Equipment Blue Book vs Certified Appraisal: Key Differences

The main difference between Equipment Blue Book and a certified equipment appraisal is that Blue Book gives general price guidance, while a certified appraisal delivers a formal, asset-specific opinion of value that carries more weight in lending, tax, and litigation matters.

Equipment blue book tools estimate price ranges based on make, model, year, and hours. A certified appraisal produces a USPAP-compliant, appraiser-signed opinion of value that accounts for actual condition, configuration, attachments, and regional market demand. Blue book values work for rough screening. Certified appraisals hold up in lending, tax, insurance, and litigation contexts where a supportable number is required.

The two serve different purposes and are not interchangeable.

What “Equipment Blue Book” Actually Means

“Blue book” is not a single product. It is a colloquial term for automated pricing reference tools that return estimated equipment values based on a narrow set of inputs: make, model, year, and operating hours. Some tools add a broad condition tier (good, fair, poor). None involve an appraiser, a physical inspection, or professional judgment applied to a specific asset.

The major platforms in this category include EquipmentWatch (owned by Informa), Sandhills Global (which operates Machinery Trader, TractorHouse, and related listing sites), and various manufacturer residual value guides published for dealer networks.

Each platform builds its dataset differently.

EquipmentWatch aggregates auction results, dealer asking prices, and rental rate data into statistical models. Sandhills Global draws primarily from its own listing and transaction platforms, capturing asking prices and, in some cases, closed sale figures across thousands of equipment categories. Manufacturer residual guides use internal sales data and fleet return histories to project future values for financing purposes.

The common thread across all these tools is the input model:

A user enters an equipment identifier (typically make, model, year, and hours) and receives a value range. The output is algorithmic. It reflects what similar units have listed or sold for in aggregate, without accounting for the specific asset’s actual condition, installed attachments, maintenance history, geographic market, or configuration differences.

A 2018 Caterpillar 330 with a standard bucket in Arizona and a 2018 Caterpillar 330 with a hydraulic thumb, coupler, and grade control package in New England will return the same blue book range despite potentially differing in fair market value by 15–25%.

This distinction matters because the data source defines the ceiling of accuracy. A tool that cannot see attachments, deferred maintenance, or regional demand cannot produce a value that reflects those factors, no matter how large its dataset.

What a Certified Appraisal Is and Who Can Produce One

A certified appraisal is a written opinion of value produced by a credentialed appraiser, developed under the Uniform Standards of Professional Appraisal Practice (USPAP), and documented in a report that meets specific content and disclosure requirements. Three elements distinguish it from any pricing reference or informal estimate: the appraiser’s credentials, a defined standard of value, and a compliant report.

Credentialed appraiser. The opinion must be signed by an individual holding a recognized professional designation in machinery and equipment valuation, such as ASA (American Society of Appraisers) or CMEA (Certified Machinery & Equipment Appraiser). These designations require coursework, demonstrated experience, peer-reviewed work product, and adherence to a code of ethics. A dealer quote, a broker’s opinion of value, or a number pulled from an online tool does not meet this threshold, regardless of the individual’s industry experience.

Defined standard of value. Every certified appraisal states the specific value type being concluded: fair market value, orderly liquidation value, forced liquidation value, or another recognized standard. The value type is selected based on the appraisal’s intended use. A blue book range carries no defined standard of value and no stated premise, which is why it cannot substitute for an appraisal in contexts that require one.

Compliant report. USPAP requires the report to disclose the scope of work, the approaches to value considered, the data and reasoning supporting the conclusion, and any assumptions or limiting conditions. The report format can range from a restricted appraisal report to a full narrative, depending on the assignment’s complexity and the client’s needs.

Scope also varies.

A complete onsite appraisal involves physical inspection of every asset. A desktop appraisal relies on client-supplied data, photographs, and asset lists without a site visit. Both can be USPAP-compliant when the scope of work is appropriate and disclosed.

The critical difference from a blue book tool is not the inspection method but the professional judgment applied:

An appraiser evaluates condition, configuration, market conditions, and functional utility for each specific asset rather than returning a statistical composite for a generic unit.

Lenders, courts, the IRS, and insurance carriers accept certified appraisals precisely because the report structure creates an auditable chain of reasoning from data to conclusion. That chain is what makes the value supportable under scrutiny.

Where Blue Book Pricing Falls Short

Automated pricing tools fail in four predictable ways, each tied to information the tool’s input model cannot capture. These are not edge cases. They affect the majority of equipment transactions where the asset’s actual configuration or market context deviates from the statistical average.

- Condition variability beyond tier labels. Blue book tools offer broad condition categories (good, fair, poor) or no condition input at all. A “good” 2016 Komatsu PC210LC with 6,200 hours and a documented preventive maintenance history is not the same asset as a “good” unit with the same hours that has a cracked boom weld, leaking hydraulic cylinders, and no service records. Both return the same blue book range. An appraiser performing even a desktop appraisal with photographs and maintenance documentation distinguishes between these two machines. The pricing tool cannot.

- Configuration and attachment differences. A base-model excavator and one equipped with a hydraulic quick coupler, thumb, GPS grade control, and a second auxiliary hydraulic circuit may share the same make, model, and year, but their market values can diverge by 15–30%. Blue book inputs do not capture installed attachments or factory-option packages. The tool treats a stripped unit and a fully configured unit as identical.

- Regional demand gaps. Equipment markets are geographic. A motor grader holds stronger resale value in West Texas, where county road maintenance drives consistent demand, than in the Pacific Northwest, where the same unit may sit on a dealer lot for months. Blue book tools aggregate transaction data nationally (or across whatever dataset the platform maintains), smoothing out the regional pricing variations that directly affect what a specific buyer in a specific market will pay.

- Standard of value mismatch. Blue book ranges carry no defined standard of value. They are not fair market value, not orderly liquidation value, and not forced liquidation value. They are statistical composites without a stated premise. A lender sizing collateral needs OLV. An IRS filing for a charitable donation requires FMV. A blue book number satisfies neither requirement because it does not conclude a recognized value type under a defined set of assumptions.

Each of these gaps compounds the others.

A fully configured excavator in a strong regional market, appraised at fair market value, can exceed the blue book midpoint by 25–40%. That spread determines whether a loan is properly collateralized, a tax deduction survives audit, or an insurance claim recovers the actual loss.

Auction Results, a Third Category

Auction sale records are neither blue book estimates nor certified appraisals. They are transaction data: actual prices paid by actual buyers under specific sale conditions. The major public sources are Ritchie Bros. Auctioneers (rbauction.com), IronPlanet (ironplanet.com, now part of Ritchie Bros.), and Purple Wave. Each platform publishes historical results searchable by make, model, year, and hours, creating a large pool of comparable sale evidence.

Appraisers treat auction results as raw inputs within the sales comparison approach, not as finished conclusions. A closed auction price tells you what one unit sold for on one day under one set of conditions.

It does not tell you why.

The appraiser’s professional work is the adjustment process: analyzing differences in condition, configuration, hours, attachments, and time of sale between the comparable and the subject asset, then quantifying those differences to arrive at a supported value opinion.

IronPlanet’s IronClad Assurance program adds particular value here because condition is documented by a third-party inspector at the time of sale, producing higher-quality comparable data than self-reported listings.

Most consignment auction results reflect conditions closer to orderly liquidation value than to fair market value, though individual lots within the same auction can vary depending on reserve status and seller motivation.

An appraiser accounts for these sale-condition variables when selecting and adjusting comparables. A blue book tool ingesting the same auction data treats every result as equivalent, regardless of the circumstances behind the hammer price.

That difference in analytical treatment is why two parties can reference the same auction dataset and reach conclusions that diverge by 20% or more.

When Each Tool Is Appropriate

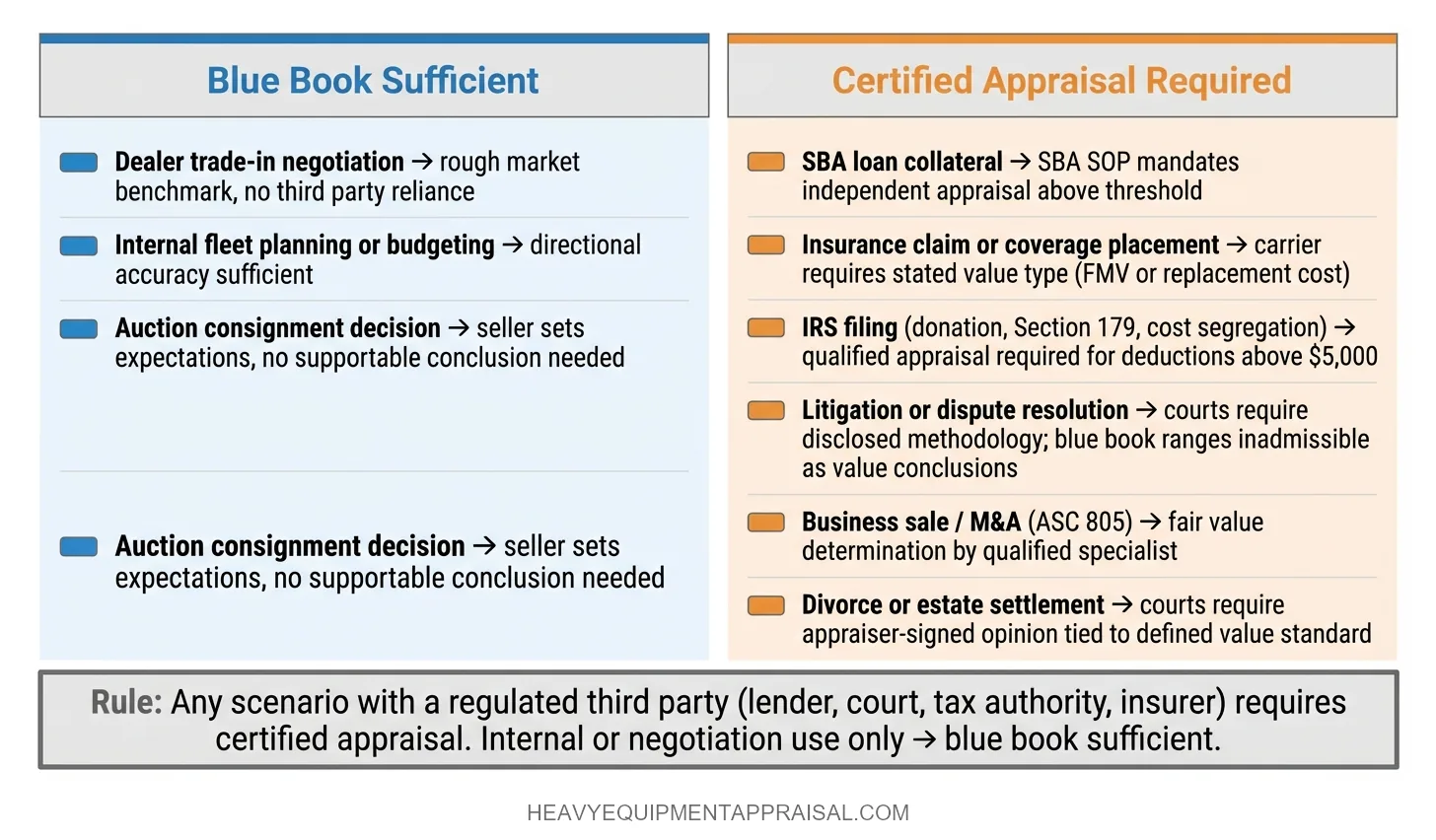

The right tool depends on the intended use of the value, not on the asset being valued. A blue book reference is appropriate for internal screening and informal negotiations where no third party requires a supportable value opinion. A certified appraisal is required whenever the value conclusion must withstand scrutiny from a lender, court, government agency, or counterparty in a transaction.

The decision matrix below maps common scenarios to the appropriate tool. “Blue book sufficient” means the scenario tolerates an algorithmic estimate without a defined standard of value. “Certified appraisal required” means a credentialed, USPAP-compliant opinion is either legally mandated or practically necessary to protect the party relying on the number.

| Scenario | Blue Book Sufficient | Certified Appraisal Required | Why |

|---|---|---|---|

| SBA loan collateral | No | Yes | SBA SOP requires independent appraisal for equipment collateral above threshold values |

| Insurance claim or coverage placement | No | Yes | Carriers require a stated value type (typically FMV or replacement cost) with supporting documentation |

| IRS filing (donation, Section 179, cost segregation) | No | Yes | IRS requires qualified appraisal by qualified appraiser for deductions above $5,000 |

| Litigation or dispute resolution | No | Yes | Courts require expert opinion with disclosed methodology. Blue book ranges are inadmissible as value conclusions |

| Business sale or M&A (purchase price allocation) | No | Yes | ASC 805 requires fair value determination by a qualified specialist |

| Divorce or estate settlement | No | Yes | Courts and mediators require appraiser-signed opinions tied to a defined value standard |

| Dealer trade-in negotiation | Yes | No | Both parties accept rough market benchmarks as a starting point for negotiation |

| Internal fleet planning or budgeting | Yes | No | No third party relies on the number. Directional accuracy is sufficient |

| Auction consignment decision | Yes | No | Seller needs a ballpark to set expectations, not a supportable conclusion |

The pattern is consistent: any scenario involving a regulated third party (lender, court, tax authority, insurer) requires a certified appraisal. Any scenario where the number stays internal or serves only as a negotiation reference point can rely on a blue book tool.

Mismatching the tool to the scenario does not just reduce accuracy. It renders the value unusable for its intended purpose, forcing the process to restart with the correct instrument and delaying the underlying transaction.

What a Certified Appraisal Covers That a Blue Book Cannot

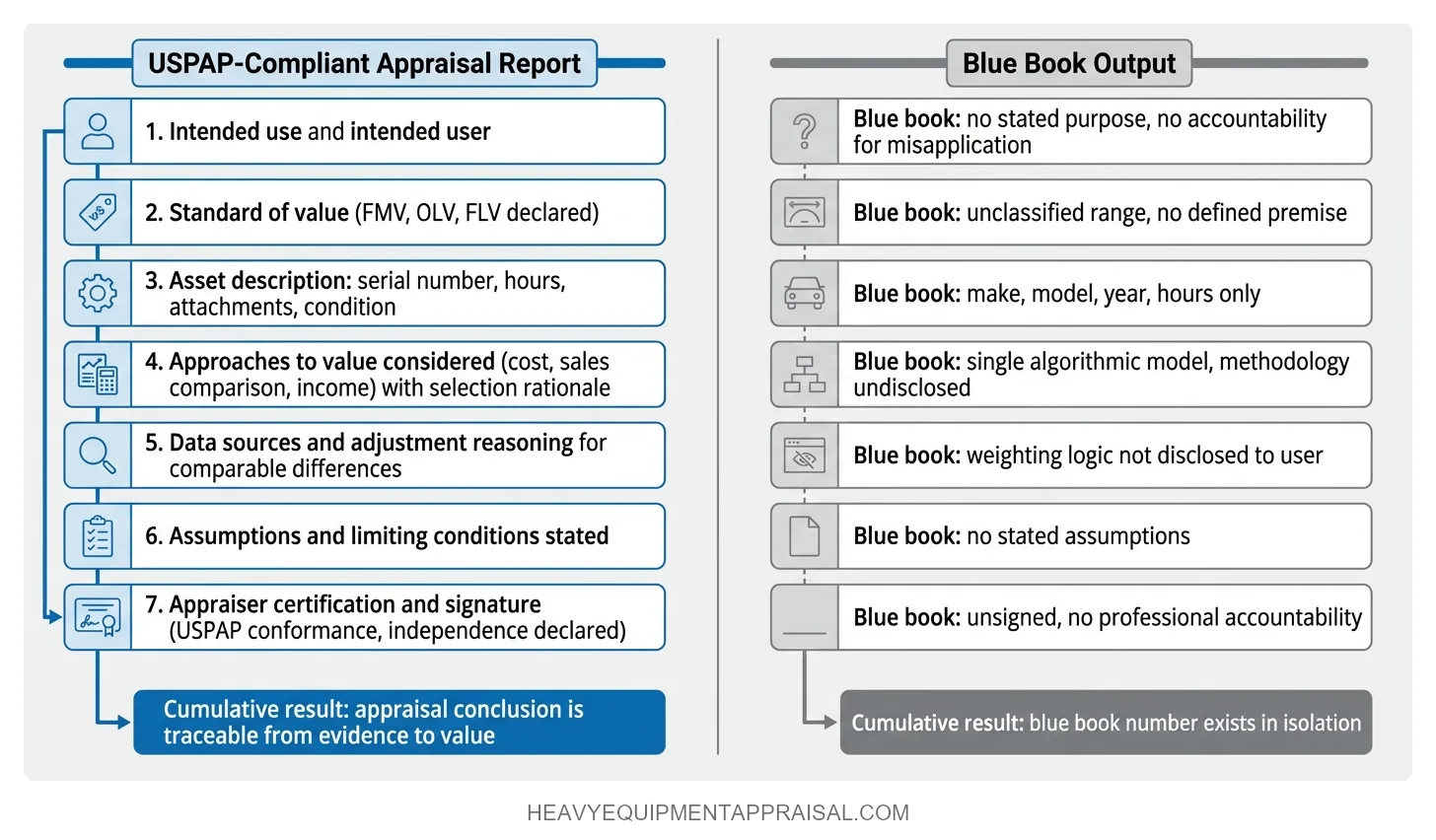

A USPAP-compliant appraisal report contains seven substantive components that have no equivalent in a blue book output. Each component exists to make the value conclusion traceable, auditable, and fit for reliance by a third party.

Intended use and intended user: The report states the specific purpose the appraisal serves (loan collateral, tax filing, litigation support) and identifies who may rely on the conclusion. A blue book output carries no stated intended use and no restriction on how the number gets applied, which means it also carries no accountability for misapplication.

Standard of value: The appraiser declares whether the conclusion represents fair market value, orderly liquidation value, forced liquidation value, or another recognized type. Blue book ranges are unclassified. They correspond to no defined value standard, so no third party can determine what assumptions underlie the number.

Asset description and condition assessment: The report documents the specific asset's make, model, serial number, hours, configuration, installed attachments, and observed or reported condition. A blue book tool captures make, model, year, and hours. Everything else is invisible to the algorithm.

Approaches to value considered: The appraiser discloses which valuation methodologies were applied (cost, sales comparison, income) and explains why each was selected or excluded. A blue book applies a single algorithmic model with no disclosed methodology and no selection rationale.

Data sources and adjustment reasoning: The report identifies the comparable sales, cost data, or income projections used, along with the adjustments made for differences between comparables and the subject asset. Blue book tools do not disclose their weighting logic or adjustment methodology to the end user.

Assumptions and limiting conditions: The report states every assumption the appraiser relied on and any conditions that limit the conclusion's applicability. A blue book output contains no stated assumptions, leaving the user unable to evaluate what the number does and does not account for.

Appraiser certification and signature: The appraiser certifies that the analysis is independent, that no undisclosed interest exists in the asset, and that the work conforms to USPAP. The certification ties a credentialed individual's professional standing to the conclusion. A blue book number is unsigned and carries no professional accountability.

The cumulative effect of these seven components is a report that a lender, judge, or tax examiner can walk backward from conclusion to evidence. Without that traceability, the number exists in isolation, unsupported by reasoning and unattached to professional accountability. That is the structural difference that determines whether a value opinion can serve as evidence or only as a reference point.

The Cost and Time Difference, and When It Matters

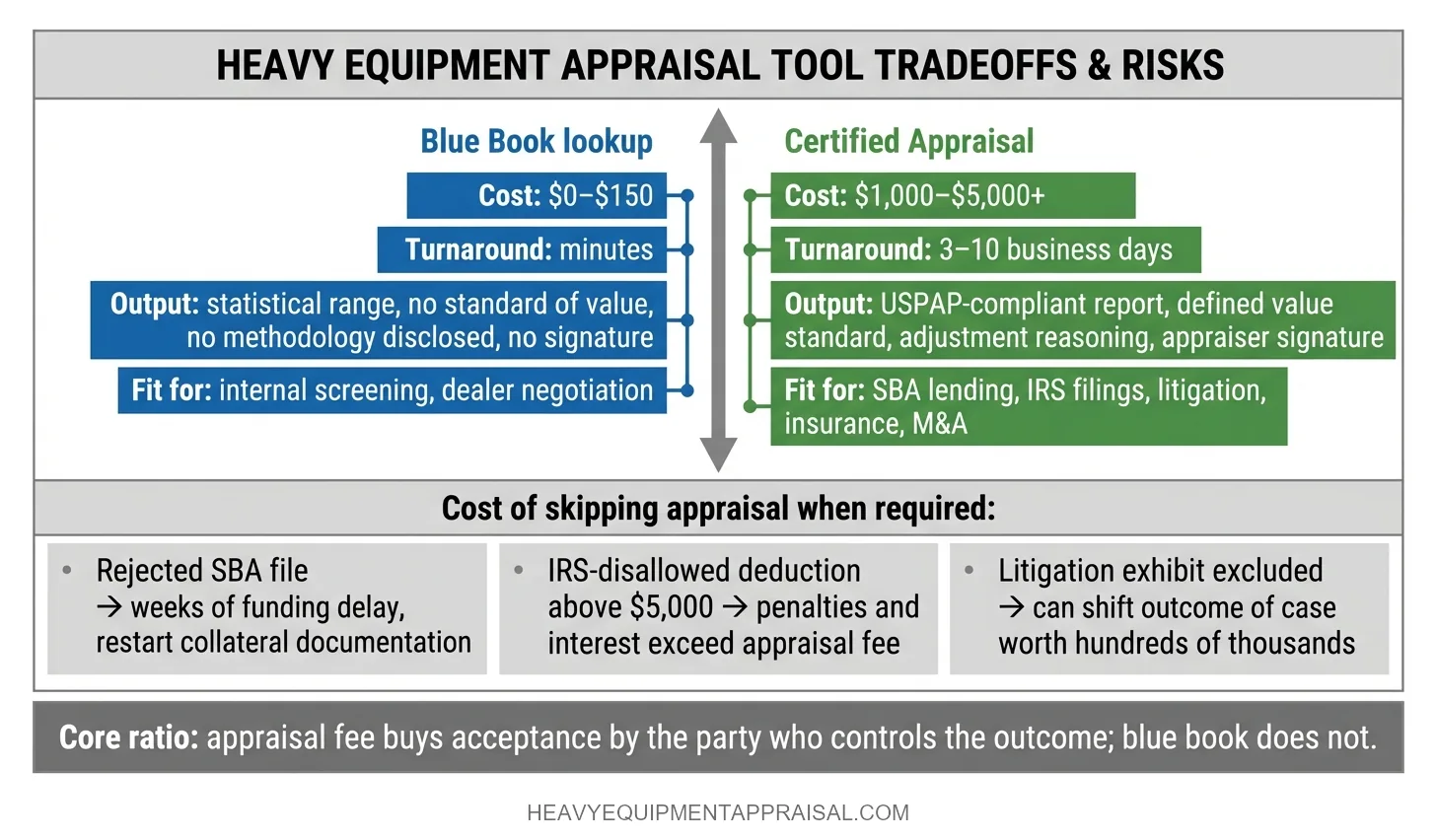

A blue book lookup costs $0–$150 and takes minutes. A certified equipment appraisal typically costs $1,000–$5,000+ depending on the number of assets, complexity, and whether an onsite inspection is required, with turnaround ranging from 3–10 business days. That cost gap is real, and for internal screening or dealer negotiations, the cheaper tool is the right one. The question is whether the scenario tolerates the limitations that come with the lower price.

The cost of a certified appraisal is not the cost of a number, it is the cost of a supportable conclusion:

The appraiser's credential, the adjustment analysis, the USPAP-compliant report structure, and the professional accountability attached to the signature.

A blue book lookup buys a statistical range with no stated standard of value, no disclosed methodology, and no individual standing behind it. The price difference reflects the difference in what each product can withstand.

Context determines whether the appraisal fee is an expense or an insurance policy.

A rejected SBA loan file delays funding by weeks and may require the borrower to restart the collateral documentation process.

An IRS-disallowed deduction above $5,000 triggers penalties and interest that dwarf the appraisal cost.

A litigation exhibit excluded at trial because it lacks expert methodology can shift the outcome of a case worth hundreds of thousands of dollars.

In each scenario, the "savings" from skipping the appraisal converts into a cost that is orders of magnitude larger.

The appraisal fee buys something a blue book price cannot: acceptance by the party who controls the outcome of the transaction. Without that acceptance, the value figure has no practical effect regardless of its accuracy.

FAQ

Does a certified equipment appraisal replace a blue book value for SBA loans?

SBA lending does not treat blue book and appraisal as automatic substitutes. A lender can rely on a guide value for standard equipment with an active resale market, but SBA loans often require an independent equipment appraisal when the asset is hard to value, the guide is outdated or unsupported, or the collateral value meaningfully affects the credit decision.

What is the difference between fair market value and a blue book price range?

The main difference between fair market value and an equipment blue book price range is that fair market value reflects the likely sale price of a specific asset, while a blue book range provides a general market guide.

Can I use EquipmentWatch or Sandhills Global data for an IRS equipment donation deduction?

Use EquipmentWatch or Sandhills Global data to support an IRS equipment donation value, but use a qualified appraisal when the claimed deduction exceeds $5,000.

Why do lenders reject blue book printouts as collateral documentation?

Lenders reject blue book printouts because they provide general pricing data, not verified asset-specific collateral support.

What credentials must an equipment appraiser hold to produce a USPAP-compliant report?

A USPAP-compliant equipment appraisal requires a competent appraiser who follows USPAP, not a single mandatory credential.

How do auction sale results from Ritchie Bros. or IronPlanet differ from a blue book estimate or a certified appraisal?

Auction sale results from Ritchie Bros. or IronPlanet show what similar equipment sold for at a specific auction on a specific date. A blue book estimate provides a general market price range based on compiled data. A certified appraisal determines the value of a specific asset by analyzing condition, configuration, use, market, and intended purpose such as lending, tax, or litigation.

Does a desktop appraisal qualify as a certified appraisal for bank lending purposes?

A desktop appraisal can qualify for bank lending purposes only if the lender accepts that scope of work and the report meets the bank’s appraisal, collateral, and underwriting requirements. Desktop describes the inspection method, not the certification level. Many banks accept desktop appraisals for lower-risk or smaller loans, but higher-risk credits often require a field inspection and a more detailed appraisal report.

What happens if I submit a blue book value instead of a qualified appraisal on an IRS filing?

If the IRS requires a qualified appraisal and you submit only a blue book value, the deduction can be reduced or fully disallowed. Blue book data can support market research, but it does not satisfy the qualified appraisal requirement by itself. For noncash charitable contributions, that risk usually applies when the claimed value exceeds $5,000 and the filing requires a qualified appraisal and completed appraisal documentation.

How does regional market demand affect equipment value beyond what blue book tools capture?

Regional market demand changes equipment value by pushing actual local prices above or below blue book ranges that do not fully capture local conditions.