is a market-derived value. It reflects what buyers actually pay under constrained-time conditions, not what it costs to replace the asset or what it earns in service.

Why Auction Data Anchors OLV

Auction results from houses like Ritchie Bros., IronPlanet, and Purple Wave are the most common OLV data anchors. Auctions impose time and place constraints on the sale: the equipment sells on a specific date, to whichever buyers are present or bidding online, with no extended negotiation period.

These conditions approximate OLV assumptions more closely than FMV assumptions. An appraiser sourcing comparables for OLV will weight auction transaction data heavily, while treating active dealer listings (which reflect asking prices, not transaction prices) as contextual, not as direct comps.

Adjustment Methodology

When a direct match exists (same make, model, year, and configuration with known transaction data), the appraiser uses that data as the primary indicator. When no direct match exists, a comparable match with adjustments is used. The primary adjustment variables for OLV are:

- Condition and hours/usage. A Caterpillar 320 excavator with 4,000 hours and a machine of the same model with 9,000 hours are different assets. The appraiser quantifies that difference.

- Configuration and attachments. Optional packages, bucket sizes, technology upgrades, and missing components all adjust value.

- Market timing. A transaction from 18 months ago in a different demand cycle requires a time adjustment to reflect current conditions.

- Geographic market. Regional supply-demand dynamics affect secondary market prices. Auction results from the Gulf Coast oilfield market may not directly translate to the Midwest agricultural market for the same piece of equipment.

What Does Not Produce a Defensible OLV

An OLV conclusion derived solely from replacement cost new minus a depreciation percentage, with no transaction data support, is analytically weak.

The cost approach produces replacement cost new less depreciation (RCNLD), a value premise rooted in what it costs to acquire an equivalent asset new and then adjusting for wear. That is a different question than what the market will pay under constrained-time conditions.

Appraisers may reference cost data for context, but an OLV report that cites no comparable sales and relies entirely on depreciation schedules is unlikely to survive lender review or legal challenge.

OLV vs. Fair Market Value vs. Forced Liquidation Value

OLV typically returns 60–80% of FMV for most heavy equipment categories. FLV typically returns 40–60% of FMV. The spread depends on equipment type, condition, age, and how liquid the secondary market is for that specific asset.

The same piece of equipment carries 3 valid values simultaneously. The value type is a function of the assumed sale scenario, not the asset itself.

| Value Type | Key Assumption | Typical Use Case |

|---|---|---|

| Fair Market Value (FMV) | No time pressure. Willing buyer, willing seller, both with reasonable knowledge. No compulsion. | Insurance replacement, estate and divorce proceedings, charitable donation (IRS Form 8283), purchase price allocation |

| Orderly Liquidation Value (OLV) | Seller compelled to sell. Active marketing through normal channels. Constrained timeline (3–9 months). As-is, where-is. | Asset-based lending, SBA loan collateral, bankruptcy, secured finance, M&A liquidation-floor analysis |

| Forced Liquidation Value (FLV) | Seller compelled to sell immediately. Minimal or no marketing period. Typically a public auction with no reserve. | Distressed asset recovery, court-ordered immediate liquidation, worst-case collateral scenarios |

Concrete Scenario

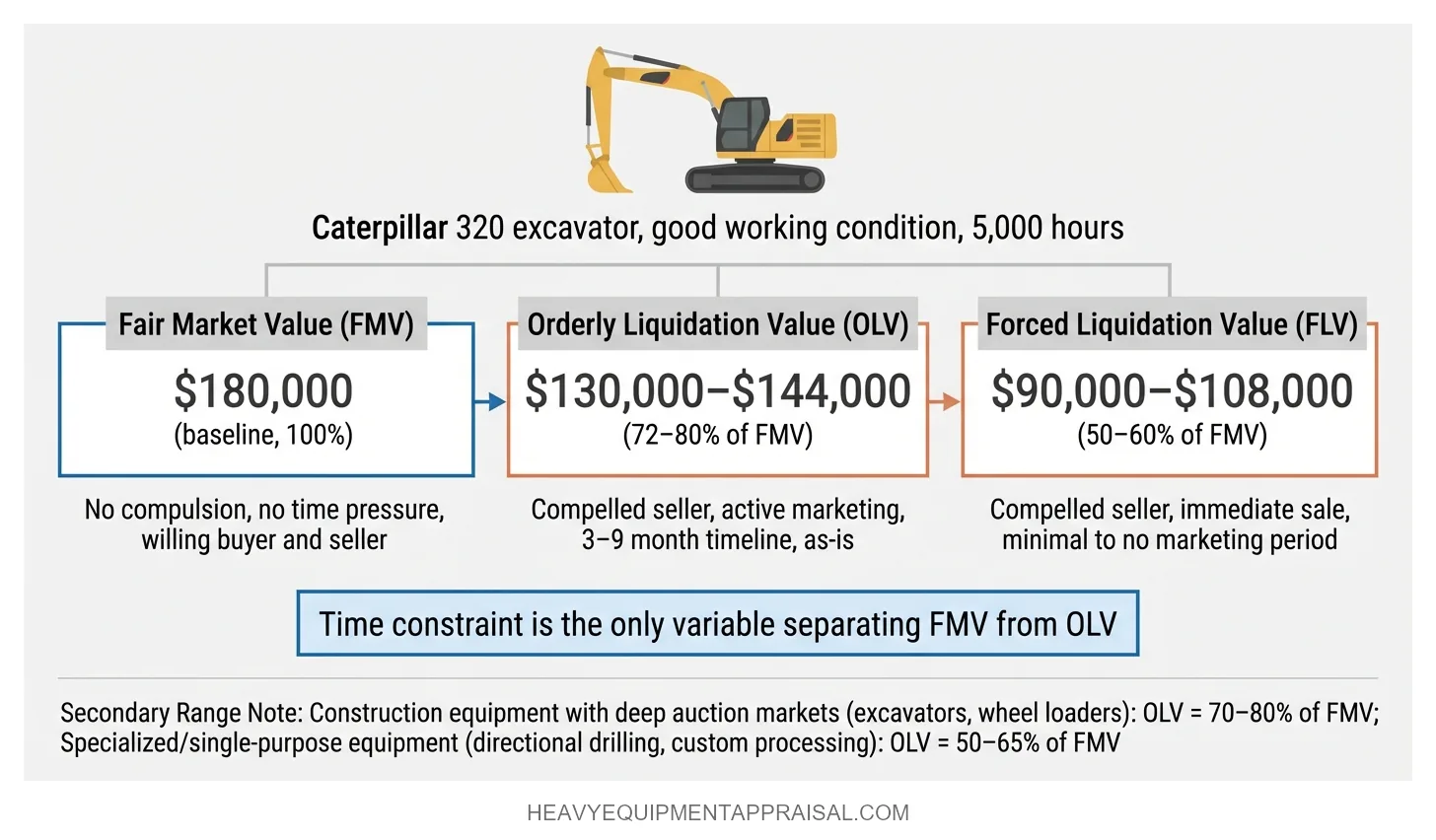

A Caterpillar 320 excavator in good working condition with 5,000 hours, appraised at $180,000 FMV, might return $130,000–$144,000 OLV and $90,000–$108,000 FLV. Same machine, same day, 3 different numbers. The difference is the assumed sale scenario.

Construction equipment with deep auction markets (excavators, wheel loaders, motor graders) tends toward the higher end of the OLV-to-FMV range: 70–80%. Specialized industrial or single-purpose equipment (custom processing machinery, directional drilling rigs) tends toward the lower end: 50–65%. The thinner the buyer pool, the wider the discount from FMV.

A full comparison of when each value type applies is covered in the FMV vs. OLV vs. FLV breakdown.

Lenders use OLV to size collateral because a default scenario is closer to an OLV sale than an FMV sale. Requesting FMV for a collateral-dependent loan produces a number that overstates what the lender would actually recover.

When OLV Is the Required Value Standard

OLV is the required or preferred value standard in asset-based lending (ABL), SBA-backed equipment financing, bankruptcy proceedings, and most collateral-dependent loan transactions.

SBA Loan Collateral

SBA Standard Operating Procedure (SOP) 50 10 7.1, effective March 2024, governs 7(a) and 504 loan programs. For equipment collateral valued at $500,000 or more, the SBA requires an equipment appraisal from a qualified appraiser. The required value basis is OLV, not FMV.

The SBA’s reasoning is explicit: in a default scenario, the lender’s recovery reflects a liquidation scenario, not a willing-buyer/willing-seller transaction. Appraisals must comply with the Uniform Standards of Professional Appraisal Practice (USPAP).

More detail on SBA equipment collateral requirements is available in the dedicated guide.

Asset-Based Lending

ABL lenders and commercial finance companies calculate advance rates against OLV (or NOLV, discussed below). Typical advance rates run 70–85% of OLV for well-maintained equipment in active secondary markets. A borrower with $1,000,000 in equipment at OLV might receive a $700,000–$850,000 credit facility. The advance rate exists specifically because OLV already reflects a constrained-sale discount from FMV.

The lender’s margin of safety is built into the spread between the advance and the OLV floor.

Bankruptcy and Receivership

Courts and trustees use OLV to establish what creditors could reasonably recover from equipment collateral in a going-concern wind-down.

Federal bankruptcy courts have accepted OLV testimony to determine creditor recovery estimates, including the distinction between OLV “in place” (equipment sold as part of an operating facility) and OLV “in exchange” (equipment removed and sold individually). That distinction can shift the value by 10–20% depending on the asset’s integration into the facility.

M&A Due Diligence

Buyers conducting an asset acquisition of an operating company may request OLV alongside FMV to understand the liquidation floor.

The OLV figure answers the question: if this acquisition fails and we need to recover capital from the equipment, what is the realistic recovery?

More on this use case is in the guide to equipment appraisal in M&A due diligence.

What OLV Is Not Required For

OLV is not the appropriate value basis for insurance replacement cost appraisals, charitable donation appraisals (IRS Form 8283 requires FMV), or estate and divorce proceedings where FMV is the legal standard. Using OLV in a context that requires FMV understates the asset and produces a report that fails its intended purpose.

Net Orderly Liquidation Value (NOLV): A Distinct but Related Concept

Net orderly liquidation value (NOLV) is OLV minus the estimated costs of sale. NOLV represents the net proceeds a creditor would actually recover after paying the costs required to convert the equipment into cash.

The distinction matters because lenders care about what hits the account, not the gross sale price. The typical deductions that separate NOLV from OLV include:

- Auction commissions: 10–18% of gross, depending on the auction house, equipment type, and negotiated terms. Ritchie Bros. and IronPlanet typically charge a buyer’s premium plus seller fees that combine to reduce seller net proceeds by 12–15%.

- Transportation and rigging: Moving a crawler crane from an industrial site to an auction yard or buyer location can cost $5,000–$25,000 or more depending on distance, permits, and equipment size.

- Storage costs: If equipment must be held at a third-party yard during the marketing period.

- Refurbishment costs: If the equipment requires repair to be saleable, though OLV’s as-is assumption limits this category.

- Remarketing fees: Broker or dealer commissions if the sale is handled through a non-auction channel.

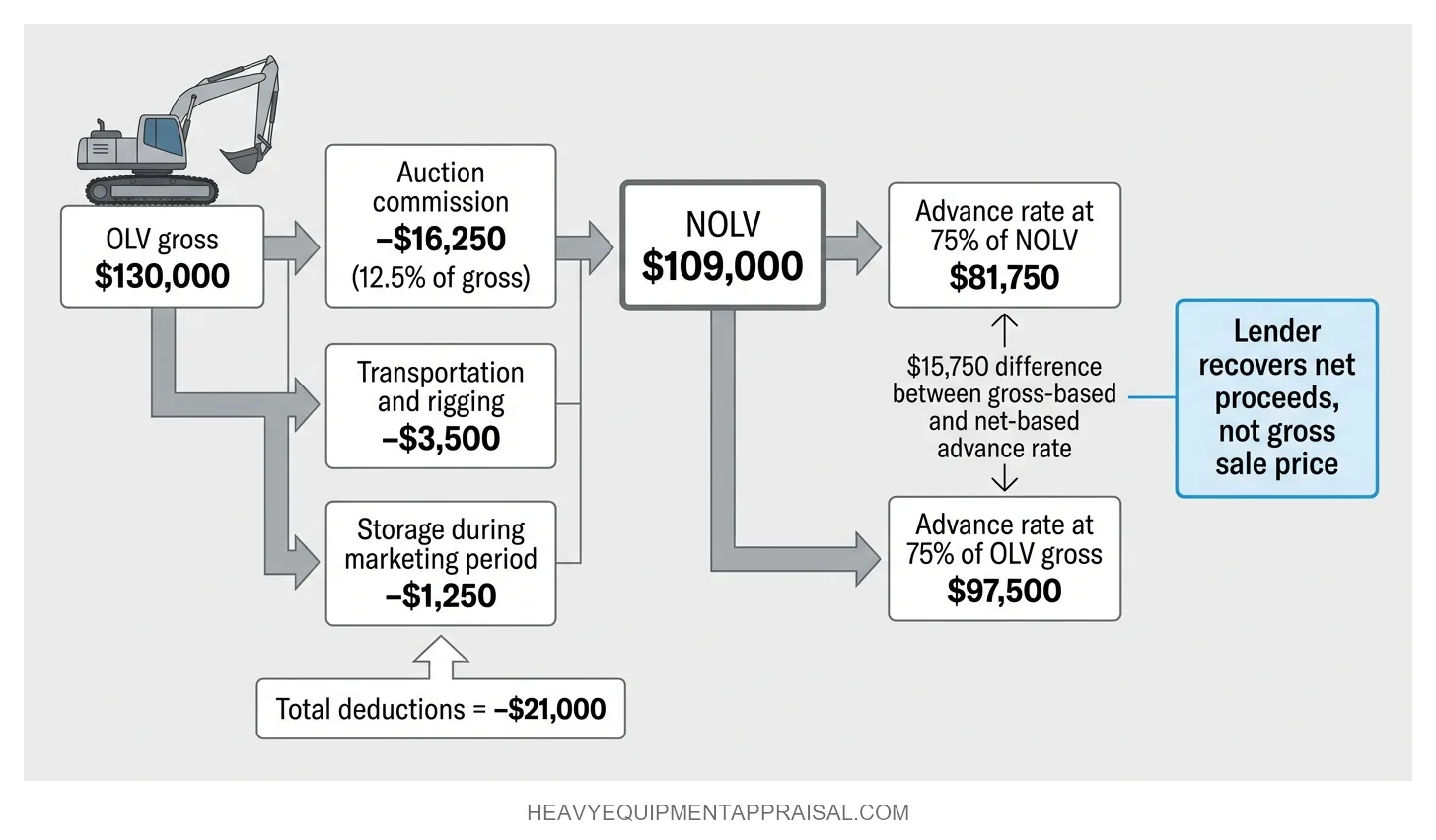

Worked Example

A crawler excavator appraised at $130,000 OLV with estimated costs of sale: $16,250 auction commission (12.5% of gross), $3,500 transportation and rigging, $1,250 storage for the marketing period.

Total costs: $21,000. NOLV: $109,000.

The advance rate calculation in many ABL transactions runs against NOLV, not OLV gross. At a 75% advance rate against NOLV, the credit facility for this single asset would be approximately $81,750, not the $97,500 that 75% of OLV gross would suggest.

USPAP requires clear identification of which value is being reported. An appraisal that states “liquidation value” without specifying whether the figure is gross (OLV) or net (NOLV) creates ambiguity that can misalign lender expectations with actual recovery.

What Makes an OLV Appraisal Credible (and What Doesn't)

A credible OLV appraisal is supported by identified, adjusted comparable sales from recognized secondary market data sources, reported under a defined scope of work that states the value premise explicitly and complies with USPAP.

USPAP Compliance

USPAP Standards Rule 7-2 governs personal property appraisal development. SR 7-2(b) requires the appraiser to identify the type and definition of value and the source of that definition.

An OLV appraisal that says "liquidation value" without specifying orderly versus forced is non-compliant with SR 7-2(b) and potentially misleading. SR 7-2(d) requires identification of the effective date. SR 7-2(f) requires a scope of work sufficient to produce credible assignment results.

Full detail on USPAP scope of work requirements is in the standards guide.

Scope of work definition is the most common compliance failure in OLV reports prepared for lenders. If the engagement letter does not specify the value basis, the appraiser may deliver a technically compliant report that does not reflect what the lender actually needs.

Appraiser Credentials

The appraiser's credential signals competency in equipment-specific valuation methodology. The ASA (American Society of Appraisers) Machinery and Technical Specialties designation (AM, ASA, FASA) and the CMEA (Certified Machinery & Equipment Appraiser) credential are the 2 primary markers for equipment appraisers.

Both require demonstrated competency in the sales comparison approach and value premise identification. A report signed by someone with no equipment-specific credential is not automatically invalid, but it carries less weight under lender review or in litigation.

Red Flags in a Weak OLV Report

A lender, attorney, or borrower reviewing an OLV report should look for these documented failure modes:

- No comparable sales cited. The value is derived entirely from cost-depreciation schedules with no market transaction support.

- Value type not explicitly identified. The report says "liquidation value" without specifying orderly or forced.

- No effective date. Equipment values shift with market conditions. A report without an effective date cannot be tied to a specific market.

- No USPAP compliance statement or scope of work section. This omission calls the entire report's methodological rigor into question.

- Comparables from irrelevant markets. Auction results from a Gulf Coast oilfield market applied without adjustment to Midwest agricultural equipment.

- No condition assessment or hours adjustment documented. 2 machines of the same model with different hours and condition are different assets. If the report does not document the adjustment, the conclusion is unsupported.

- No equipment-specific credential. The appraiser holds no ASA-MTS or AMEA designation.

An inflated OLV hurts the borrower, not just the lender. If a lender advances against an OLV that overstates recovery and the equipment sells below that figure at default, the borrower faces a deficiency balance. The credibility of the OLV number protects both sides of the transaction.

Getting the Assumptions Right

OLV is not a conservative estimate of value. It is an accurate estimate of value under a specific set of sale assumptions:

- Compelled seller

- Active marketing

- Constrained timeline

- As-is condition

Getting those assumptions wrong, or allowing an appraiser to leave them unstated, produces a number that neither the lender nor the borrower can rely on when it matters.

A reader who needs an OLV appraisal now knows what the number represents, how it is developed, what distinguishes it from NOLV, and where to look in the report to verify that the conclusion is supported.