Desktop vs Onsite Equipment Appraisal: Key Differences

The main difference between desktop and onsite equipment appraisal is location and inspection depth. A desktop equipment appraisal uses records, and market data, and sometimes photos without visiting the asset. An onsite equipment appraisal includes a physical inspection, condition verification, and more precise valuation for financing, insurance, litigation, or sale decisions.

*Photos are not a USPAP requirement.

Desktop and onsite equipment appraisals differ in one fundamental way: whether the appraiser physically inspects the asset. That distinction controls the credibility of the value opinion, the standards it can support, and whether it holds up under lender, IRS, or legal scrutiny.

Both methods operate within USPAP’s scope-of-work framework, but keep reading because choosing the wrong one for a given use case can invalidate the appraisal entirely.

What a Desktop Equipment Appraisal Is

A desktop equipment appraisal is an opinion of value developed without the appraiser physically inspecting the equipment. The appraiser works from client-submitted documentation and external market data, applying the same valuation methodologies used in any appraisal but without independent verification of the asset’s physical condition.

This approach is sometimes called a “limited-scope” or “restricted” appraisal, though neither term is synonymous with lower quality. It means the appraiser’s conclusion rests on a narrower evidence base.

Typical inputs for a desktop appraisal include:

- Manufacturer name

- Model number

- Serial number

- Year of manufacture

- Yours or mileage

- Size and capacity specifications

- Client-submitted photographs

The appraiser cross-references these details against market databases, comparable sales records, and published cost data to develop the value opinion. Maintenance records and repair history, when provided, strengthen the analysis. The documents the client prepares directly shape the appraiser’s ability to reach a credible conclusion.

The critical distinction is what the appraiser certifies.

In a desktop appraisal, the appraiser certifies that the value opinion is based on the information provided and the market data analyzed. The appraiser does not certify the equipment’s physical condition, operational status, or the absence of damage, modifications, or undisclosed wear. Any of those factors, if misrepresented or omitted, can materially affect accuracy.

USPAP’s Scope of Work Rule requires the appraiser to disclose the limited nature of the inspection (or its absence) and to determine that the restricted scope still produces credible results for the intended use. If the appraiser concludes that a desktop scope is insufficient for the assignment’s purpose, the appraiser must either expand the scope or withdraw. This disclosure requirement exists to protect all parties relying on the report.

The value conclusion from a desktop appraisal is only as reliable as the documentation behind it. Undisclosed damage, hidden wear, or missing maintenance history can cause the reported value to be materially overstated, a risk that compounds when the appraisal supports lending or litigation decisions.

What an Onsite Equipment Appraisal Is

An onsite equipment appraisal includes a physical inspection of the equipment by the appraiser, enabling direct assessment of condition, operational status, and factors that documentation alone cannot reveal. The appraiser travels to the asset’s location and conducts a visual examination, recording objective data points that form the evidentiary foundation for the condition rating and, ultimately, the value conclusion.

During a physical inspection, the appraiser typically:

- Records hour meter or odometer readings

- Photographs the asset from multiple angles

- Evaluates visible wear on structural components and high-stress areas

- Checks for fluid leaks or corrosion

- Notes the condition of attachments and auxiliary systems

- Identifies any modifications, aftermarket additions, or missing components

Serial numbers and nameplates are verified against the client’s records. The appraiser also documents environmental and operational context: how the equipment is stored, whether it appears actively deployed, and whether the surrounding facility suggests routine maintenance practices.

One common misconception is that “onsite” means the appraiser runs the machine. In standard practice, an onsite inspection is a visual inspection, not an operational test.

The appraiser observes physical evidence of condition but does not start, operate, or load-test the equipment unless the scope of work explicitly calls for functional testing. Some assignments for high-value process equipment or specialized assets do include operational verification, but that expanded scope is defined in the engagement letter before the inspection begins.

The inspection findings translate directly into a condition rating. Appraisers use defined condition scales (ranging from excellent to scrap) that correspond to specific physical criteria.

A machine documented with 12,000 hours, moderate hydraulic wear, and intact structural members receives a different rating than a comparable unit with the same hours but cracked welds and a bypassed safety system. That rating then informs the depreciation calculation within the cost approach or the comparability adjustments within the sales comparison approach.

Physical inspection gives the appraiser’s condition rating independent evidentiary support, which determines whether the final report can withstand challenge from a lender, opposing counsel, or a regulatory reviewer.

How Scope of Work Governs the Choice

USPAP’s Scope of Work Rule requires the appraiser to determine, before beginning the assignment, whether the planned level of inspection will produce a credible result for the intended use.

The rule does not mandate onsite inspection for every assignment.

It mandates that the appraiser evaluate whether omitting physical inspection introduces enough uncertainty to undermine the value conclusion’s credibility. That evaluation, and its rationale, must be documented in the report.

The Scope of Work Rule operates on a principle of sufficiency, not preference. An appraiser accepting an assignment for SBA lending collateral on a 15-year-old crawler crane with no recent service records cannot credibly conclude that a desktop scope is sufficient. The condition uncertainty is too high, and the intended use (loan underwriting) demands a defensible opinion.

By contrast, a fleet of 2-year-old over-the-road trucks with verified telematics data and manufacturer maintenance logs may present low enough condition risk for a desktop approach to satisfy both the appraiser’s professional judgment and the lender’s requirements.

When physical inspection is omitted, USPAP requires specific disclosures: that the appraiser did not inspect the property, that the value opinion is based on information provided by others, and that the appraiser assumes the accuracy of that information.

These disclosures are not optional qualifiers.

They define the evidentiary boundaries of the report. A report that omits inspection without these disclosures violates the standard, regardless of how accurate the value conclusion turns out to be.

The scope decision also constrains which value types the report can credibly support. A desktop appraisal concluding fair market value in continued use for equipment the appraiser has never seen carries an inherent credibility gap that no amount of market data can close. Scope of work is the compliance mechanism that determines whether the appraisal report is accepted or rejected by its intended audience.

When Desktop Appraisals Are Appropriate

Desktop appraisals fit assignments where condition uncertainty is low and the stakes do not demand independent physical verification. The common thread across valid desktop use cases is that the equipment is either:

- Well-documented

- Relatively new

- Low in individual value

- Being appraised for a purpose that tolerates the narrower evidence base

Virtual appraisals, where the appraiser views equipment via live video or high-resolution imagery submitted in real time, generally fall within the desktop category because the appraiser still relies on the client to facilitate access rather than conducting an independent physical inspection.

| Use Case | Why Desktop Works |

|---|---|

| Preliminary due diligence | Provides a defensible range before committing to full engagement costs |

| Low-value or commodity assets | Cost of onsite inspection may exceed a meaningful percentage of asset value |

| Portfolio or fleet reviews | Large asset counts with standardized equipment and telematics data reduce per-unit condition risk |

| Insurance renewals for newer equipment | Manufacturer specs and verified service records supply the data an appraiser needs when physical deterioration is minimal |

| Refinancing with recent prior inspection | An onsite appraisal completed within the prior 12–24 months anchors condition data that a desktop update can refresh against current market comps |

Cost and turnaround differences between desktop and onsite work are real but secondary to the scope decision. Desktop appraisals typically cost 30–50% less than onsite engagements and deliver in days rather than weeks, largely because they eliminate travel time, site coordination, and the labor of physical documentation. Those savings matter most when multiplied across a large fleet or when a transaction timeline is compressed.

The deciding factor is not budget.

It is whether the appraiser can reach a credible conclusion without seeing the asset. A 3-year-old motor grader with 2,000 hours and a complete dealer service history presents a different risk profile than a 20-year-old hydraulic press with no records.

The first may be a clear candidate for desktop valuation. The second almost certainly is not.

Matching the appraisal method to the assignment’s intended use controls whether the resulting report carries weight with the party relying on it, or gets returned as insufficient.

When Onsite Appraisals Are Required

Certain use cases mandate or strongly favor physical inspection because the intended audience will reject a value opinion that lacks independent condition verification. These are not situations where onsite is merely preferable. They are situations where a desktop appraisal creates regulatory, legal, or financial exposure for the party relying on the report.

SBA lending above collateral thresholds: SBA Standard Operating Procedures require a certified appraisal with physical inspection for machinery and equipment collateral above specified dollar thresholds. A desktop report submitted for an SBA 7(a) or 504 loan that exceeds those thresholds will be returned by the lender’s credit department before it reaches underwriting.

IRS charitable donation deductions: The IRS requires a qualified appraisal for noncash charitable contributions exceeding $5,000, and the appraiser must describe the property’s physical condition. A desktop opinion that omits condition verification exposes the donor to disallowance of the deduction and potential penalties. IRS scrutiny of equipment appraisals for tax purposes focuses heavily on whether the appraiser had sufficient basis to assess condition.

Litigation and divorce proceedings: Courts expect appraisers to testify to what they observed, not what someone told them. In divorce and estate disputes, opposing counsel will challenge a desktop opinion by asking whether the appraiser personally verified the asset’s existence and condition. A report built on unverified client data is a weak exhibit.

M&A purchase price allocation: Buyers allocating purchase price across tangible assets under ASC 805 need defensible fair values that auditors will accept. A desktop appraisal covering a production facility with hundreds of assets and no recent inspection history introduces audit risk that most accounting firms will not tolerate.

High-inspection-risk equipment categories also push assignments toward onsite regardless of use case. Marine assets, process plant equipment with integrated piping systems, older CNC machinery, and any asset with complex hydraulic or electrical systems present condition variables that photographs and spec sheets cannot capture.

The consequences of using a desktop appraisal where onsite inspection was warranted range from lender rejection and IRS disallowance to excluded testimony and restated financials. Each of those outcomes costs more than the inspection would have.

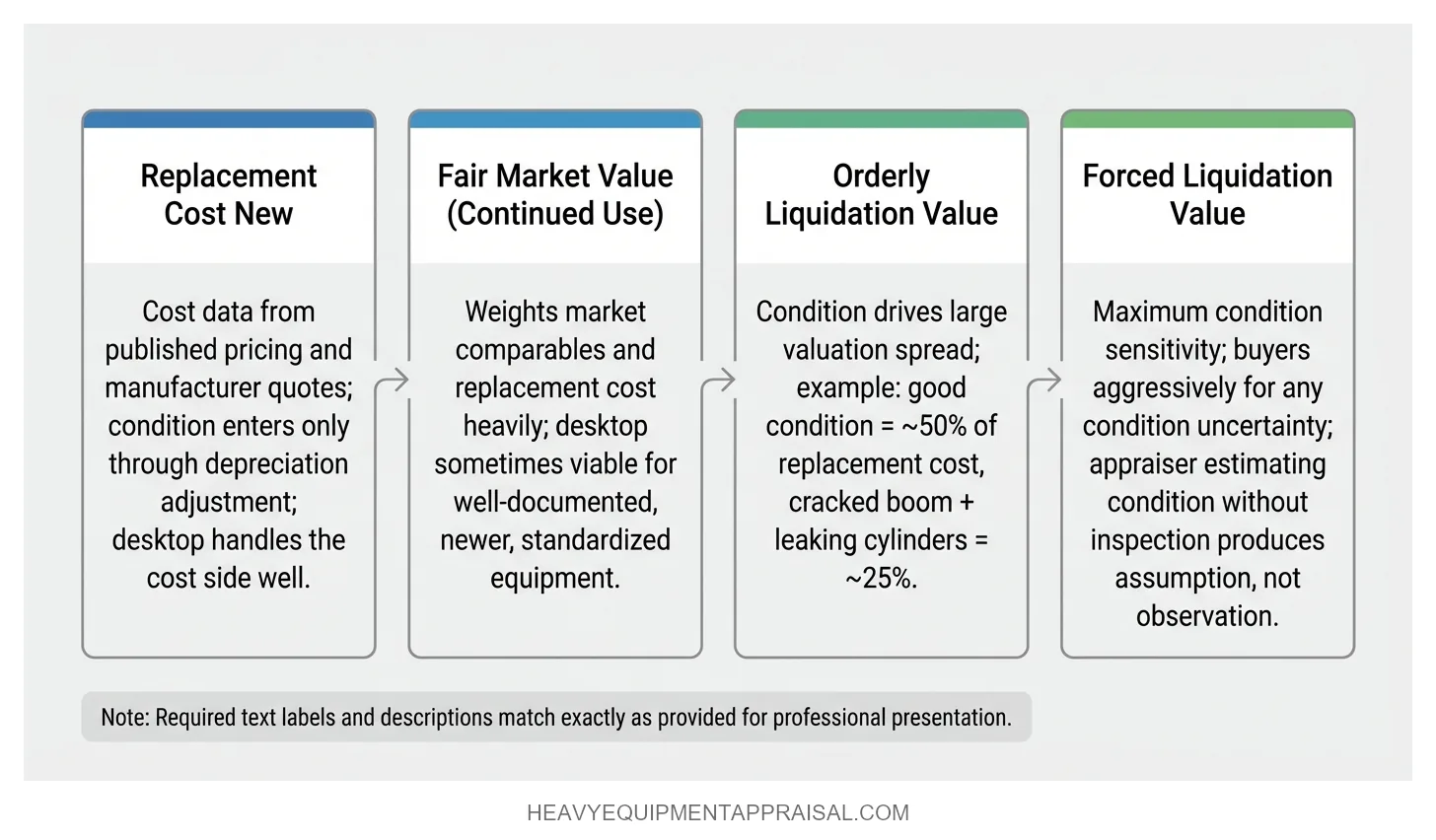

How Value Type Interacts with Appraisal Method

The value standard an appraiser develops directly constrains whether a desktop approach can credibly support the conclusion. Fair market value, orderly liquidation value, and forced liquidation value each carry different sensitivity to physical condition, and that sensitivity determines how much the appraisal depends on firsthand inspection data.

FMV in continued use assumes the equipment is operational and maintained in its current application. Condition still matters, but FMV calculations weight market comparables and replacement cost data heavily. A desktop approach can sometimes support an FMV conclusion when the asset is well-documented, relatively new, and operating in a standardized application. The appraiser's reliance on client-submitted data is partially offset by the availability of robust market comps for common equipment types.

OLV and FLV are far more condition-dependent.

Both liquidation value types model what a buyer would pay under sale pressure, and buyers in those scenarios discount aggressively for any condition uncertainty. A deferred-maintenance hydraulic excavator might return 50% of its replacement cost under OLV in good condition but only 25% with a cracked boom and leaking cylinders. That spread is invisible in a spec sheet. An appraiser concluding OLV or FLV without physical inspection is estimating the very factor (condition) that drives the largest variable in the calculation. The result is a value opinion built on an assumption rather than an observation.

Replacement cost new, used in the cost approach, presents the opposite profile.

The cost figure itself comes from published pricing data and manufacturer quotes, not from inspecting the subject asset. Condition enters only when the appraiser applies depreciation to arrive at a depreciated replacement cost. Desktop methods handle the cost side well but still require credible condition data for the depreciation adjustment.

The practical implication: as the value standard moves from replacement cost toward forced liquidation, the minimum credible inspection level moves from desktop toward onsite.

An appraiser who recognizes this relationship selects the right scope before the engagement begins, reducing the risk that the completed report fails to support the value type it purports to conclude.

What the Appraisal Report Looks Like for Each Method

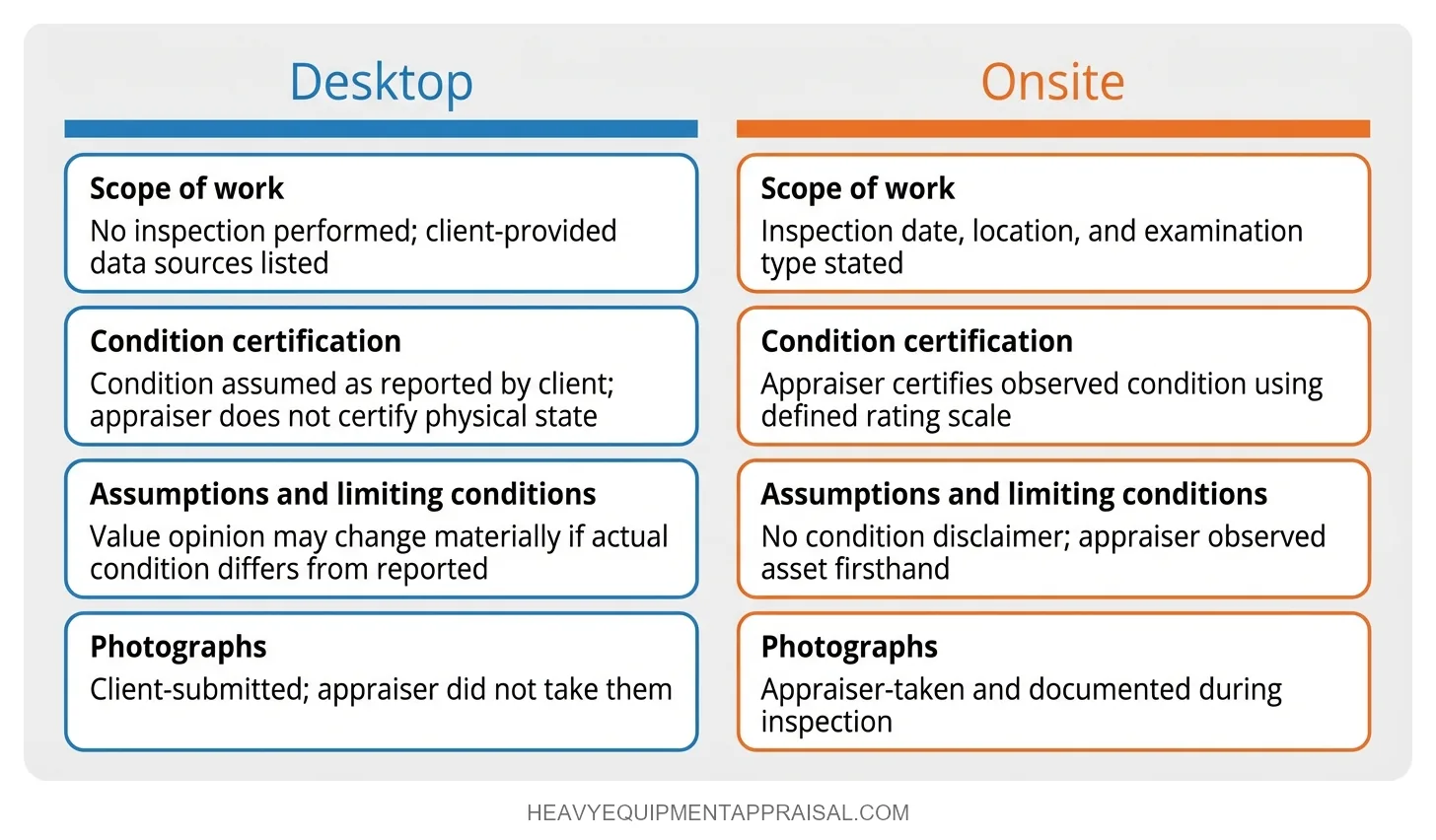

The clearest differences between a desktop and an onsite appraisal report appear in three sections:

- The scope of work disclosure

- The condition certification language

- The assumptions and limiting conditions

A lender, attorney, or IRS reviewer can identify which method was used, and what the appraiser is actually standing behind, by reading these three sections alone.

The scope of work disclosure states whether the appraiser inspected the property and, if not, what information sources replaced physical observation. In a desktop report, this section will include language such as "the appraiser did not conduct a physical inspection of the subject property" and will identify the client-submitted documents, photographs, and market databases relied upon. An onsite report states the date of inspection, the location, and the extent of the examination (visual only, or visual plus functional testing). This disclosure is not boilerplate. It defines the evidentiary boundary of everything that follows.

| Report Element | Desktop Report | Onsite Report |

|---|---|---|

| Scope of work | States no inspection was performed, lists client-provided data sources | States inspection date, location, and examination type |

| Condition certification | Assumes condition as reported by client, appraiser does not certify physical state | Appraiser certifies observed condition based on defined rating scale |

| Assumptions and limiting conditions | Includes explicit assumption that client-provided information is accurate and complete | May include standard limiting conditions but does not disclaim condition verification |

| Photographs | Client-submitted (if any), appraiser did not take them | Appraiser-taken, documented during inspection |

The assumptions and limiting conditions section is where the risk allocation lives. A desktop report's limiting conditions will state that the appraiser assumes the accuracy of all information provided and that the value opinion could change materially if the actual condition differs from what was reported. An onsite report carries no equivalent disclaimer for condition, because the appraiser observed the asset firsthand.

Reviewers who understand these distinctions can assess report reliability before ever reaching the value conclusion. A report that lacks clear scope disclosure or uses ambiguous condition language raises questions about whether the appraiser followed USPAP's documentation requirements, which in turn determines whether the report can serve as credible evidence in the proceeding or transaction it was commissioned to support.

Choosing the Right Method for the Intended Use

The intended use of the appraisal report dictates the inspection method, not the other way around. Starting from budget or turnaround preferences and working backward to justify a scope produces reports that fail when they reach the audience that matters.

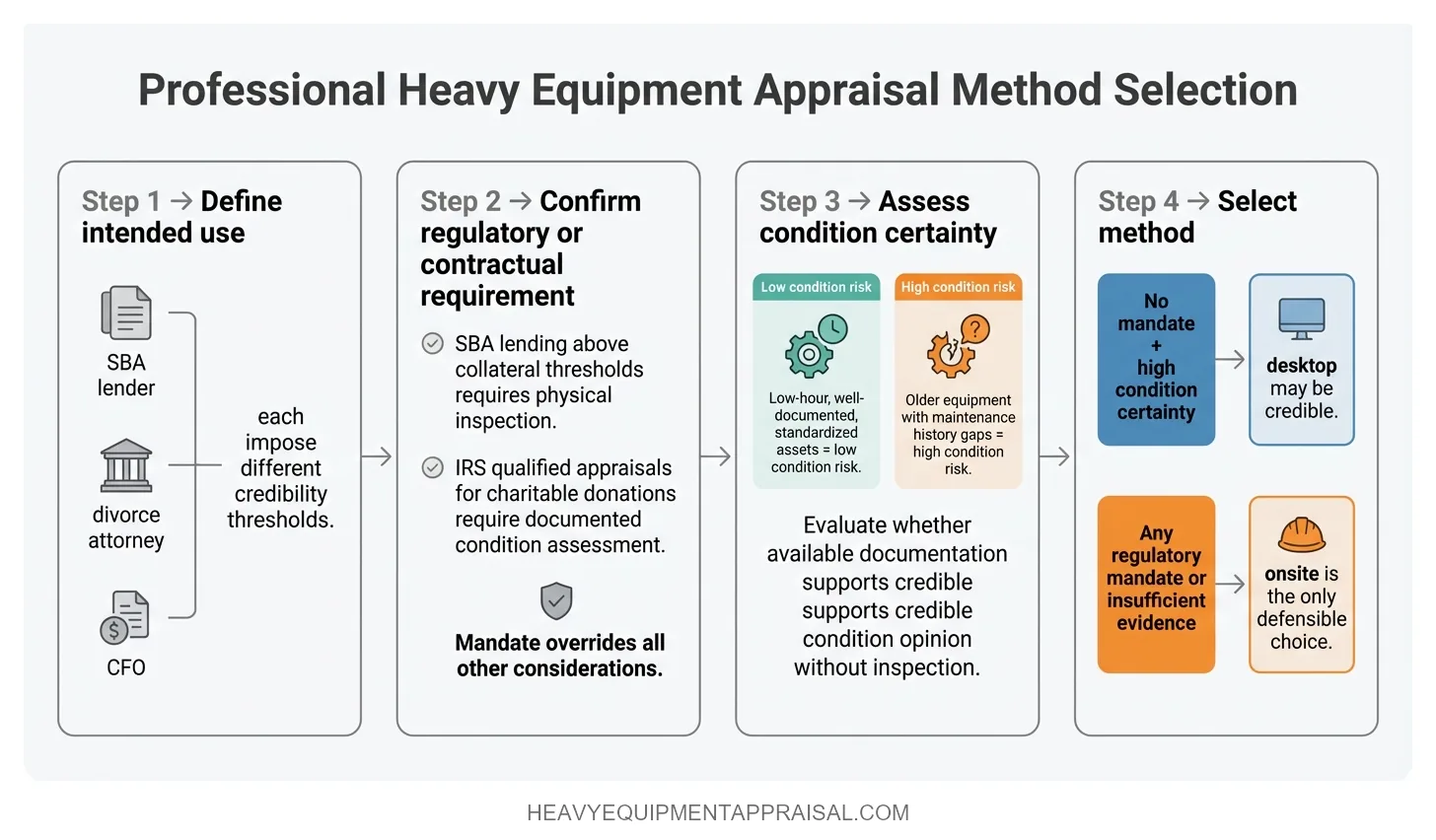

The correct sequence is a four-step decision process:

- Define the intended use. Identify who will rely on the report and for what purpose. An SBA lender underwriting a $500,000 equipment loan, a divorce attorney introducing exhibits in a contested proceeding, and a CFO refreshing an internal asset register each impose different credibility thresholds on the appraisal.

- Confirm any regulatory or contractual requirement. Check whether the intended use carries a mandated inspection level. SBA lending above collateral thresholds requires physical inspection. IRS qualified appraisals for charitable donations require documented condition assessment. If a mandate exists, it overrides all other considerations.

- Assess condition certainty. Evaluate whether the available documentation (service records, telematics, recent photographs, prior inspection reports) gives the appraiser enough evidence to form a credible condition opinion without physical inspection. Low-hour, well-documented assets with standardized configurations present low risk. Older equipment with gaps in maintenance history does not.

- Select the method that satisfies steps 1–3. If no regulatory mandate exists and condition certainty is high, a desktop approach may produce a credible result. If any step reveals insufficient evidence or an audience that will demand independent verification, onsite inspection is the only defensible choice.

Treating this sequence as non-negotiable prevents the most common and costly error in equipment appraisal engagements: selecting a method that produces a technically sound value opinion no one will accept.

The report's usefulness depends entirely on whether the scope aligns with the qualifications and expectations of the party who commissioned it and the party who must rely on it.

FAQ

What is the difference between a desktop and an onsite equipment appraisal?

The main difference between desktop and onsite equipment appraisal is location and inspection depth. A desktop equipment appraisal uses records, and market data, and sometimes photos* without visiting the asset. An onsite equipment appraisal includes a physical inspection, condition verification, and more precise valuation for financing, insurance, litigation, or sale decisions.

When does the SBA require a physical inspection for an equipment appraisal?

The SBA generally requires a physical inspection for an equipment appraisal when the equipment is used, specialized, or high value and a desktop review cannot reliably confirm condition, existence, and market value. SBA lenders should verify the exact trigger in the current SBA SOP because thresholds and documentation standards can change.

Can a desktop appraisal be used for an IRS charitable donation deduction?

A desktop appraisal can support an IRS charitable donation deduction only in limited cases. For most noncash charitable contributions that require a qualified appraisal, the IRS expects a qualified appraiser to perform a complete appraisal that credibly identifies the property, its condition, and fair market value.

How does equipment condition affect whether a desktop appraisal is credible?

Equipment condition affects desktop appraisal credibility by determining how reliably records, photos, and market data reflect actual value. A desktop appraisal is more credible when the equipment is new, well documented, standardized, and in known working condition. Credibility drops when condition is uncertain, damage is possible, or wear materially changes market value.

What does USPAP require when an appraiser skips physical inspection?

USPAP does not automatically require a physical inspection in every appraisal assignment. USPAP requires the appraiser to identify the assignment conditions, develop a credible appraisal, disclose the scope of work, and explain any extraordinary assumptions or limiting conditions when no physical inspection occurs. Credibility must match the intended use.

Is a desktop equipment appraisal acceptable for litigation or divorce proceedings?

A desktop equipment appraisal can be acceptable for litigation or divorce proceedings when the court, attorneys, and intended use accept a report based on documents, photos, and market data. Acceptance drops when equipment condition, identity, or ownership is disputed. In contested cases, a physical inspection usually produces a more credible and defensible opinion.

How do orderly liquidation value and forced liquidation value differ from fair market value in terms of inspection requirements?

Orderly liquidation value, forced liquidation value, and fair market value differ in inspection requirements because liquidation appraisals depend more heavily on actual condition, removability, and sale constraints. Fair market value can sometimes rely on records and market data. Orderly and forced liquidation values usually require stronger inspection support because condition and disposition timing directly affect recoverable price.

What should an equipment appraisal report disclose if no physical inspection was performed?

An equipment appraisal report should disclose that no physical inspection was performed, identify the information sources used, state the scope of work, and explain any extraordinary assumptions or limiting conditions. The report should also describe how the lack of inspection affects reliability, condition analysis, and the intended use of the value conclusion.

How much less does a desktop appraisal cost compared to an onsite appraisal?

A desktop appraisal usually costs 30% to 50% less than an onsite appraisal because it avoids travel, site time, and hands-on inspection. Cost savings shrink when the assignment involves complex equipment, weak documentation, or urgent turnaround. Final pricing depends on equipment count, location, report scope, and intended use.

Can a virtual or video-based equipment appraisal substitute for an onsite inspection?

A virtual or video-based equipment appraisal can substitute for an onsite inspection when the appraiser can reliably verify identity, condition, quantity, and relevant features through live video, clear images, records, and supporting documents. It does not fully replace onsite inspection when damage, wear, access limits, or disputed facts reduce credibility.