FMV vs. OLV vs. FLV in Equipment Appraisal: Definitions, Differences, and When Each Applies

Fair market value (FMV), orderly liquidation value (OLV), and forced liquidation value (FLV) are the 3 standard value premises used in equipment appraisal.

The main difference between FMV, OLV, and FLV in equipment appraisal is the assumed sale condition and time horizon. FMV estimates price in an open market between willing parties. OLV estimates price from a managed sale over 60-180 days. FLV estimates price from a rapid sale, often 1-30 days, under compulsion.

Selecting the wrong one produces a number that is technically correct under its own assumptions but useless for the intended purpose. Each premise models a different set of hypothetical transaction conditions:

- Who is selling

- Under what time pressure

- To what buyer pool

This article defines all 3 premises, compares them directly, and maps each to the situations where it is required.

What a Value Premise Is

A value premise defines the hypothetical conditions of the transaction, not the physical condition of the equipment. It establishes the assumptions about seller motivation, marketing timeline, buyer pool, and transaction structure under which the appraiser forms a value opinion.

A Caterpillar 336 excavator with 4,000 hours will produce 3 different values under 3 different premises applied to the same physical machine on the same date.

The equipment’s age, hours, maintenance history, and physical condition all affect the number within a given premise. The premise itself is a separate variable. A well-maintained excavator will appraise higher than a neglected one under any premise, but the same well-maintained machine will appraise lower under FLV than under FMV because the assumed transaction conditions are more constrained.

The value premise also governs which comparable sales data is relevant, what marketing time assumptions are appropriate, and what buyer pool the appraiser is modeling.

A sale between 2 willing parties after 6 months of open-market listing is FMV-relevant data. An auction result from a 30-day consignment is FLV-relevant data. Mixing data from different transaction contexts without adjusting for the premise produces unreliable conclusions.

One structural point that competitors consistently miss: value premises are independent of appraisal approaches. The cost approach, sales comparison approach, or income approach can each be used to reach an FMV, OLV, or FLV conclusion. The premise governs the hypothetical conditions of the transaction. The approach governs the methodology used to estimate value under those conditions.

Lenders, courts, and tax authorities specify the required premise in advance. An appraisal that delivers a defensible number under the wrong premise is non-compliant regardless of the quality of the underlying analysis.

Fair Market Value (FMV)

Fair market value is the price at which equipment would change hands between a willing buyer and a willing seller, neither under compulsion to transact, both with reasonable knowledge of relevant facts. This definition derives from IRS Revenue Ruling 59-60 and is the most widely cited value standard across tax, legal, and transactional contexts.

FMV rests on 4 core assumptions:

- No compulsion to buy or sell on either side of the transaction.

- Both parties are reasonably informed about the equipment, its market, and relevant conditions.

- Adequate marketing time exists to expose the equipment to the broadest possible buyer pool.

- The transaction is arm’s length, with no special relationships or terms distorting the price.

Because FMV assumes the most favorable transaction conditions of the 3 standard premises, it produces the highest value for the same piece of equipment on the same date. The buyer pool is unrestricted. The seller has no time pressure. The price reflects what the market will bear under optimal conditions.

FMV has 2 common sub-premises worth noting briefly. FMV in continued use assumes the equipment remains installed and operational at its current location as part of a going concern. FMV in exchange assumes the equipment is removed and sold separately.

In-continued-use typically produces a higher value because removal, transportation, and reinstallation costs are not embedded. The full treatment of these sub-premises belongs in the dedicated FMV page, but the distinction matters when reading an appraisal report: a conclusion stated as “FMV in continued use” cannot be compared directly to one stated as “FMV in exchange.”

Common FMV use cases:

- IRS tax purposes: Charitable donation deductions on equipment exceeding $5,000, estate and gift tax calculations, cost segregation analysis.

- Divorce and estate settlement: Equitable distribution and probate proceedings default to FMV.

- M&A and business sale: Purchase price allocation under ASC 805, asset-based deal structuring, partner buyouts.

- Insurance: Replacement cost benchmarking often starts from FMV as a baseline reference.

One brief but important distinction: fair value as defined under ASC 820 for financial reporting purposes is not identical to FMV. ASC 820 fair value assumes an orderly transaction between market participants at the measurement date. It is closer to FMV than to OLV or FLV, but uses a different definitional framework. Financial reporting professionals working on purchase price allocation or impairment testing should not treat FMV and ASC 820 fair value as interchangeable terms.

FMV assumes conditions that often do not match a lender’s actual risk scenario. A lender sizing collateral against default risk cannot rely on FMV because default liquidation is not a willing-seller transaction. This is why lending appraisals default to liquidation premises.

Orderly Liquidation Value (OLV)

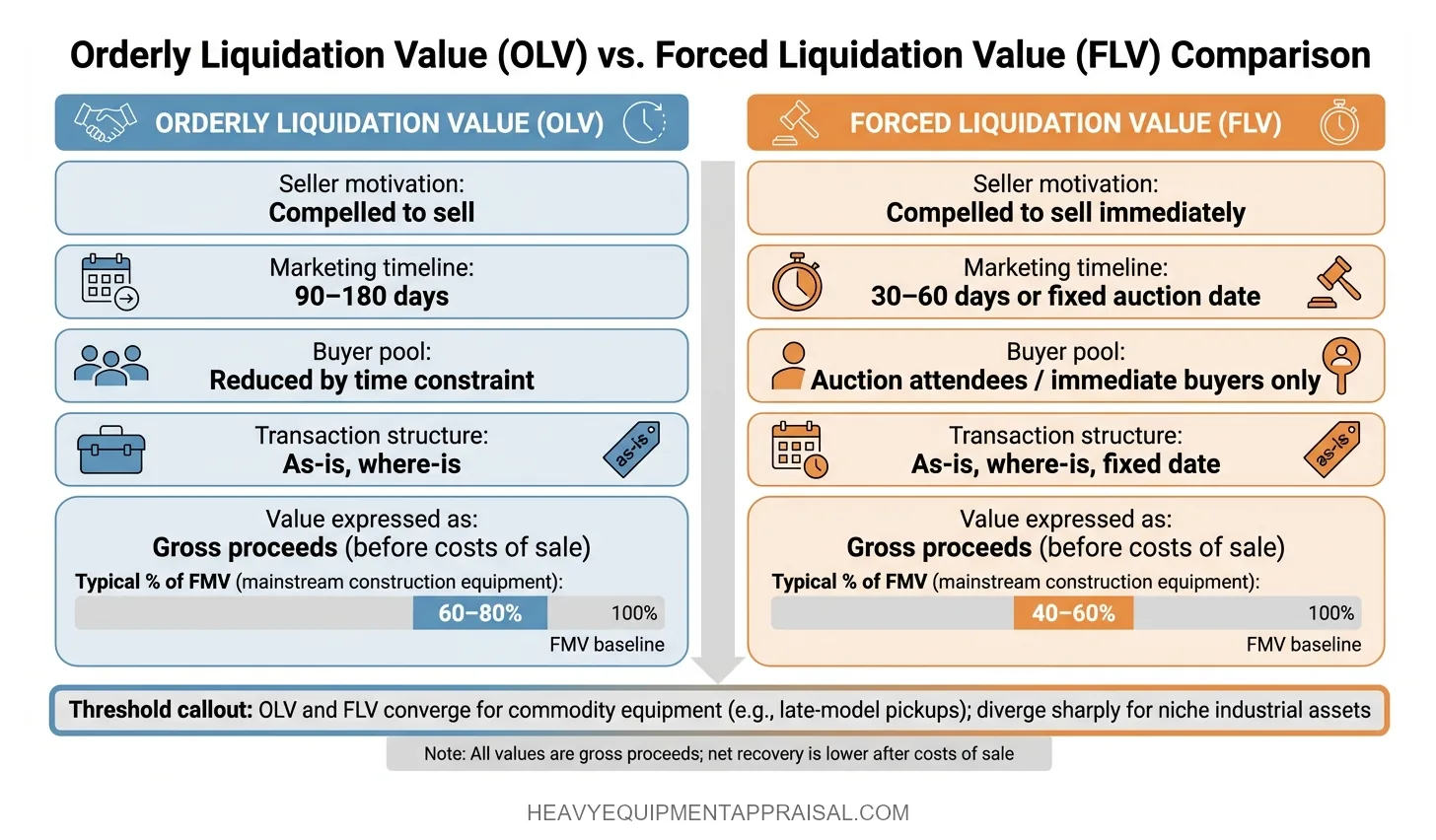

Orderly liquidation value is the estimated gross amount, expressed in terms of money, that could typically be realized from a sale given a reasonable time to find a purchaser, with the seller being compelled to sell on an as-is, where-is basis.

The defining characteristic of OLV is seller compulsion combined with adequate (but not unlimited) marketing time. The seller must sell. The question is how much the equipment will bring when the seller has a reasonable window to reach buyers, but no ability to hold indefinitely for an optimal price. In practice, that marketing window typically ranges from 90 to 180 days depending on equipment type and market depth.

A precision point that matters for lenders: OLV is expressed as gross proceeds, before costs of sale. Commissions, rigging, transport, and other disposition expenses reduce the net amount the seller actually receives. A lender who treats an OLV conclusion as equivalent to net recovery after liquidation expenses is overestimating recoverable collateral value.

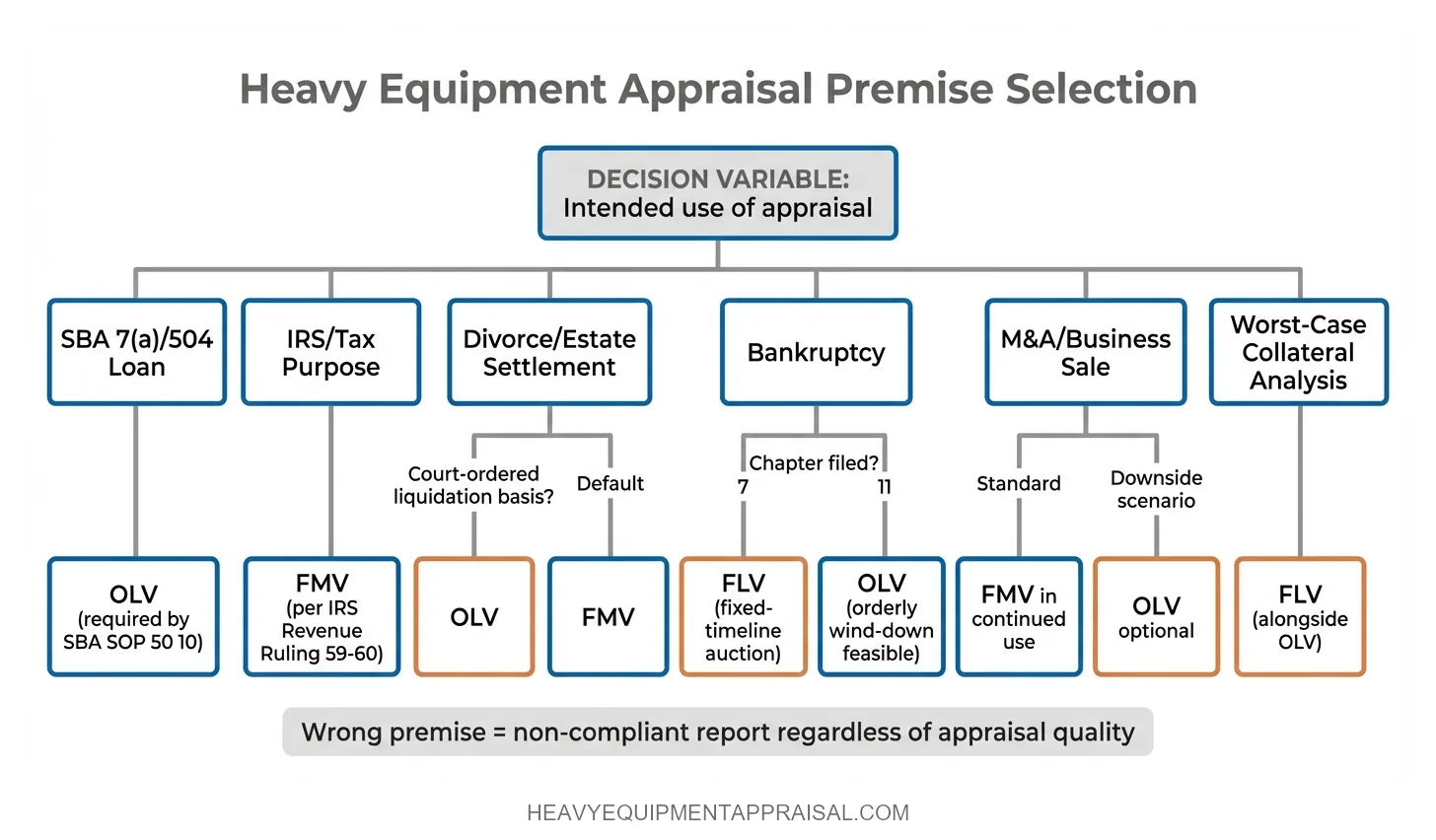

OLV is the primary collateral valuation premise for equipment-secured lending. The SBA’s Standard Operating Procedure (SOP) 50 10 requires OLV for equipment collateral under the 7(a) and 504 programs when a certified appraisal is triggered. Asset-based lending (ABL) practitioners set advance rates against OLV, not FMV, because OLV represents recoverable value in a non-adversarial wind-down.

Common OLV use cases:

- SBA 7(a) and 504 loan collateral when the appraisal threshold is met.

- ABL advance rate setting for revolving and term loan facilities secured by equipment.

- Equipment portfolio valuation for financial reporting and covenant compliance.

- Bankruptcy reorganization under Chapter 11 where a going-concern wind-down is possible.

OLV typically returns 60–80% of FMV for mainstream construction and transportation equipment with active secondary markets (excavators, motor graders, wheel loaders, over-the-road trucks). The gap widens for specialized or low-liquidity categories. Tunnel boring equipment, large process machinery, and highly customized production lines can see OLV fall to 40–50% of FMV because the buyer pool narrows dramatically under compressed marketing conditions.

An appraisal submitted to an SBA lender under FMV assumptions will be rejected or require revision regardless of the appraiser’s credentials. The program requirement is premise-specific, and OLV is not a conservative version of FMV. It is a different value conclusion under different hypothetical conditions.

Forced Liquidation Value (FLV)

Forced liquidation value is the estimated gross amount, expressed in terms of money, that could typically be realized from a properly advertised and conducted public auction, with the seller being compelled to sell with a sense of immediacy on an as-is, where-is basis.

FLV is the floor of the 3 standard premises. It assumes a fixed sale date (typically within 30 to 60 days), an as-is, where-is transaction, a buyer pool limited to those who can act within the auction timeline, and no ability to hold for a better offer. Every constraint that OLV imposes, FLV imposes more aggressively.

Two precision points are critical to understanding FLV correctly.

First, FLV assumes a properly advertised auction. The definition models a well-run sale with adequate buyer notification, not a distressed fire sale with no notice. FLV is the value the equipment would produce under auction-equivalent conditions run competently. It is not the worst-imaginable-case scenario.

Second, FLV is a value premise, not an auction prediction. A specific auction may produce more or less than an FLV opinion depending on auction quality, advertising reach, buyer attendance, weather, and market timing on that particular day. FLV estimates what properly conducted auction conditions would yield. Treating an FLV conclusion as a guarantee of what a specific auction will produce is a misapplication of the premise.

Like OLV, FLV is expressed as gross proceeds before costs of sale. Auction commissions (typically 10–15% of hammer price), buyer premiums, rigging, and transportation further reduce net recovery to the seller.

Common FLV use cases:

- Worst-case collateral analysis alongside OLV for lending decisions.

- Bankruptcy liquidation under Chapter 7 or forced asset sale.

- IRS collection enforcement and tax lien scenarios.

- Distressed business wind-down where assets must be converted to cash on a fixed timeline.

FLV typically returns 40–60% of FMV for standard construction equipment. For highly specialized machinery with thin buyer pools, the discount steepens further. OLV and FLV can converge for commodity-type equipment with deep auction markets (e.g., late-model pickup trucks) and diverge sharply for niche industrial assets where only a handful of potential buyers exist globally.

FLV is not inherently inferior as an appraisal. It is the correct premise when the hypothetical conditions it models match the actual situation. A Chapter 7 trustee liquidating a fabrication shop at auction needs FLV, not FMV. Misapplying FLV where OLV is required (or vice versa) is a premise error, not a quality error.

Side-by-Side Comparison

The 3 value premises differ across 6 key dimensions. The following table provides a direct comparison for the same piece of equipment appraised on the same date.

| Dimension | FMV | OLV | FLV |

|---|---|---|---|

| Seller motivation | No compulsion | Compelled to sell | Compelled to sell immediately |

| Marketing timeline | Adequate, open-ended | 90–180 days (typical) | 30–60 days or fixed auction date |

| Buyer pool | Broadest possible | Reduced by time constraint | Auction attendees or immediate buyers only |

| Transaction structure | Arm’s length, negotiated | As-is, where-is | As-is, where-is, fixed date |

| Value expressed as | Sale price | Gross proceeds (before costs of sale) | Gross proceeds (before costs of sale) |

| Typical % of FMV (mainstream construction equipment) | 100% (baseline) | 60–80% | 40–60% |

The percentage ranges in the final row apply to equipment with active secondary markets: excavators, dozers, wheel loaders, over-the-road trucks, and similar mainstream categories. Specialized, low-liquidity, or highly customized equipment categories show steeper discounts at both OLV and FLV. Process equipment, large cranes, and single-purpose production lines can fall well below the ranges above.

The gross-proceeds distinction in the “Value expressed as” row has practical consequences for lenders. A machine appraised at $200,000 OLV will not net $200,000 to the lender after liquidation. Commissions, rigging, transport, and legal costs reduce the actual recovery. Advance rate calculations that fail to account for this gap overstate recoverable collateral value.

Which Premise Applies to Which Situation

The intended use of the appraisal determines the required premise. The appraiser’s default, the client’s preference, or what produces the most favorable number are not controlling factors. Below are the standard premise assignments for the most common appraisal purposes.

SBA Loans

OLV is the required premise for equipment collateral under SBA 7(a) and 504 programs when the appraisal threshold is met. SBA SOP 50 10 specifies this requirement. FMV is not an acceptable substitute. An SBA loan appraisal delivered under FMV will be flagged during underwriting review and returned for correction.

IRS and Tax Purposes

FMV is the statutory standard for charitable contribution deductions, estate and gift tax valuations, and cost segregation analysis. IRS Revenue Ruling 59-60 establishes the definition. OLV and FLV are not appropriate premises for tax-purpose appraisals unless the IRS or a tax court explicitly requires a liquidation premise in a specific dispute.

Divorce and Estate Settlement

FMV is the default standard for equitable distribution in divorce and estate matters. Courts occasionally specify a different premise in contested proceedings. In cases where 1 party argues the equipment would need to be liquidated rather than continued in use, OLV can become relevant. The default remains FMV absent a specific court order.

Bankruptcy

FLV applies to Chapter 7 liquidation scenarios where assets are sold at auction or on a compressed timeline. OLV applies to Chapter 11 reorganization scenarios where a going-concern wind-down or orderly asset sale is feasible. The correct premise depends on the chapter filed and the trustee’s or debtor’s disposition plan.

M&A and Business Sale

FMV (typically FMV in continued use) is the standard for purchase price allocation and asset-based deal structuring in a business sale or M&A transaction. Buyers conducting due diligence sometimes request OLV as a downside scenario to understand recoverable value if the acquisition underperforms.

An appraisal delivered under the wrong premise is not a conservative or liberal version of the correct answer. It is a non-compliant appraisal that will require revision or replacement.

How USPAP Governs Value Premise Selection

Under the Uniform Standards of Professional Appraisal Practice (USPAP), the appraiser is responsible for identifying the value definition and premise that matches the intended use of the appraisal. Standards Rule 7-2 requires the appraiser to specify the type and definition of value in every personal property appraisal report. The scope of work rule further requires that methodology be appropriate for the stated intended use.

This obligation is not passive. The appraiser does not simply disclose which premise was used. The appraiser must independently determine that the selected premise is appropriate for the assignment's intended use. If a client requests FMV for an SBA collateral appraisal, a USPAP-compliant appraiser has 2 options: clarify the engagement to reflect the correct premise (OLV), or decline the assignment. Delivering a non-applicable value conclusion because the client asked for it is a scope-of-work violation.

An appraiser who delivers an FMV conclusion for an SBA 7(a) collateral assignment has produced a non-compliant report under both USPAP and SBA SOP requirements. The lender's underwriting team will typically catch this during review. The result is a delayed closing, a re-engagement, and additional cost. In the worst case, the original appraisal is discarded entirely.

Verifying that an appraiser has correctly identified the premise before work begins is as important as verifying their credentials. A credentialed appraiser using the wrong premise is still producing a non-compliant report.

Using the Correct Premise Protects Everyone in the Transaction

Premise selection determines whether the appraisal is usable, defensible, and compliant for its intended purpose. The consequences of getting it wrong are specific and tangible.

A lender who accepts a wrong-premise appraisal exposes the institution to collateral risk: the actual recoverable value in default may be 20–40% below the number in the report.

An attorney who relies on a wrong-premise appraisal in litigation faces evidentiary challenges when opposing counsel demonstrates the premise does not match the legal standard.

A business owner who uses a wrong-premise appraisal for a tax filing risks IRS scrutiny and potential revaluation.

The premise is the first decision in any equipment appraisal engagement. Before methodology, before comparable selection, before site inspection, the appraiser and client must agree on which hypothetical transaction conditions the value conclusion will model. Every subsequent step in the appraisal process flows from that decision. Getting it right at the outset costs nothing. Correcting it after the report is delivered costs time, money, and credibility.