Equipment Appraisal for Divorce & Estate Proceedings

In divorce and estate proceedings, a certified equipment appraisal establishes the fair market value (FMV) of machinery, vehicles, and production assets as of a legally specified date. Courts, attorneys, and beneficiaries rely on this number to divide or distribute property.

Informal valuations and book values do not meet the evidentiary standard required in these proceedings. A credentialed appraisal that follows USPAP produces a figure that survives legal scrutiny.

Why Courts Require Certified Appraisals, Not Estimates

Courts, estate administrators, and opposing counsel require USPAP-compliant certified appraisals because informal valuations lack the methodological rigor and transparency needed to serve as evidence of value.

The legal standard in both divorce and estate proceedings is fair market value (FMV):

The price a willing buyer would pay a willing seller, both with reasonable knowledge of relevant facts, neither acting under compulsion.

Reaching that number requires documented research, defined methodology, and a credentialed appraiser who can defend the conclusion under cross-examination. Dealer quotes, online listings, and depreciation schedules meet none of those requirements.

Book value is the most common substitute parties attempt to use, and it is the least reliable. Tax depreciation schedules reflect accounting treatment dictated by IRS recovery periods, not market reality. A crawler excavator fully depreciated over five years on a balance sheet may still command $80,000–$120,000 at sale.

Dealer quotes reflect a single dealer's inventory position and margin expectations on a given day, not an arm's-length market transaction. Online listing prices represent asking prices, not closed sales, and carry no analytical framework explaining how the figure was derived.

A certified written appraisal report prepared under USPAP solves each of these problems.

USPAP governs equipment appraisal methodology selection, scope of work documentation, and report format. The report must identify the approaches to value considered, explain which were applied and why, disclose assumptions and limiting conditions, and state the effective date of the valuation.

This structure gives judges, attorneys, and the IRS a transparent chain of reasoning from raw data to final opinion of value. A report that cannot demonstrate this chain is vulnerable to exclusion or impeachment, which means the asset value it supports has no standing in the proceeding.

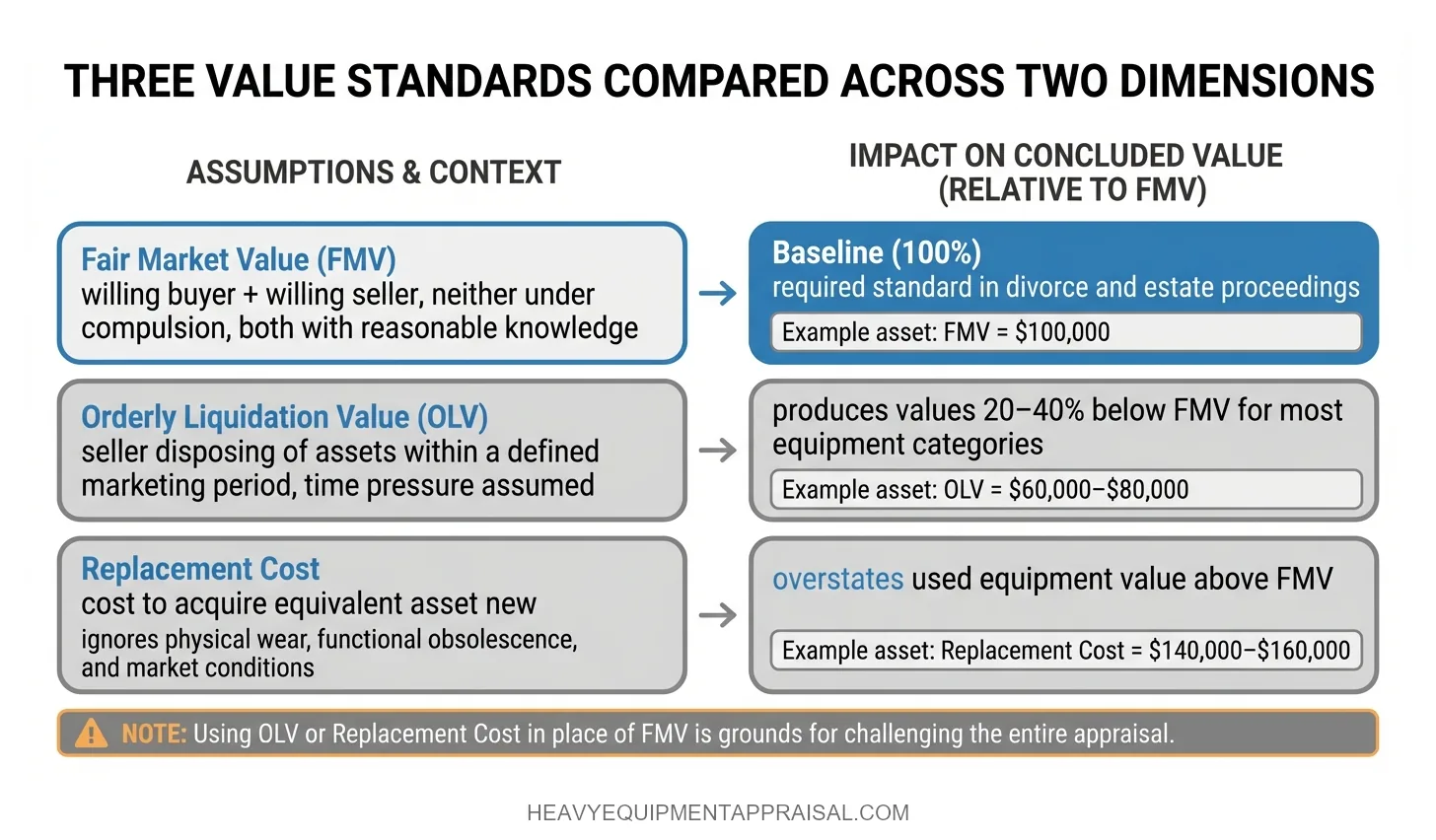

The Controlling Value Standard: Fair Market Value

Fair market value (FMV) is the required value standard in both divorce property division and estate asset distribution. FMV represents the price a willing buyer would pay a willing seller, both possessing reasonable knowledge of relevant facts, with neither party acting under compulsion to transact.

This definition is codified in IRS Revenue Ruling 59-60 for estate and gift tax purposes and adopted by family courts across both community property and equitable distribution jurisdictions.

FMV is not interchangeable with other value premises.

Orderly liquidation value (OLV) assumes a seller disposing of assets within a defined marketing period, typically under some degree of time pressure. That assumption produces values 20–40% below FMV for most equipment categories.

Replacement cost measures what it would take to acquire an equivalent asset new, which overstates the value of used equipment by ignoring physical wear, functional obsolescence, and economic conditions.

Courts applying either OLV or replacement cost in place of FMV would systematically undervalue or overvalue the marital or estate assets, distorting the distribution. The distinction between these value types is not academic. Using the wrong standard is grounds for challenging the entire appraisal.

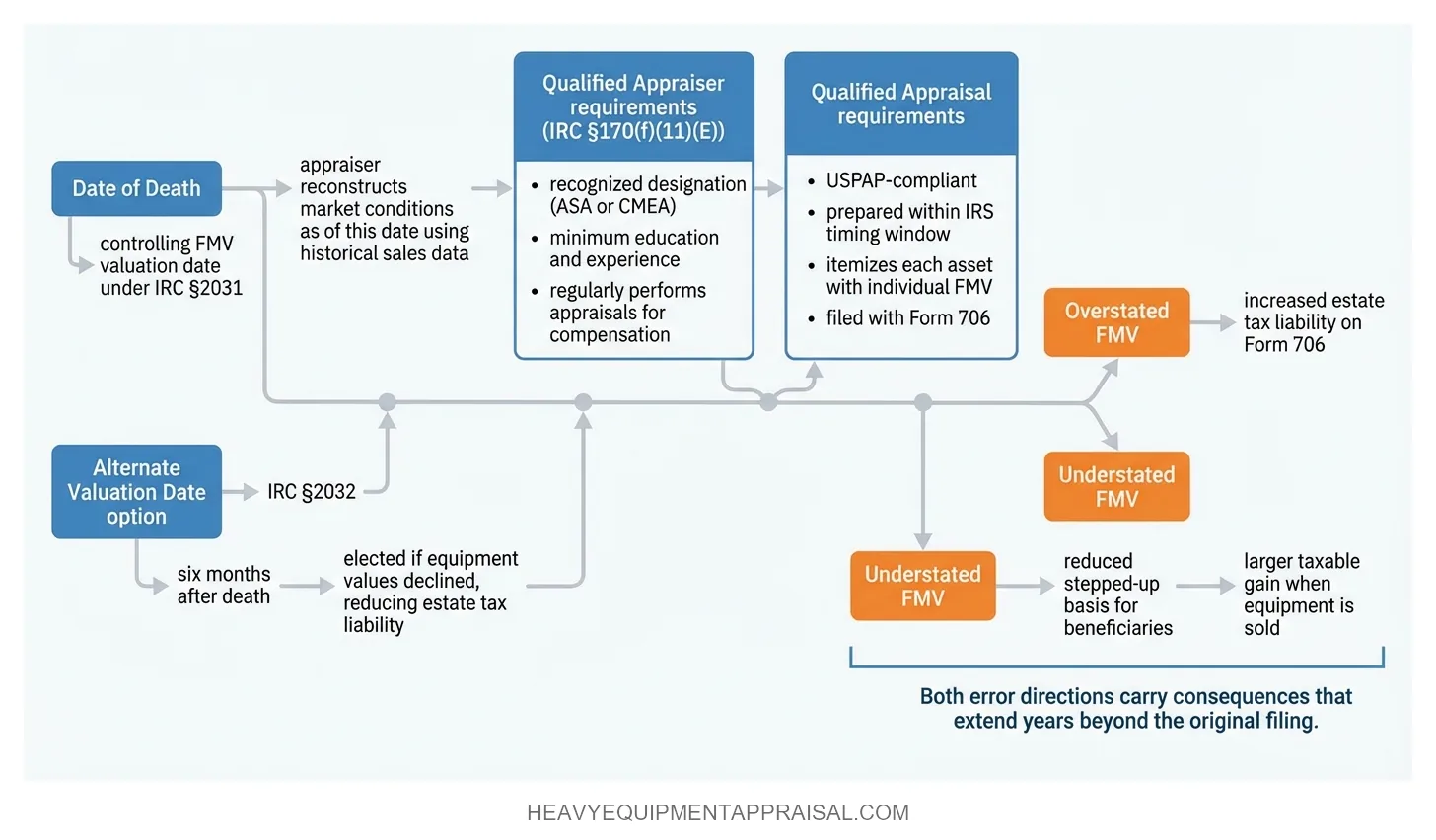

The effective date of the appraisal is equally critical. In estate proceedings, the controlling date is typically the decedent's date of death (or the alternate valuation date six months later, if elected under IRC §2032).

In divorce, jurisdiction determines whether the relevant date is the date of separation, the date of filing, or another milestone. Equipment values can shift meaningfully over a span of months. A motor grader worth $165,000 at separation may trade at $145,000 by trial.

The appraisal report must state the effective date explicitly and value the assets as of that date, because a mismatch between the court's controlling date and the appraiser's valuation date renders the opinion inapplicable to the proceeding.

Divorce Proceedings: Equitable Distribution and Community Property

The legal framework governing a state's divorce process determines which equipment assets are subject to valuation and how the appraised FMV translates into a division of property.

Community property states (nine states, including California, Texas, and Arizona) presume a 50/50 split of all assets acquired during the marriage.

Equitable distribution states (the remaining 41 states plus D.C.) divide marital property based on what the court deems fair, which may not be equal.

In both frameworks, the court needs an FMV figure for every piece of equipment classified as marital property before it can calculate a division or order a buyout.

The buyout scenario is where the appraisal carries the most direct financial consequence. When one spouse operates a business and intends to retain the equipment, the court orders that spouse to compensate the other for their share of the appraised value.

A fleet of dump trucks appraised at $420,000 in a community property state means one spouse owes the other $210,000 (or its equivalent in offset assets). In an equitable distribution state, the court has discretion to weight that figure based on factors like each party's contribution to the business, earning capacity, and overall asset pool. Either way, the FMV in the appraisal report is the starting number the court uses. An error of even 10% on a $420,000 fleet shifts $21,000 from one party to the other.

Parties can retain a single joint appraiser or hire separate appraisers who produce competing reports. A joint appraisal reduces cost and simplifies proceedings when both parties agree on the appraiser's independence and qualifications.

Dueling appraisals become necessary when the equipment is high-value, the parties dispute condition or usage, or one side questions the other's appraiser's objectivity. In contested cases, each appraiser may be called to testify as an expert witness and defend their methodology, data sources, and conclusions under cross-examination.

The appraiser's ability to articulate the reasoning behind the FMV opinion in court is what separates a report that influences the judge's decision from one that gets discounted during deliberation.

Estate Settlement: Date-of-Death Valuation and IRS Compliance

Estate tax compliance under IRC §2031 requires that all property includible in a decedent's gross estate be reported at fair market value as of the date of death. For estates that include machinery and equipment, this means the appraiser must produce a retrospective valuation reflecting market conditions on a specific past date, not the date the appraisal is performed.

The IRS treats this date-of-death FMV as the figure that determines both estate tax liability and the stepped-up cost basis inherited by beneficiaries.

The IRS imposes specific requirements on who can provide that valuation. Under IRC §170(f)(11)(E), a qualified appraiser must hold a recognized professional designation (such as ASA or CMEA), meet minimum education and experience thresholds, and regularly perform appraisals for compensation.

The appraisal itself must be a qualified appraisal: a USPAP-compliant document prepared no earlier than 60 days before the date of the contribution or death and no later than the due date of the return on which it is claimed.

For Form 706 (United States Estate Tax Return), the appraisal must accompany the filing and itemize each piece of equipment with its individual FMV.

Retrospective appraisals present a distinct analytical challenge. The appraiser must reconstruct market conditions as they existed on the valuation date, relying on comparable sales data, auction results, and dealer transaction records from that period.

Current market pricing is irrelevant.

If the decedent died eight months before the appraisal engagement begins, the appraiser needs access to historical sales comparison data from that window. Estates also have the option under IRC §2032 to elect an alternate valuation date six months after death, which can reduce tax liability if equipment values declined during that period.

Errors in estate equipment valuations carry compounding consequences. An overstated FMV increases the estate's tax liability on Form 706. An understated FMV reduces the beneficiaries' stepped-up basis, creating a larger taxable gain when the equipment is eventually sold. The IRS audits equipment values on estate returns by comparing reported figures against market data for the same asset class and vintage.

An appraisal that documents its data sources, methodology, and effective-date market analysis gives the estate executor a strong position if the return is examined. One that lacks this documentation invites adjustment, penalties, and potential litigation with consequences that extend years beyond the original filing.

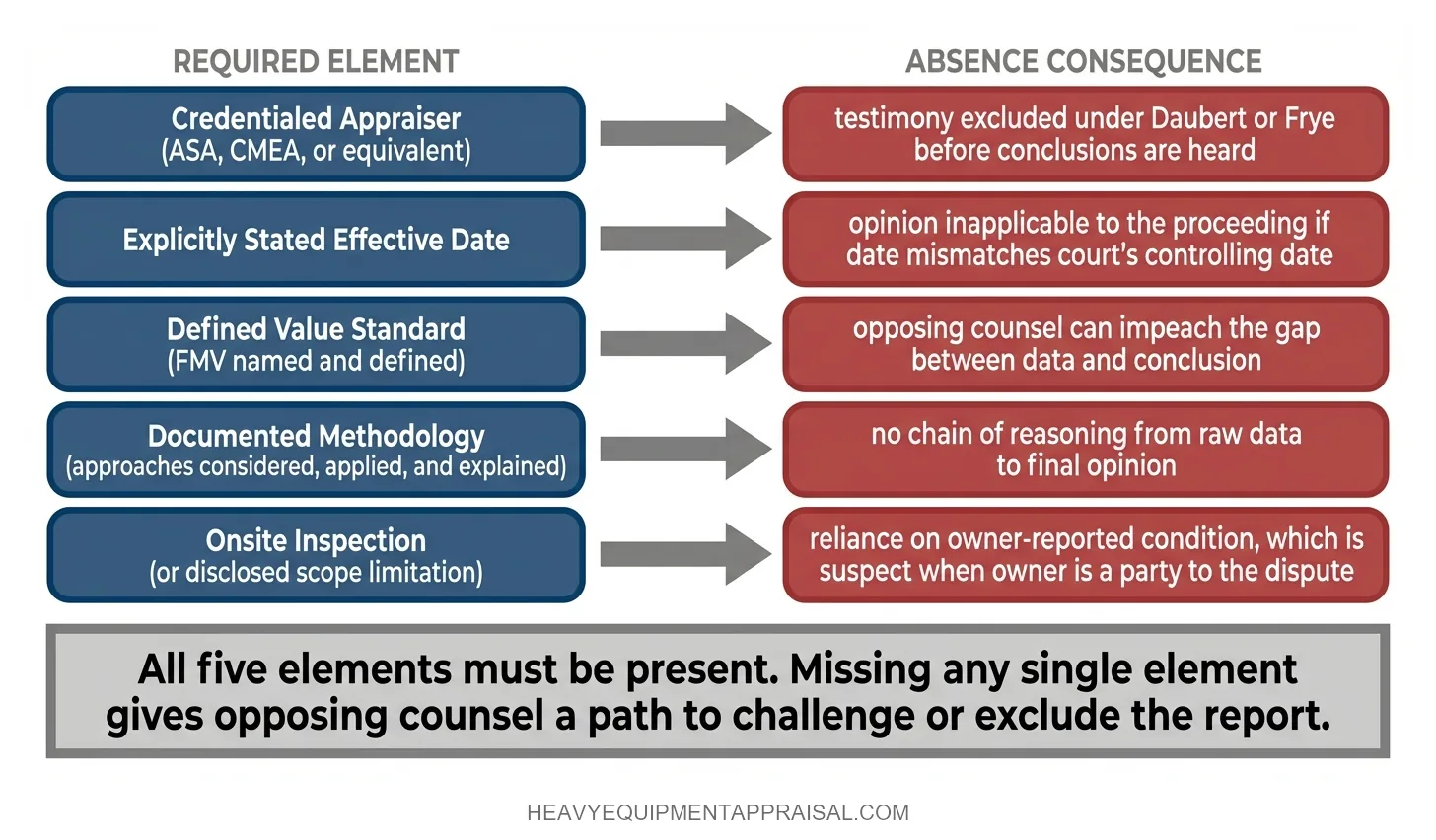

What Makes an Equipment Appraisal Legally Defensible

A legally defensible equipment appraisal contains five core elements: a credentialed appraiser, an explicitly stated effective date, a defined value standard, documented methodology, and an onsite inspection (or a disclosed scope limitation explaining why one was not performed). Missing any single element gives opposing counsel a path to challenge or exclude the report.

Appraiser credentials establish the expert's standing to offer an opinion of value. Courts evaluate whether the appraiser holds a recognized professional designation (ASA, CMEA, or equivalent), meets minimum experience thresholds, and regularly performs equipment appraisals for compensation.

An appraiser who cannot demonstrate these qualifications risks having their testimony excluded under Daubert or Frye standards before the report's conclusions are even discussed.

Value definition and methodology form the analytical backbone of the report. The appraisal must name the value standard applied (FMV in divorce and estate contexts), define it, and identify which approaches to value were considered and why.

A report that states a number without showing how it was derived offers opposing counsel a straightforward impeachment target: the appraiser cannot explain the gap between data and conclusion.

Onsite inspection carries particular weight in adversarial proceedings. Physical verification of condition, installed configuration, and operating status eliminates reliance on owner-reported information, which is inherently suspect when the owner is a party to the dispute.

A desktop appraisal may be appropriate for low-value assets or uncontested items, but the scope limitation must be disclosed in the report.

Appraiser independence is the element most frequently attacked in contested cases. Divorce proceedings and estate disputes are adversarial by nature.

Professional ethics standards prohibit an appraiser from acting as an advocate for either party. An appraiser who has a financial relationship with one side, or whose compensation is contingent on the outcome, produces a report that is disqualified on its face. Independence is not a formality. It is the foundation that allows the court to treat the appraisal as objective evidence rather than partisan argument.

Documents Needed for a Divorce or Estate Appraisal

The appraiser's concluded value is only as reliable as the documentation supporting it. In divorce and estate engagements, the following records form the evidentiary foundation of the appraisal.

Original Purchase Records: Invoices, bills of sale, and purchase agreements establish acquisition cost, date of purchase, and original specifications. These anchor the cost approach and confirm whether an asset falls within the marital or estate period.

Maintenance and Repair Records: Service logs, rebuild receipts, and component replacement records directly affect the appraiser's condition assessment. A wheel loader with a documented engine overhaul at 8,000 hours retains materially more value than an identical unit with no service history. When maintenance records are absent, the appraiser must assume average or below-average condition, which typically reduces the concluded FMV.

Equipment Lists and Fixed Asset Schedules: A complete inventory with make, model, serial number, year, and hour meter readings gives the appraiser the baseline dataset. Fixed asset schedules from accounting records help identify assets that may have been overlooked or misclassified.

Title and Registration Documents: For titled assets (trucks, trailers, registered vehicles), these confirm ownership, lien status, and VIN-level identification.

Lease and Financing Agreements: Any active leases or loan documents clarify whether the asset is owned, financed, or leased. Only owned equity is subject to division or inclusion in the gross estate.

Prior Appraisals or Insurance Valuations: Earlier appraisal reports provide historical reference points and may reveal modifications or upgrades not captured elsewhere.

When documentation gaps exist, the appraiser does NOT stop the engagement. The appraiser discloses the missing records as a scope limitation in the report, relies on physical inspection findings and comparable market data, and applies conservative assumptions where owner-provided information cannot be verified.

The strength of the final report correlates directly with the completeness of the supporting documentation, because every gap the appraiser must bridge with assumptions is a point opposing counsel can probe during cross-examination.

When One Appraisal Isn't Enough: Disputes and Second Opinions

Divergent appraisals are common in contested divorce and estate proceedings, and the gap between two credentialed opinions on the same equipment can exceed 15–20% when appraisers apply different comparable sales, make different condition assumptions, or weight the approaches to value differently. That divergence does not automatically invalidate either report. It triggers a process for resolving the difference.

Grounds for challenging an opposing appraisal fall into three categories: methodology errors, factual errors, and independence failures. A methodology challenge targets the appraiser's selection or application of valuation approaches.

If an opposing report relies solely on the cost approach for assets with an active resale market and ignores available sales comparison data, that omission is a substantive deficiency.

A factual challenge targets incorrect equipment specifications, misidentified models, or hour meter readings that contradict maintenance logs. An independence challenge targets the appraiser's relationship with the retaining party or any compensation structure tied to the outcome. Each category gives an attorney a distinct line of cross-examination.

Courts can appoint a neutral appraiser when competing reports produce irreconcilable conclusions. The neutral appraiser conducts an independent engagement under the court's direction, producing a third opinion that carries no presumption of advocacy for either side. Judges in equitable distribution states have broad discretion to adopt, reject, or blend any of the competing valuations.

An appraisal review is a more targeted litigation tool.

Rather than producing a new opinion of value, a review appraiser examines the opposing report for USPAP compliance, methodological soundness, and data accuracy. The review identifies specific deficiencies without requiring a full re-inspection of the equipment.

Attorneys use review reports to narrow the issues in dispute, focusing the court's attention on where and why the competing opinions diverge rather than asking the judge to choose between two complete but conflicting conclusions.

FAQ

What is the difference between fair market value and book value for equipment in a divorce?

The main difference between fair market value and book value for equipment in a divorce is that fair market value reflects the current resale price in an open market, while book value reflects historical cost minus depreciation on financial statements. Courts rely on fair market value to divide assets accurately.

Does equipment appraisal follow different rules in community property states versus equitable distribution states?

The main difference between equipment appraisal rules in community property states and equitable distribution states is how courts apply the appraised value. Appraisal methods follow the same standards such as USPAP, but community property states split assets 50/50, while equitable distribution states divide assets based on fairness factors.

What date should an equipment appraisal use for an estate tax return?

An equipment appraisal for an estate tax return should use the date of death as the valuation date under IRS rules. Executors may elect an alternate valuation date six months after death under IRC Section 2032 if it reduces estate taxes. The chosen date must apply to all estate assets consistently.

Can the IRS reject an equipment appraisal filed with Form 706?

The IRS can reject an equipment appraisal filed with Form 706 if the valuation lacks support, uses improper methods, or fails to follow fair market value standards. The IRS may adjust values, request additional documentation, or impose penalties if the appraisal understates asset values or lacks a qualified appraiser.

What credentials must an appraiser have for a court-admissible equipment valuation?

An appraiser for a court-admissible equipment valuation must qualify as an expert witness and follow USPAP standards. Courts prefer credentials such as ASA or CMEA, along with 5–10 years of relevant valuation experience. The appraiser must demonstrate independence, reliable methodology, and the ability to defend the valuation under testimony.

What happens when two appraisers produce different values for the same equipment in a divorce case?

When two appraisers produce different values in a divorce case, the court evaluates both reports and determines the most credible valuation. Judges weigh methodology, assumptions, and appraiser credentials. Courts may average values, select one appraisal, or appoint a third independent appraiser to resolve the discrepancy.

Is an onsite inspection always required for a divorce or estate equipment appraisal?

An onsite inspection is not always required for a divorce or estate equipment appraisal. Appraisers can perform desktop appraisals using photos, asset lists, and records when data is reliable. Courts and the IRS prefer onsite inspections for high-value or disputed assets to ensure accuracy and credibility.

What documents should I gather before hiring an equipment appraiser for estate settlement?

Gather equipment lists, purchase invoices, depreciation schedules, prior appraisals, and maintenance records before hiring an equipment appraiser for estate settlement. Include photos, serial numbers, and location details. Provide estate documents such as the date of death and Form 706 requirements to ensure accurate fair market valuation.

What is an appraisal review and how does it differ from a second opinion?

The main difference between an appraisal review and a second opinion is that an appraisal review evaluates the quality, methodology, and compliance of an existing report, while a second opinion provides an independent valuation. Reviews assess accuracy and USPAP compliance, while second opinions generate a new value conclusion.

How does the alternate valuation date under IRC §2032 affect an estate equipment appraisal?

The alternate valuation date under IRC §2032 requires the equipment appraisal to use fair market value as of six months after the date of death instead of the date of death. This election can reduce estate taxes if asset values decline, and the chosen date must apply consistently to all estate assets.