USPAP Equipment Appraisal Standards: What They Require and Why They Matter

The Uniform Standards of Professional Appraisal Practice (USPAP) is the authoritative standard governing equipment appraisals accepted by lenders, the IRS, the SBA, and courts in the United States.

Published by The Appraisal Foundation, which Congress authorized in the Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (FIRREA), USPAP establishes the ethical and methodological requirements that separate a credible appraisal from an unsupported opinion of value.

Equipment appraisals fall under the personal property standards within USPAP, and compliance is not a style preference. It is a threshold requirement for most institutional and legal use cases.

What USPAP Is and Who Sets It

USPAP is published by The Appraisal Foundation, a nonprofit authorized by Congress in 1989 as the source of appraisal standards and appraiser qualifications in the United States. The Appraisal Standards Board (ASB), the body within The Appraisal Foundation responsible for promulgating USPAP, updates the standards on a 2-year edition cycle. The current edition covers 2026.

USPAP is not law in itself.

Federal agencies, interagency banking guidelines, and many state statutes require USPAP compliance for appraisals used in regulated transactions. The FDIC, Federal Reserve, OCC, and other banking regulators jointly treat USPAP as the minimum standard for appraisals submitted to federally supervised lending institutions. This extends beyond SBA lending to any commercial transaction where a federally regulated lender requires a collateral appraisal.

Equipment appraisers are not state-licensed the way real estate appraisers are. No state licensing board governs who can call themselves a machinery and equipment appraiser.

This absence of regulatory licensing makes voluntary USPAP adherence, and the credentials that enforce it, the primary credibility signal for personal property appraisers. Without that regulatory licensing framework, USPAP compliance is the mechanism that distinguishes a credible equipment appraisal from an unqualified opinion of value.

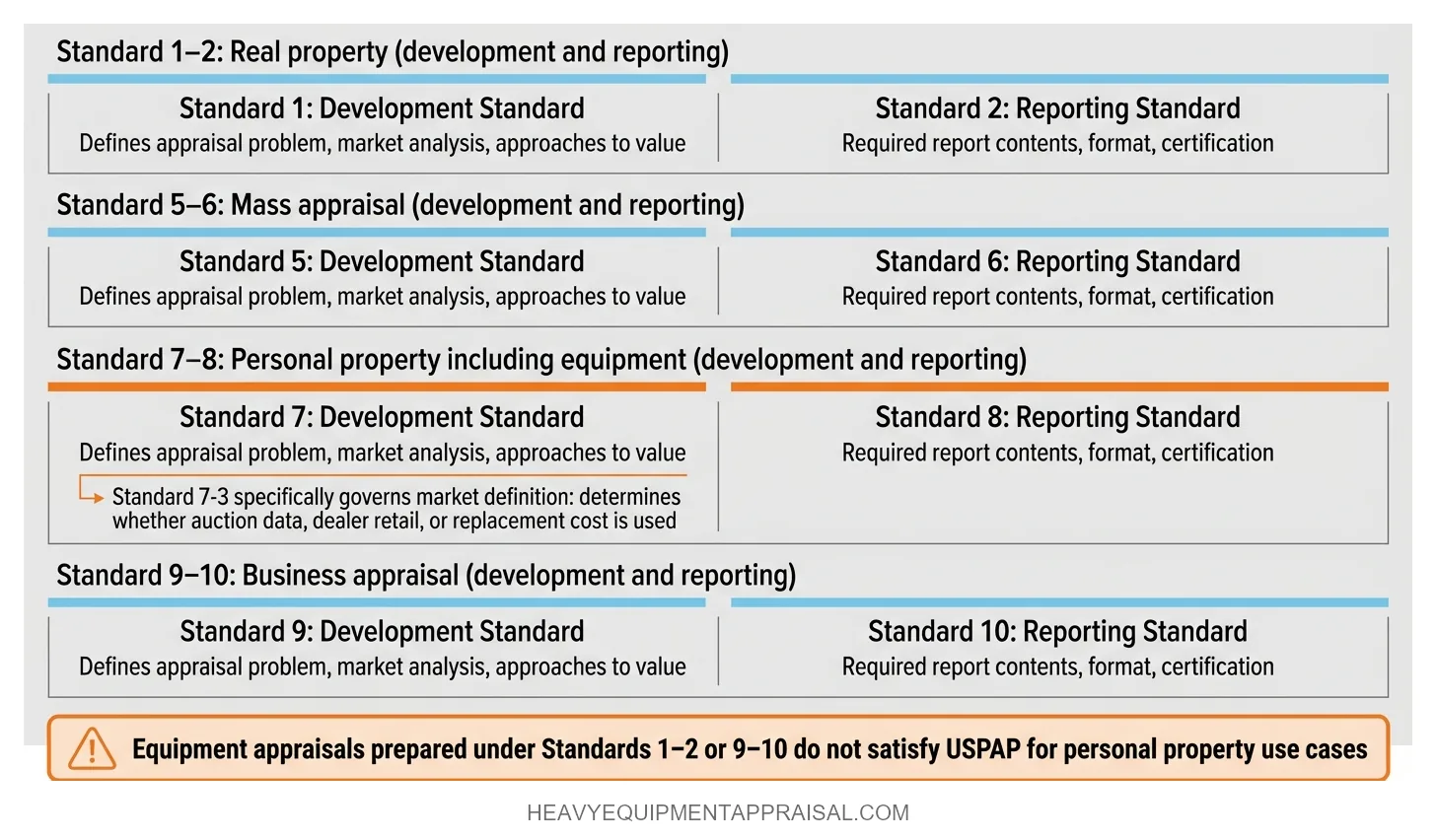

Which USPAP Standards Apply to Equipment Appraisals

Equipment appraisals fall under Standard 7 (development) and Standard 8 (reporting), the USPAP standards governing personal property appraisals. USPAP contains 10 standards total, organized by asset class.

| Standard | Scope | Asset Class |

|---|---|---|

| Standards 1–2 | Development and Reporting | Real property |

| Standards 5–6 | Development and Reporting | Mass appraisal |

| Standards 7–8 | Development and Reporting | Personal property (including equipment) |

| Standards 9–10 | Development and Reporting | Business appraisal |

Standard 7 governs how the appraiser develops the appraisal. It requires identifying the appraisal problem, collecting data, selecting and applying approaches to value, and forming a credible opinion.

A specific Standards Rule within Standard 7 (Standard 7-3) requires the appraiser to define and analyze the appropriate market for the subject property. This is the provision that determines whether the appraiser uses auction data, dealer retail data, or replacement cost data. The market definition drives which comparable sales are relevant and which level-of-trade assumptions apply.

Standard 8 governs how the appraiser communicates the results. It specifies what the report must contain, what cannot be omitted, and what level of detail is required for the report to function as a credible document.

Standards 1–2 (real property) and Standards 9–10 (business valuation) do not apply to individual equipment appraisals. An equipment appraisal report prepared under the wrong standards pair fails to satisfy USPAP for its intended purpose.

4 cross-cutting Rules apply across all USPAP standards:

- The Ethics Rule

- The Competency Rule

- The Scope of Work Rule

- The Record Keeping Rule

A Jurisdictional Exception Rule also applies when state or local law conflicts with USPAP provisions. These rules bind every appraiser in every assignment regardless of asset class.

What USPAP Compliance Requires in Practice

USPAP compliance is not a checklist. It is a framework of rules that governs how the appraiser defines the problem, investigates it, and reports the conclusion. These 3 rules carry the most practical weight for equipment appraisals:

1. Scope of Work

The Scope of Work Rule requires the appraiser to identify and perform the research and analysis necessary to produce a credible assignment result. Credible is a defined term in USPAP: worthy of belief, meaning supported by data and reasoning adequate for the intended use. An opinion that is credible for internal asset tracking may not be credible for SBA loan collateral review.

Scope is determined by the intended use and intended users. A desktop appraisal for internal planning has different scope requirements than an on-site appraisal for a federally regulated lending transaction. The appraiser determines:

- The degree of inspection

- The extent of market research

- The depth of analysis appropriate for the assignment

These decisions must be disclosed in the report. A scope decision that produces a result unsuitable for its stated intended use is not USPAP-compliant, even if the report is otherwise well-constructed. The scope disclosure is what allows a reviewer to determine whether the appraiser’s work was adequate for the purpose it claims to serve.

2. The Ethics Rule

The Ethics Rule prohibits advocacy. The appraiser’s opinion must be independent and impartial, not shaped by the outcome the client wants. Contingency fees based on the appraised value are explicitly prohibited. An appraiser whose compensation increases if the equipment appraises higher (or lower) cannot produce a USPAP-compliant report.

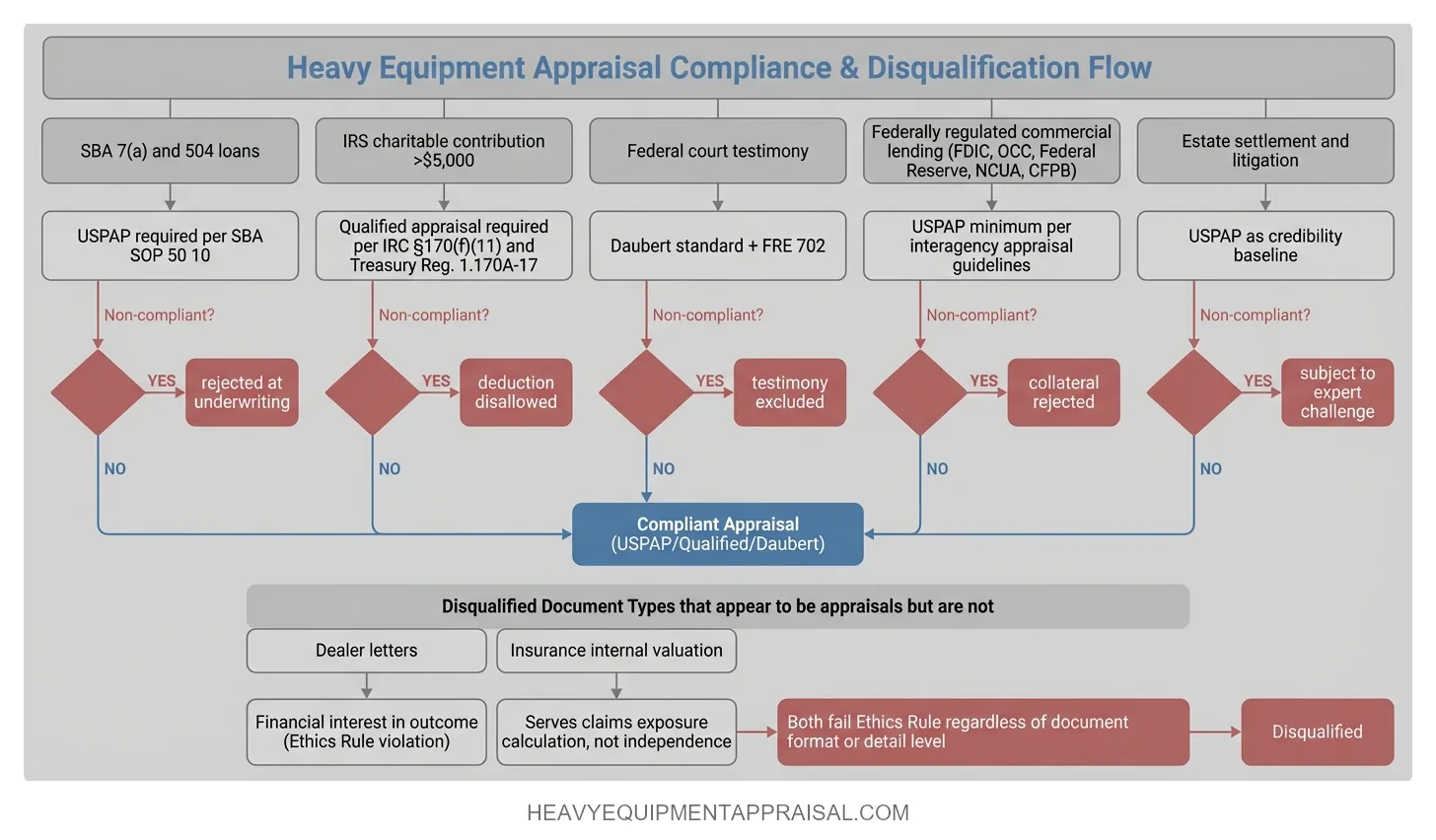

This prohibition is what disqualifies dealer estimates and insurance company internal valuations from functioning as appraisals in regulated contexts. A dealer has a financial interest in the transaction outcome. An insurance company’s internal valuation serves the company’s claims exposure calculation. Neither party meets the independence requirement of the Ethics Rule, and neither output satisfies USPAP regardless of how detailed the document appears.

3. The Competency Rule

The Competency Rule requires the appraiser to have the knowledge and experience to complete the specific assignment competently. If the appraiser lacks competency in the relevant asset class, they must disclose the deficiency to the client before accepting the assignment and take steps to remedy it before completing the work.

A real estate appraiser cannot produce a USPAP-compliant equipment appraisal without personal property competency. The credential category and the competency requirement are linked.

This is why appraiser credentials in the machinery and equipment category, such as the ASA designation from the American Society of Appraisers or the AMEA designation from the Equipment Appraisers Association of North America, matter. They are documented evidence of subject-matter competency in the asset class the appraisal covers.

An appraisal signed by an appraiser lacking demonstrable M&E competency is vulnerable to challenge on Competency Rule grounds alone.

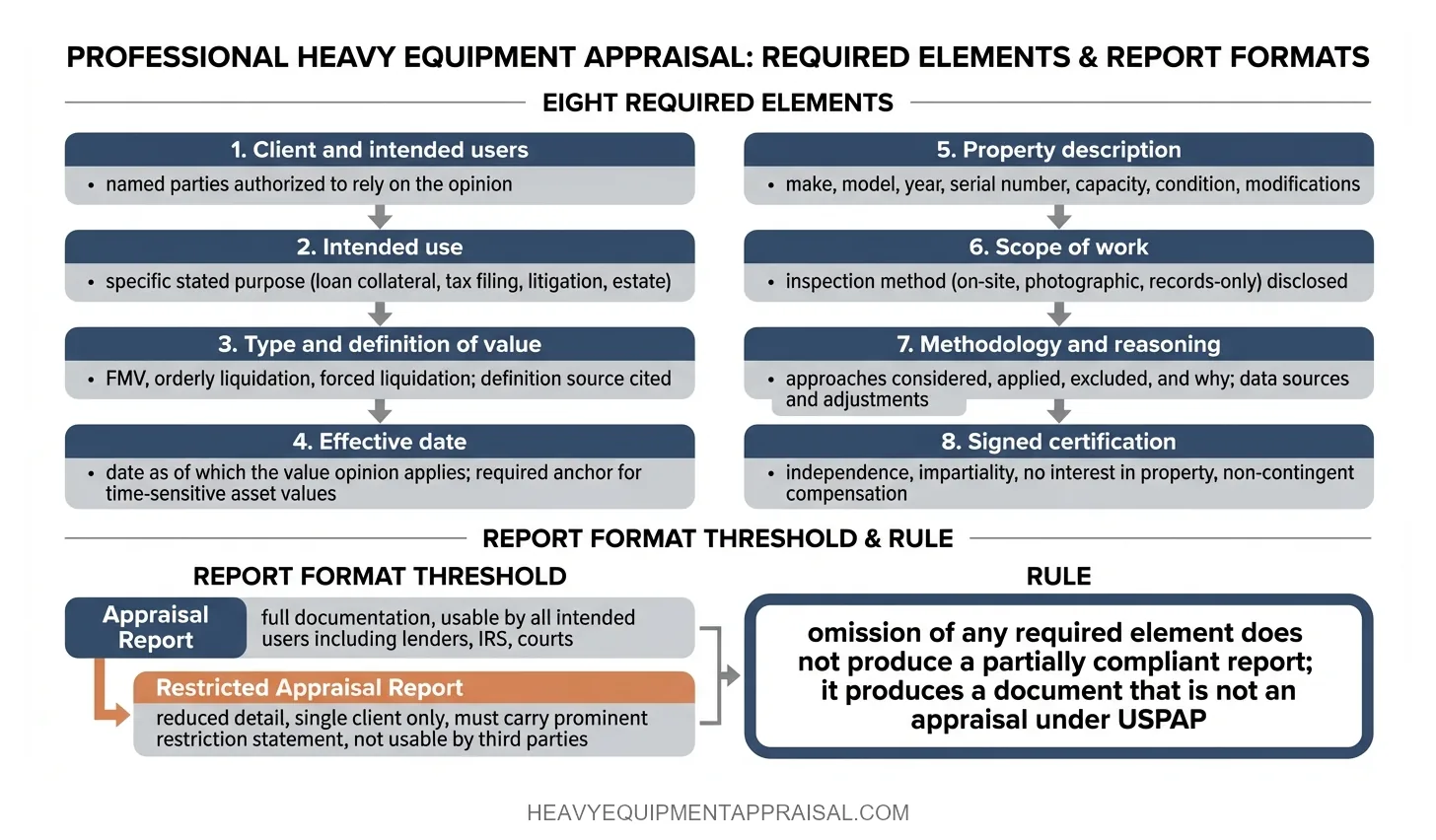

What a USPAP-Compliant Equipment Appraisal Report Contains

A USPAP-compliant equipment appraisal report under Standard 8 must contain specific elements. Omissions do not produce a “mostly compliant” report. They produce a document that is not an appraisal under USPAP. The required elements are:

- Identification of the client and intended users

- The report must name the client and identify (by name or type) all parties authorized to rely on the appraisal opinion.

- Identification of the intended use

- The specific use of the appraisal (loan collateral, tax filing, litigation, estate settlement) must be stated. Intended use drives scope, scope drives methodology, and methodology drives the value conclusion.

- Type and definition of value

- The report must specify the type of value (fair market value, orderly liquidation value, forced liquidation value, or another defined type) and cite the source of the definition used.

- Effective date

- The date as of which the value opinion applies. Equipment values are time-sensitive. A value opinion without a stated effective date has no anchor.

- Description of the subject property

- Sufficient detail for identification: make, model, year, serial number, capacity, condition, and any modifications or attachments.

- Scope of work performed

- What the appraiser did and did not do. Whether the equipment was inspected on-site, reviewed via photographs, or valued from records alone.

- Methodology and reasoning

- Which approaches to value were considered, which were applied, and why any approach was excluded. The data sources, adjustments, and analytical reasoning supporting the conclusion.

- Signed certification

- A formal attestation that the appraiser performed an independent, impartial analysis, that the statements of fact are true and correct, that the appraiser has no present or prospective interest in the property, and that compensation is not contingent on the value conclusion.

Two report formats exist under Standard 8:

The Appraisal Report contains full documentation of the elements listed above. The Restricted Appraisal Report contains less detail and is limited to a single client who has prior knowledge of the engagement context.

A Restricted Appraisal Report must contain a prominent statement restricting its use to that single party. Any third party (lender, IRS, court, opposing counsel) cannot rely on a Restricted Appraisal Report. Lenders, courts, and the IRS require the full Appraisal Report format. Ordering a Restricted Appraisal Report when third-party reliance is anticipated means the report cannot be used for the purpose that prompted it.

When a Non-USPAP Appraisal Is Not Acceptable

A non-USPAP equipment appraisal is not acceptable for SBA loans, IRS charitable contribution deductions over $5,000, litigation, estate settlement, and most commercial lending transactions.

SBA Standard Operating Procedure 50 10 requires USPAP compliance for appraisals of personal property used as collateral in SBA 7(a) and 504 loans. A non-compliant valuation submitted as collateral support will be rejected by the lender’s underwriting review.

IRS regulations under IRC Section 170(f)(11) require a “qualified appraisal” performed by a “qualified appraiser” for non-cash charitable contributions exceeding $5,000. The IRS definition of a qualified appraisal, detailed in Treasury Regulation 1.170A-17 and the instructions for Form 8283, incorporates the substance of USPAP requirements. An equipment appraisal for tax purposes that fails to meet these requirements exposes the donor to disallowance of the deduction.

Courts treat USPAP compliance as the credibility baseline for expert valuation testimony. Under the Daubert standard and Federal Rule of Evidence 702, judges evaluate whether an expert’s methodology is reliable, testable, and generally accepted.

A non-USPAP equipment valuation opinion offered as expert testimony is vulnerable to a Daubert challenge. The opposing party can argue that the methodology is not grounded in a generally accepted standard, and the court may exclude the testimony entirely. This applies in divorce proceedings, estate settlement, business litigation, and insurance disputes where equipment value is contested.

The interagency appraisal guidelines issued by the Federal Reserve, FDIC, OCC, NCUA, and CFPB apply across all federally supervised financial institutions. USPAP compliance is a minimum requirement under these guidelines, not just for SBA transactions but for any equipment appraisal used as collateral in a regulated lending transaction.

How to Verify That an Appraiser Is USPAP-Compliant

USPAP compliance cannot be verified through a certificate alone. It is demonstrated through appraiser credentials, training records, and the content of the appraisal report itself.

The ASA (Accredited Senior Appraiser) designation from the American Society of Appraisers and the AMEA designation from the Equipment Appraisers Association of North America both require USPAP education as a condition of credentialing in the machinery and equipment category. Appraisers holding these designations have completed USPAP coursework (approximately 15 hours) and demonstrate ongoing compliance through continuing education requirements.

When reviewing a completed appraisal, 2 sections signal USPAP compliance most directly:

- The signed certification

- The scope of work disclosure

The certification attests to independence, impartiality, and non-contingent compensation. The scope of work disclosure documents what the appraiser did, what they did not do, and why the scope was adequate for the intended use. A report missing either element is not USPAP-compliant regardless of how detailed the valuation analysis appears.

Asking whether the appraiser holds an active machinery and equipment credential from ASA or EAANA before the assignment begins is the most reliable way to confirm both USPAP compliance and subject-matter competency. Verifying compliance before the appraisal is ordered prevents the situation where a completed report fails to qualify for its intended use.