Equipment Appraisal for SBA Loans

SBA lenders require a qualified equipment appraisal when machinery, vehicles, or production equipment serve as loan collateral and exceed the dollar thresholds defined in SBA Standard Operating Procedure 50 10 (SBA SOP 50 10).

The applicable value standard is orderly liquidation value (OLV), not fair market value (FMV), because the SBA’s collateral framework sizes equipment against default-recovery risk. A non-compliant appraisal can stall or kill a loan closing.

When the SBA Requires an Equipment Appraisal

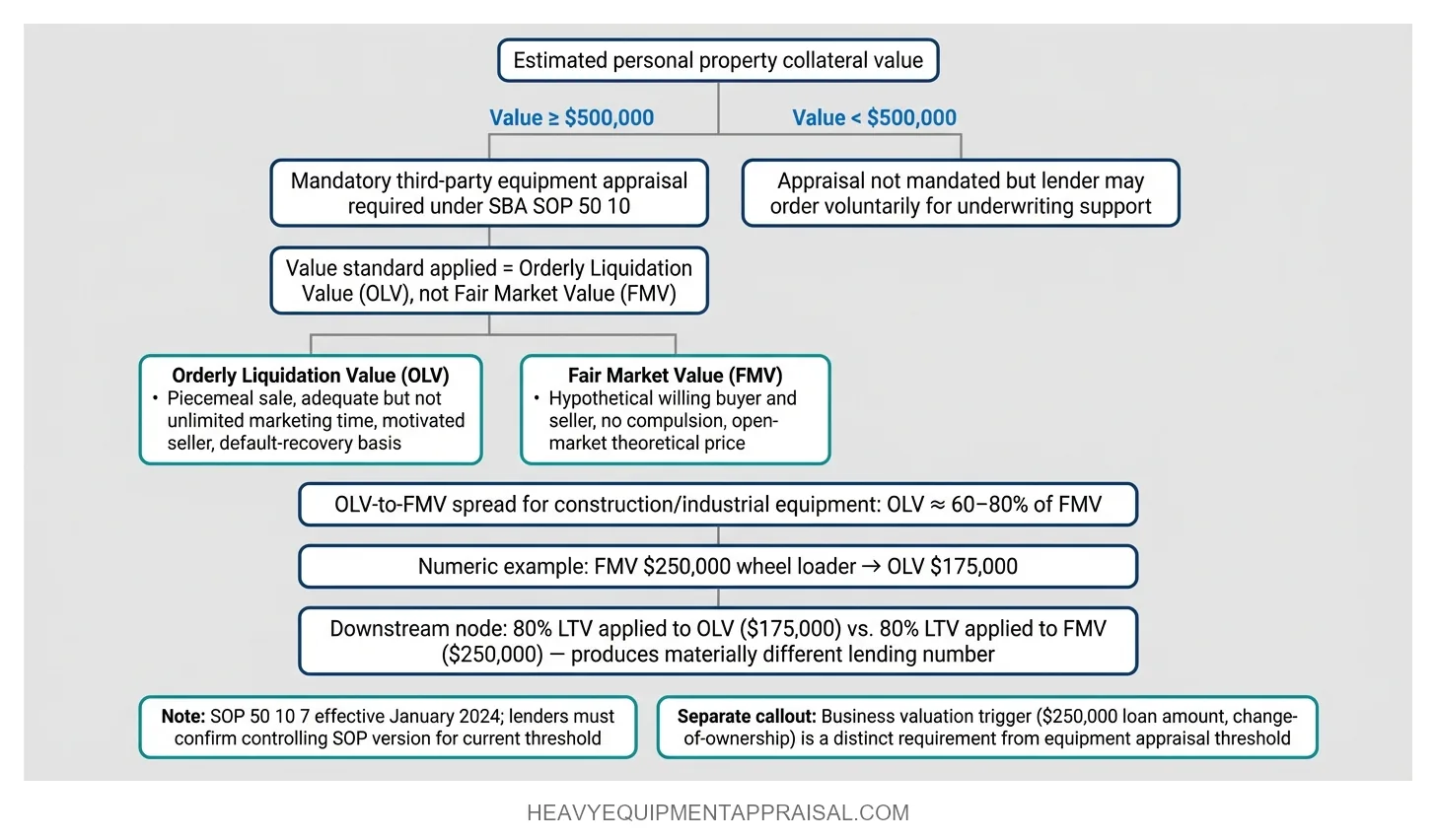

The SBA mandates a third-party equipment appraisal when personal property taken as collateral (equipment, machinery, fixtures, or inventory) meets or exceeds the dollar threshold specified in SBA SOP 50 10.

The commonly cited trigger is $500,000 in estimated personal property value, though the SOP has been revised multiple times, with SOP 50 10 7 (effective January 2024) restructuring certain collateral requirements. Lenders and borrowers should confirm the current threshold against the controlling SOP version before ordering an appraisal.

This threshold applies to both SBA 7(a) loans and SBA 504 loans, though the two programs apply it differently. Under an SBA 7(a) loan, the lender retains some discretion in how collateral is evaluated below the mandatory threshold.

Under an SBA 504 loan, the Certified Development Company (CDC) may impose additional requirements beyond the SOP baseline. The trigger for a mandatory business valuation ($250,000 in loan amount for change-of-ownership transactions) is a separate requirement from the equipment appraisal threshold. Conflating the two is a common error in SBA lending discussions.

Even below the mandatory threshold, lenders routinely order equipment appraisals to support loan-to-value calculations and demonstrate prudent underwriting. A lender who skips the appraisal on a $400,000 equipment package and later faces a default has a collateral file with no independent value support.

Which Value Standard the SBA Requires (and Why It's OLV, Not FMV)

SBA collateral policy specifies "net recovery value" or "liquidation value" for personal property, which is functionally equivalent to orderly liquidation value (OLV) as defined under USPAP and ASA standards. The SBA does not use the term "fair market value" for equipment collateral sizing.

OLV assumes the equipment will be sold piecemeal with adequate but not unlimited marketing time, by a motivated seller, in an orderly disposal scenario. FMV, by contrast, assumes a hypothetical willing buyer and seller, both with reasonable knowledge, under no compulsion to act. The structural difference is that OLV reflects what a lender would actually recover in a default, while FMV reflects a theoretical open-market transaction price.

For most construction and industrial equipment categories, OLV returns approximately 60–80% of FMV. A wheel loader with an FMV of $250,000 might appraise at $175,000 OLV. That spread matters when a lender is calculating collateral coverage. An 80% loan-to-value ratio applied against OLV produces a materially different lending number than the same ratio applied against FMV.

Understanding how OLV compares to fair market value and forced liquidation value is essential for anyone involved in SBA collateral analysis.

What Qualifies as a Compliant SBA Equipment Appraisal

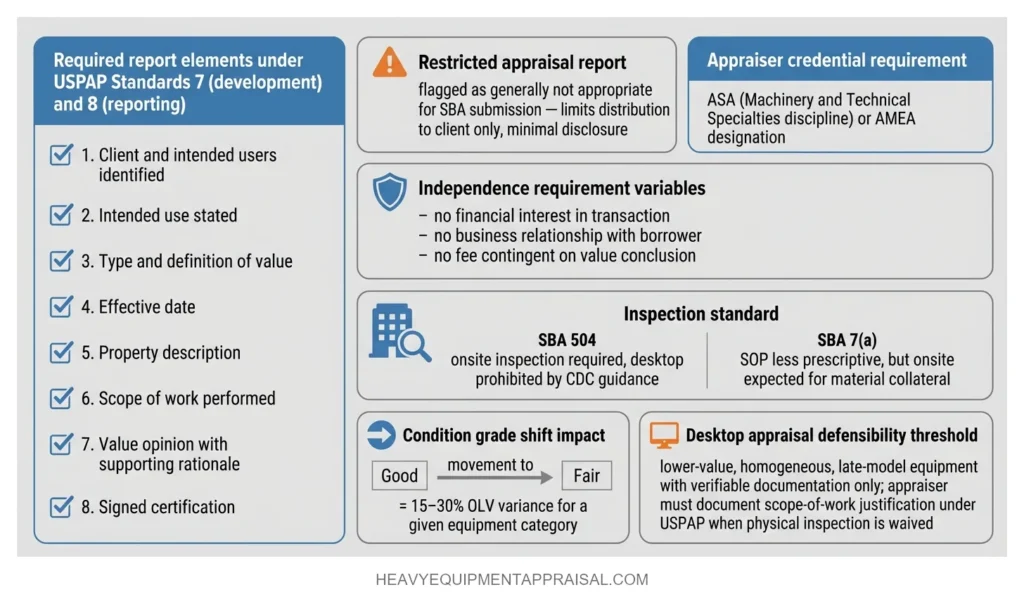

An SBA-compliant equipment appraisal must be performed by a qualified, independent appraiser and conform to the Uniform Standards of Professional Appraisal Practice (USPAP).

For SBA 504 loans, CDC guidance documents state this requirement explicitly. For SBA 7(a) loans, USPAP compliance flows through the lender's own underwriting standards and the SBA's requirement that appraisals be conducted by qualified professionals.

The SBA does not mandate a specific appraiser designation by name. In practice, lenders require appraisers credentialed through the American Society of Appraisers (ASA) Machinery and Technical Specialties discipline or the Association of Machinery and Equipment Appraisers (AMEA).

An ASA or CMEA credentialed appraiser carries a recognized professional designation tied to demonstrated competency in equipment valuation. "Qualified appraiser" without a recognized credential is too vague to satisfy most lender review departments.

Appraiser independence is a regulatory requirement, not a suggestion. The appraiser cannot have a financial interest in the transaction, a business relationship with the borrower, or any arrangement where the fee depends on the value conclusion.

The appraisal report must conform to USPAP Standards 7 (development) and 8 (reporting) for personal property. A USPAP-compliant appraisal report for SBA submission contains:

- Identification of the client and intended users

- Intended use of the appraisal

- Type and definition of value

- Effective date

- Description of the property appraised

- Scope of work performed

- The appraiser's opinion of value with supporting rationale, and a signed certification.

A restricted appraisal report (the most abbreviated USPAP format) is generally not appropriate for SBA submission because it limits distribution to the client only and contains minimal disclosure.

Equipment Appraisals in SBA Business Acquisitions

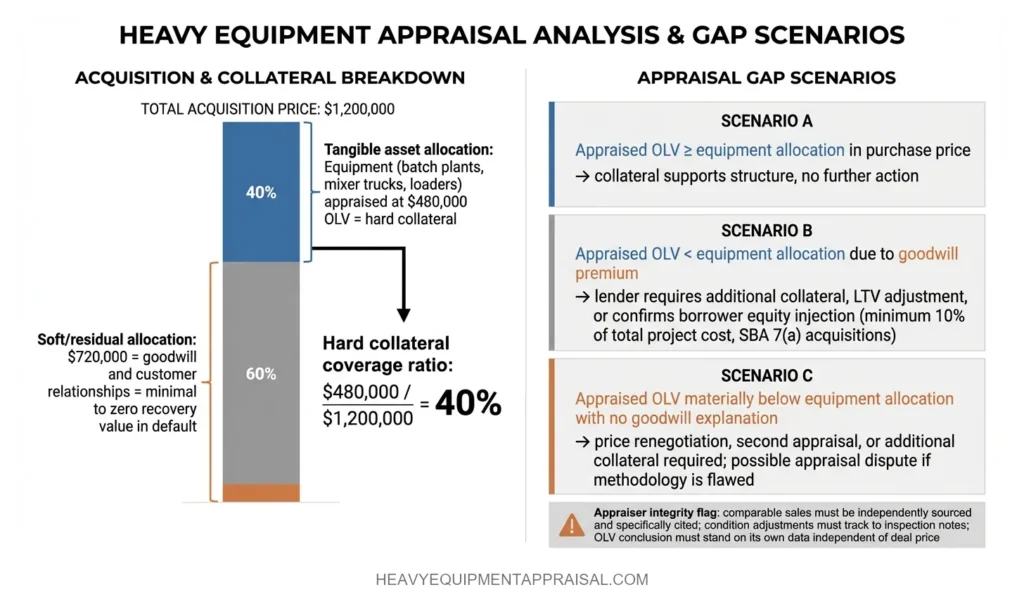

When an SBA loan finances the purchase of an existing business, the equipment appraisal serves a specific function: establishing the OLV of tangible assets so the lender can distinguish hard collateral from goodwill within the purchase price.

The purchase price in a business acquisition must be allocated among tangible assets (equipment, inventory, real estate), identifiable intangible assets (customer lists, non-compete agreements, trade names), and goodwill (the residual). The equipment appraisal establishes the tangible asset value. The SBA treats tangible assets as hard collateral. Goodwill and intangibles are soft collateral with minimal or no recovery value in a default scenario.

Consider a borrower acquiring a concrete contractor for $1.2 million. The equipment (batch plants, mixer trucks, loaders) appraises at $480,000 OLV. The remaining $720,000 is attributed to goodwill and customer relationships. The lender now has $480,000 in hard collateral against a $1.2 million transaction. That gap determines whether additional collateral (real estate, personal assets) is required and how the loan is structured to meet SBA collateral adequacy standards.

The SBA does not decline loans solely for insufficient collateral, but the collateral shortfall affects every downstream lending decision. An equipment appraisal that accurately identifies and values each asset gives the lender a defensible basis for the allocation. An appraisal that inflates equipment values to narrow the goodwill gap creates a false collateral picture that unravels at default.

When Appraised Value and Purchase Price Diverge

A gap between appraised equipment value and the price a buyer is paying is common and does not automatically disqualify a loan. It does, however, change the lender's collateral analysis and may require additional equity from the borrower.

Three scenarios define how lenders handle the gap:

Appraised value meets or exceeds the equipment allocation in the purchase price. The collateral supports the loan structure. This is the simplest outcome.

Appraised value falls below the equipment allocation due to goodwill premium. This is typical in business acquisitions. The lender accounts for the shortfall by requiring additional collateral, adjusting the loan-to-value ratio, or confirming that the borrower's equity injection (typically 10% of total project cost for SBA 7(a) acquisitions) adequately offsets the gap.

Appraised value is materially below the equipment allocation with no goodwill explanation. This raises concerns about overpricing. The lender may require price renegotiation, a second appraisal, or additional collateral. The borrower may have grounds for disputing an appraisal result if the methodology is flawed, but a low appraisal supported by strong comparable sales methodology is difficult to overturn.

The appraiser's methodology matters here. An OLV opinion built on thin auction data or unsupported condition assumptions will produce a less defensible number than one grounded in verified comparable sales with documented adjustments for age, hours, and configuration.

What Borrowers and Lenders Should Prepare Before the Appraisal

A complete equipment appraisal for SBA purposes requires specific documentation, and missing records are the most common cause of delays in SBA lending transactions.

The borrower or seller should prepare:

- Equipment list with make, model, year of manufacture, serial number, and current hours or mileage for each unit

- Maintenance records and service logs (condition directly affects OLV, and documented maintenance supports higher condition grades)

- Titles, registration, or ownership documentation for titled assets (vehicles, trailers, certain mobile equipment)

- Lien information identifying any existing encumbrances on the equipment

- Equipment location with access details for onsite inspection scheduling

A complete document checklist for an equipment appraisal covers these items in detail. Incomplete documentation forces the appraiser to make assumptions about age, condition, or configuration. Every assumption introduces potential inaccuracy into the OLV conclusion, which then flows directly into the lender's collateral analysis.

Desktop vs. Onsite Appraisal for SBA Purposes

SBA 504 lender guidance is explicit: equipment appraisals must be conducted in person and cannot be desktop appraisals. For SBA 7(a) loans, the SOP is less prescriptive, but the underlying logic favors onsite inspection for any material collateral.

The reason is structural. OLV depends on condition assessment, and condition assessment depends on physical observation.

A desktop vs. onsite appraisal involves fundamentally different inspection scopes. A desktop appraisal relies on the borrower's or seller's representation of condition, which introduces systematic optimism bias. Movement between condition grades (from "Good" to "Fair," for example) can shift OLV by 15–30% for a given equipment category. That range is too large to leave unverified for collateral that secures an SBA-guaranteed loan.

Desktop appraisals may be defensible for lower-value, homogeneous, late-model equipment with verifiable documentation (a single late-model skid steer with a clean service record and documented hours, for instance).

Under USPAP scope-of-work rules, the appraiser must document why a desktop inspection is appropriate when physical inspection is waived.

For SBA transactions above the mandatory appraisal threshold, onsite inspection is the standard that lenders and SBA reviewers expect to see in the report file.