How to Dispute Equipment Appraisal: 4 Valid Grounds

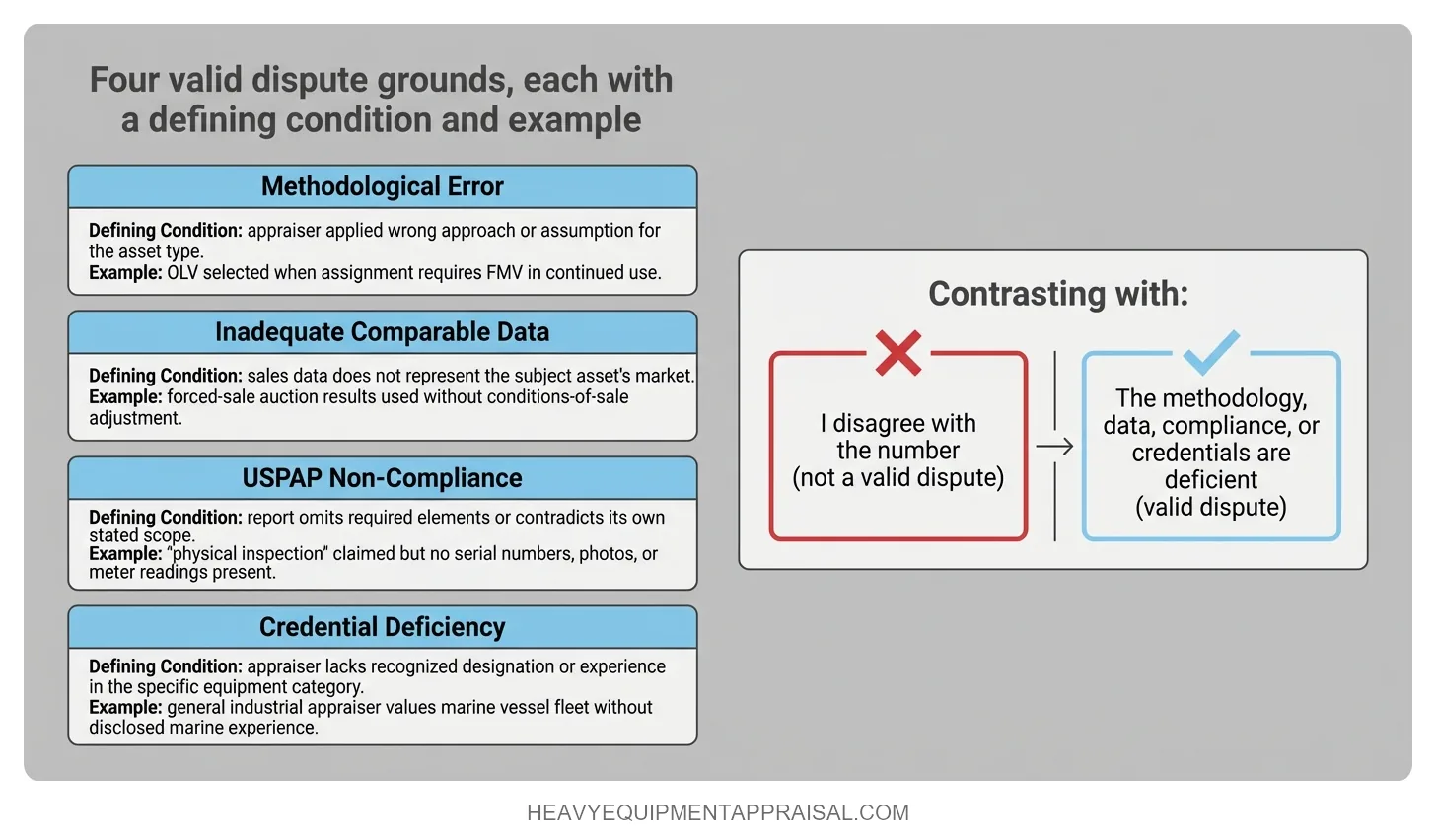

A heavy equipment appraisal can be formally disputed on four grounds:

- Methodological error

- Inadequate comparable data

- USPAP non-compliance

- Appraiser credential deficiency

Disagreeing with the final number is not a dispute.

A valid challenge requires identifying a specific, documentable flaw in how the value was developed. This process matters most to business owners contesting a low valuation, lenders questioning collateral coverage, and attorneys challenging appraisal testimony in litigation.

What Qualifies as a Valid Dispute

A valid appraisal dispute is based on a specific, documentable error in how the value was developed, not a preference for a higher or lower number. Courts, lenders, and review appraisers distinguish between “I disagree with the conclusion” and “the methodology, data, compliance, or credentials are deficient.” Only the latter category triggers a formal challenge process.

Four grounds qualify:

- Methodological error

- The appraiser applied an approach, technique, or assumption that is inappropriate for the asset or the assignment’s purpose. Selecting orderly liquidation value when the engagement calls for fair market value in continued use is a methodological error. So is assigning a “Good” condition rating to a motor grader with a documented accident history and no physical inspection. The error must be identifiable in the report and traceable to its effect on the value conclusion.

- Inadequate comparable data

- The appraisal relies on sales data that does not reasonably represent the subject asset’s market. This includes using comparables from a different equipment category, a different geographic market without adjustment, or a different level of trade. When a direct match exists in the market and the appraiser substitutes a comparable match without documenting why, the data basis is challengeable. The same applies when the appraiser defaults entirely to the cost approach without disclosing the absence of market transaction data.

- USPAP non-compliance

- The report fails to meet the minimum requirements of the Uniform Standards of Professional Appraisal Practice. Common examples include omitting the value definition, stating a scope of work that contradicts the report’s own evidence (claiming physical inspection when no condition photographs or serial numbers appear), or delivering a restricted-use report to a third party for lending or litigation purposes. A restricted report explicitly requires access to the appraiser’s workfile to be understood. Providing one to a lender or court as standalone support is a compliance failure that can disqualify the report regardless of its methodology.

- Credential deficiency

- The appraiser lacks credentials, training, or demonstrated experience relevant to the specific equipment category. An appraiser credentialed in general industrial machinery who values a fleet of marine vessels without disclosed marine appraisal experience presents a credential gap. This ground is strongest when combined with one of the other three.

A bare objection (“the value seems low”) without evidence tied to one of these four categories rarely succeeds in court, in a lender review, or in a formal complaint process. The distinction matters because pursuing the wrong type of challenge wastes time and can undermine credibility when a legitimate flaw does exist in the report.

How to Identify Errors in an Appraisal Report

Appraisal errors fall into three categories: scope-of-work errors, data errors, and reporting errors:

- Scope-of-work errors

- The scope of work states what the appraiser did and why that level of investigation was appropriate. A desktop appraisal that does not disclose the absence of a physical inspection, or that claims condition ratings without photographs or serial number verification, has a scope deficiency. Look for mismatches between the stated scope and the report’s own evidence. A report claiming “on-site inspection” that contains no condition photographs, no recorded serial numbers, and no notation of hours or meter readings contradicts itself. Also examine whether the scope fits the assignment: a fleet of 30 crawler excavators valued for SBA lending collateral via a restricted desktop report raises an immediate question about whether the level of investigation was sufficient for the intended use.

- Data errors

- These appear in the comparable sales, the cost basis, or the condition assessment. In the sales comparison approach, check whether the comparables match the subject in equipment category, capacity class, and approximate age. Auction results used without adjustment for conditions of sale (forced vs. orderly) are a frequent and documentable flaw. In the cost approach, verify that the replacement cost new reflects current pricing, not a stale catalog figure. Condition ratings assigned without documented support (“Good” on a 15-year-old unit with no maintenance records referenced) signal unsupported judgment.

- Reporting errors

- A compliant report must include the value type with its definition, the effective date, the intended use, all assumptions and limiting conditions, and the appraiser’s certification. Each missing element is a discrete, citable deficiency. The most consequential reporting error is a mismatch between the value type and the assignment’s purpose. An appraisal concluding fair market value when the lender ordered orderly liquidation value does not answer the question it was hired to answer, regardless of how sound the underlying analysis may be.

Each category leaves distinct indicators in the report itself, and each requires a different challenge strategy. Reviewing a report systematically against these categories prevents the common mistake of fixating on the final number while missing the structural flaw that produced it.

A report that survives all three checks is not necessarily correct, but a report that fails any one of them gives a challenging party specific, documentable grounds. Identifying the category of error first determines whether the appropriate next step is an appraisal review, a formal complaint, or litigation testimony preparation.

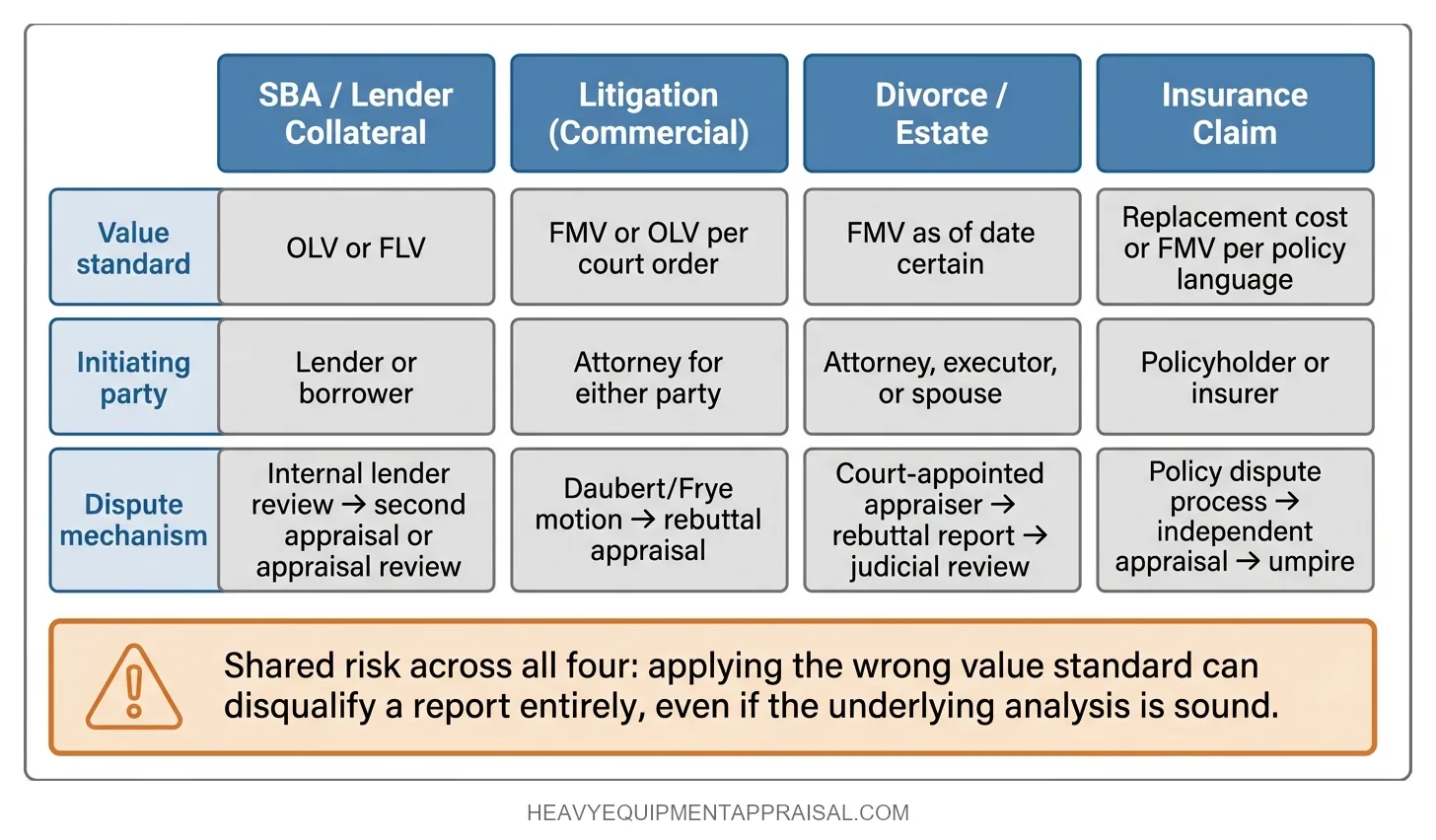

Grounds for Dispute by Context

The appropriate dispute mechanism, the applicable value standard, and the party who initiates the challenge all vary by context. An SBA lender disputing collateral coverage follows a different path than an attorney challenging appraisal testimony at trial.

Matching the dispute to the correct procedural framework is the first step toward a successful challenge.

| Context | Typical Value Standard | Initiating Party | Primary Dispute Mechanism |

|---|---|---|---|

| SBA / lender collateral | OLV or FLV | Lender or borrower | Internal lender review, then second appraisal or appraisal review |

| Litigation (commercial) | FMV or OLV per court order | Attorney for either party | Expert challenge (Daubert/Frye motion), rebuttal appraisal |

| Divorce / estate | FMV as of specific date | Attorney, executor, or spouse | Court-appointed appraiser, rebuttal report, or judicial review |

| Insurance claim | Replacement cost or FMV per policy | Policyholder or insurer | Policy dispute process, independent appraisal clause, umpire |

SBA and Lender Disputes

SBA and lender disputes center on whether the appraisal supports the collateral value the lender needs. Lenders typically order OLV because they are sizing collateral against default risk. The borrower’s challenge path starts with the lender’s internal review desk. If the lender rejects the borrower’s objection, the borrower can commission an appraisal review or a second independent appraisal to present competing evidence.

Lender Disputes

Litigation disputes test the appraisal’s admissibility and credibility under rules of evidence. The opposing attorney can file a Daubert or Frye motion arguing the appraiser’s methodology does not meet the standard for expert testimony. Alternatively, the opposing side retains its own appraiser and presents a rebuttal report. The court weighs the competing conclusions based on methodology, data quality, and USPAP compliance.

Divorce and Estate Proceedings

Divorce and estate proceedings require FMV as of a date certain, often months or years before the hearing. The most common dispute ground here is the effective date: an appraisal reflecting current market conditions when the court requires the date-of-separation value is procedurally deficient regardless of its analytical quality.

Insurance Claims

Insurance claims operate under the policy’s own dispute clause. Many commercial equipment policies include an independent appraisal provision where each side selects an appraiser and the two appraisers select an umpire. The value standard depends on the policy language, not on standard appraisal practice, which means an otherwise sound report can be disputed simply because it applied FMV when the policy specifies replacement cost.

Each context carries different consequences for using the wrong value standard. A report that concludes the right number under the wrong standard can be disqualified entirely, producing a worse outcome than a report with a minor data error that at least answers the correct question.

How to Challenge an Appraiser’s Methodology

The most effective methodology challenge demonstrates that the appraiser selected the wrong valuation approach for the asset type, misapplied the chosen approach, or failed to document the adjustments that connect raw data to the value conclusion.

Each of the three standard approaches (cost, sales comparison, and income) carries specific requirements for when it applies and how it must be supported. A challenge that names the specific methodological failure and traces its dollar impact on the conclusion carries far more weight than a general objection to the number.

Approach Selection

The cost approach is standard for specialized or custom-built equipment where market transaction data is scarce. The sales comparison approach is preferred when an active resale market exists with sufficient comparable transactions. The income approach applies when the asset’s value derives primarily from its revenue-generating capacity.

An appraiser who defaults to the cost approach for a common piece of equipment (a late-model wheel loader, for example) when dozens of comparable sales are available has made a selection error. The challenge must show that adequate market data existed and that the appraiser either ignored it or failed to disclose why it was rejected.

Comparable selection and adjustment transparency

Within the sales comparison approach, every adjustment between a comparable sale and the subject asset requires documentation. If the appraiser used an auction result from a forced sale to value equipment under an orderly liquidation premise without adjusting for conditions of sale, that is a traceable, quantifiable error.

Likewise, comparables from a different capacity class, geographic market, or vintage year require disclosed adjustments. A report that lists comparables but shows no adjustment grid or narrative explaining how each was reconciled to the subject lacks the analytical transparency that USPAP demands.

Workfile documentation

The appraiser’s workfile must contain all data, calculations, and reasoning sufficient to allow another appraiser to replicate the analysis.

A methodology challenge gains significant strength when the opposing party requests the workfile and finds it thin or absent. If the appraiser cannot produce the source data for replacement cost figures, the basis for depreciation estimates, or the raw comparable transaction records, the report’s conclusions rest on unsupported judgment rather than documented analysis.

In formal proceedings, requesting the workfile is often the single most productive step a challenging party can take, because a methodology that cannot be reconstructed from its own documentation cannot be defended.

Appraiser Credential Deficiency as Grounds for Dispute

An appraiser who lacks recognized credentials or demonstrable competency in the specific equipment category can produce a report that is vulnerable to disqualification on its face.

This ground is distinct from methodology or data errors because it challenges the appraiser's authority to render the opinion at all, not the quality of the opinion itself.

Credential standards by context

The IRS requires that appraisals supporting charitable deductions or estate valuations be performed by a "qualified appraiser" who has earned a recognized designation from a professional organization (such as ASA or CMEA) or can demonstrate equivalent education and experience.

SBA lenders typically require appraisers with professional designations and documented experience in the relevant equipment category. In litigation, courts evaluate appraiser qualifications under their rules for expert testimony. A credential deficiency in any of these contexts gives the opposing party or reviewing institution a procedural basis to reject the report before the methodology is even examined.

Verification

ASA designations (Accredited Member, Accredited Senior Appraiser) are verifiable through the ASA's public directory. The CMEA designation is verified through its issuing organization.

The appraiser's certification page in the report should disclose designations held, relevant experience, and any USPAP competency disclosures. An appraiser credentialed in general industrial equipment who values a fleet of aircraft or marine vessels without disclosed specialized experience triggers the USPAP competency rule, which requires the appraiser to either acquire the necessary competency before accepting the assignment or withdraw.

When credential deficiency alone is sufficient

In IRS proceedings, a report signed by an appraiser who does not meet the "qualified appraiser" definition is disallowed by statute.

No analysis of methodology is necessary.

In lending and litigation, credential deficiency alone rarely invalidates a report, but it substantially weakens the report's standing when combined with any of the other three dispute grounds.

An appraiser whose credentials do not withstand scrutiny faces an uphill defense of every judgment call in the report, because the presumption of competence that a recognized designation provides is absent.

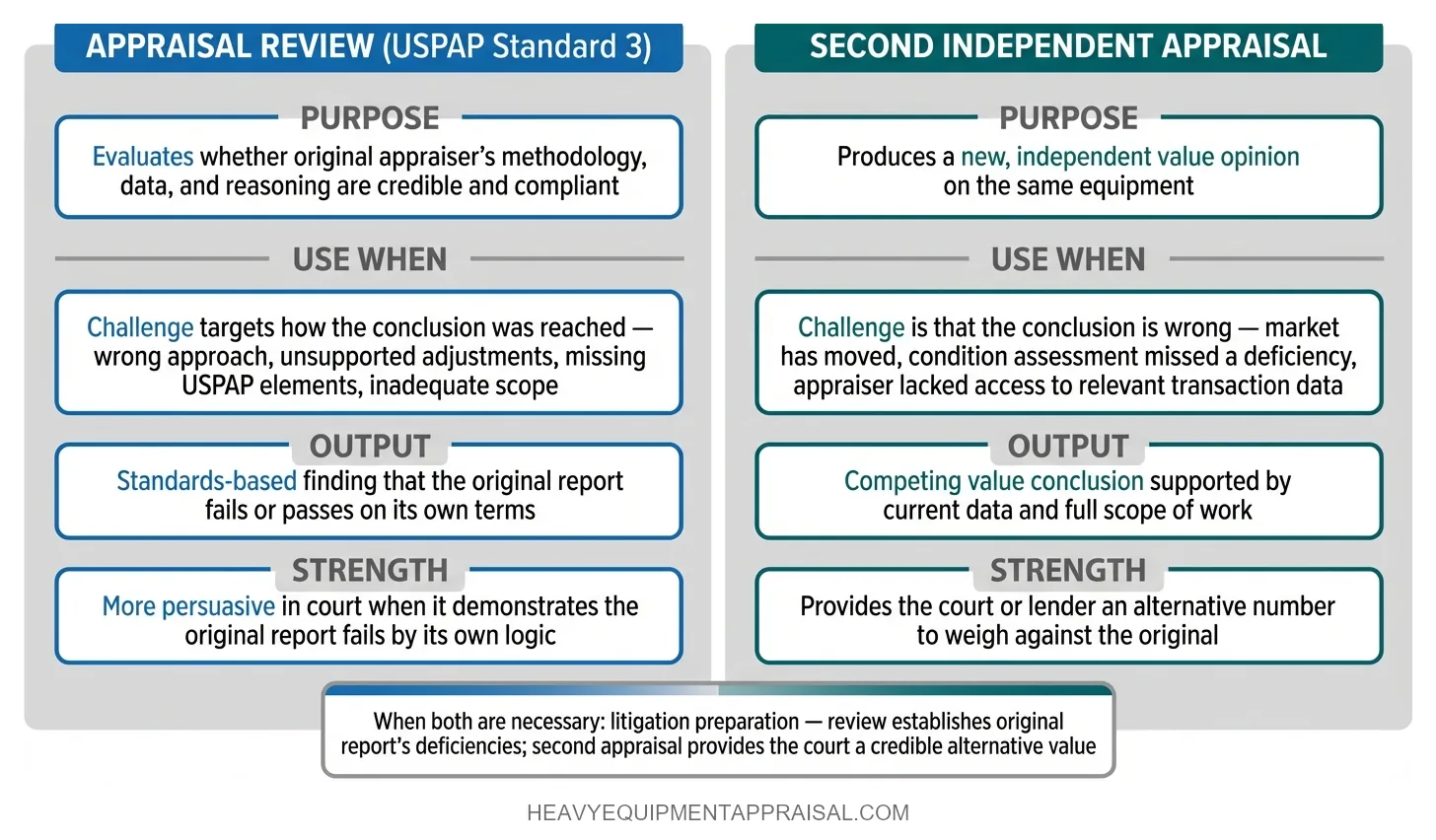

Appraisal Review vs. Second Appraisal: Which to Commission

An appraisal review and a second appraisal serve fundamentally different purposes, and commissioning the wrong one delays resolution while weakening the challenging party's position.

An appraisal review is a standards-based evaluation of an existing report, performed under USPAP Standard 3, that assesses whether the original appraiser's methodology, data, and reasoning are credible and compliant. A second appraisal is an independent value opinion on the same equipment, performed as a new assignment that produces its own conclusion of value.

The deciding factor is the nature of the dispute.

If the challenge targets how the original appraiser reached the conclusion (wrong approach, unsupported adjustments, missing USPAP elements, inadequate scope), an appraisal review is the correct instrument. The review appraiser evaluates whether a clear, defensible path exists from the data cited to the value concluded.

A review that exposes a logical break in that path is more persuasive in court or lender proceedings than a competing number, because it demonstrates the original report fails on its own terms.

If the challenge is that the original report's conclusion is simply wrong (the market has moved, the condition assessment missed a major deficiency, or the appraiser lacked access to transaction data that would materially change the result), a second independent appraisal is appropriate. The second appraiser produces a new value opinion using current data and a full scope of work, giving the challenging party an alternative conclusion to present alongside the original.

In some disputes, both are necessary.

An attorney preparing for litigation may commission a review to establish the original report's deficiencies and a second appraisal to provide the court with a credible alternative value. A lender reviewing collateral coverage may accept either path depending on internal policy.

Choosing correctly at the outset preserves the challenging party's budget and ensures the evidence produced matches the procedural standard that the reviewing body, court, or lender applies to resolve the dispute.

Steps to Formally Dispute an Equipment Appraisal

The formal dispute process follows five sequential steps, each building the evidentiary foundation for the next. Skipping steps (particularly documentation) weakens the challenge at every subsequent stage.

- Document the specific error. Identify which of the four dispute grounds applies (methodological error, inadequate data, USPAP non-compliance, or credential deficiency) and cite the exact page, paragraph, or exhibit in the report where the flaw appears. A written summary that quotes the report's own language and explains why it constitutes an error becomes the foundation for every action that follows.

- Request the appraiser's workfile. USPAP requires the appraiser to retain all data, calculations, and supporting documentation. Submit a written request to the appraiser or the party who commissioned the report. The workfile either confirms the documented error or reveals additional unsupported conclusions that strengthen the challenge.

- Commission the appropriate professional response. Based on the nature of the flaw, engage either an appraisal review (to evaluate the original report's compliance and credibility) or a second independent appraisal (to produce a competing value conclusion). In litigation or high-value disputes, both may be necessary.

- Submit the challenge through the correct channel. File the documented objection with the appropriate body: the lender's internal review desk for SBA or collateral disputes, the court for litigation, the insurance umpire process for policy claims, or the appraiser's credentialing organization (such as ASA) for ethical or competency complaints.

- Escalate if unresolved. If the initial channel does not produce a resolution, escalation paths include retaining legal counsel for court action, filing a formal ethics complaint with the appraiser's professional organization, or requesting a court-appointed appraiser in divorce and estate proceedings.

Each step generates a documented record. That record is what transforms a dispute from a disagreement about a number into an evidentiary challenge that lenders, courts, and review bodies are procedurally required to address.

FAQ

What is the difference between disputing an equipment appraisal and simply disagreeing with the value?

The main difference between disputing an equipment appraisal and disagreeing with the value is evidence. Disputing an appraisal challenges the method, data, condition assessment, or comparable sales used to reach the number. Simply disagreeing states that the value feels wrong but does not prove a specific appraisal error.

Can a lender reject a borrower's equipment appraisal, and what recourse does the borrower have?

Yes, a lender can reject a borrower’s equipment appraisal if the report uses weak comparables, outdated market data, unsupported assumptions, or an unqualified appraiser. A borrower’s recourse is to request the reasons in writing, submit a revised appraisal, provide stronger supporting market evidence, seek an internal review, or apply with another lender.

What does USPAP non-compliance look like in an equipment appraisal report?

USPAP non-compliance in an equipment appraisal report appears as missing scope of work, lack of signed certification, unsupported valuation methods, and inadequate data disclosure. Reports often omit assumptions, fail to identify intended use or users, or include biased conclusions. These violations reduce credibility and fail USPAP Standards Rules 7 and 8 requirements.

How do I request an appraiser's workfile, and what should I look for in it?

Request an equipment appraiser’s workfile in writing and identify the report, appraisal date, and intended review purpose. Ask for all data, notes, comparable sales, calculations, photos, limiting conditions, and certification support. Review the workfile for consistency with the report, support for value conclusions, source reliability, and signs of missing analysis or bias.

What is a Daubert motion, and how does it apply to challenging equipment appraisal testimony?

A Daubert motion challenges expert testimony by testing reliability, methodology, and relevance under Federal Rule of Evidence 702. In equipment appraisal cases, it excludes opinions that lack market support, use improper valuation methods, or fail USPAP standards. Courts assess data sufficiency, method application, error rates, and professional acceptance.