Equipment Appraisal Cost: Pricing Guide by Type & Scope

Equipment appraisal cost ranges from $300 to $2,500 for most standard business equipment, while complex, high-value, or litigation appraisals often cost $3,000 to $10,000 or more. Price depends on equipment type, quantity, location, inspection needs, and whether the appraisal supports financing, insurance, tax, or legal use.

The two primary fee structures are per-asset pricing and hourly or day-rate billing. The purpose of the appraisal (SBA lending, litigation, insurance, estate settlement) determines the scope requirements, and scope is what ultimately drives cost.

What a Single-Asset Equipment Appraisal Costs

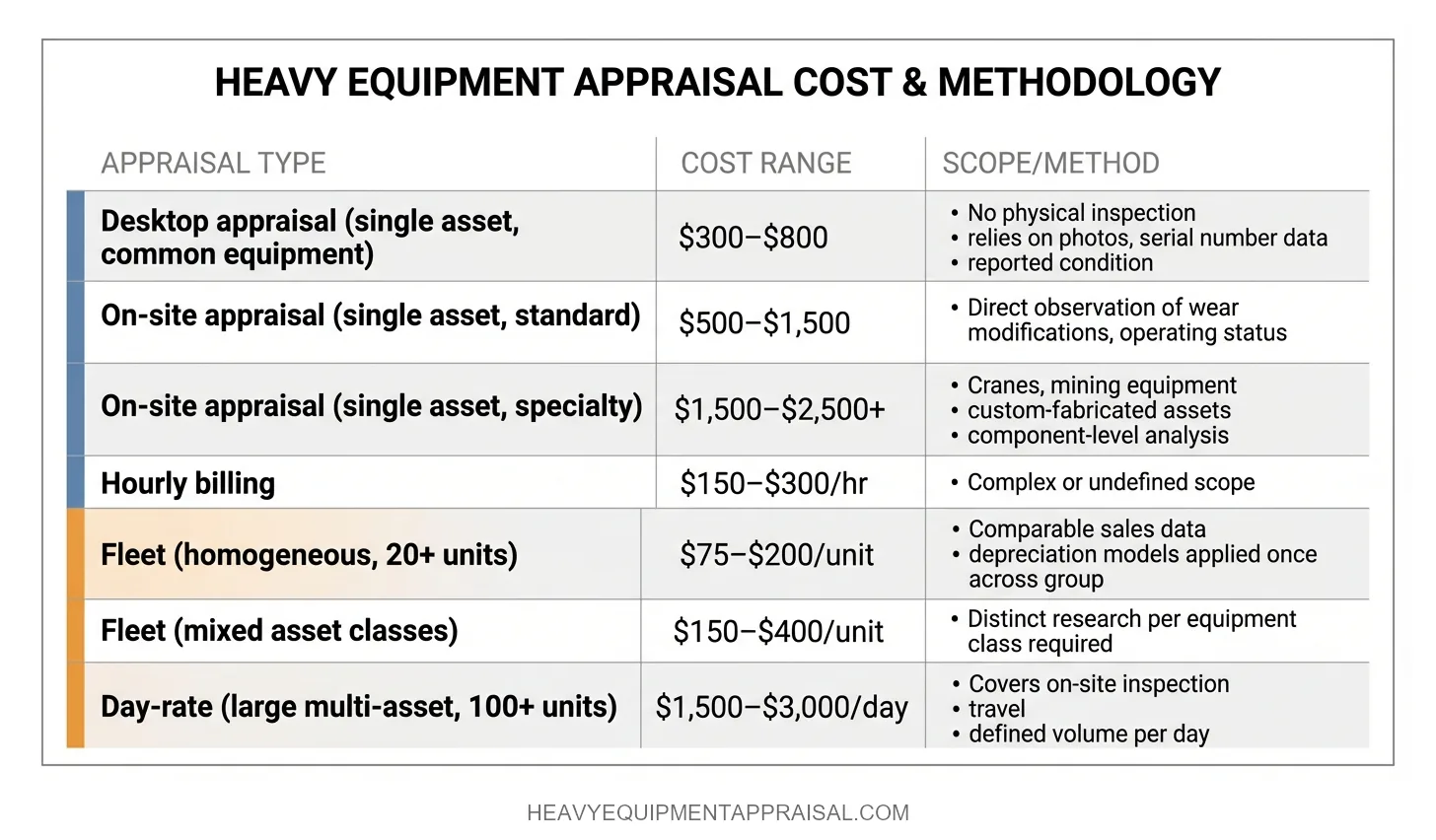

A desktop/online equipment appraisal for a single piece of common equipment (forklift, skid steer, backhoe) runs $300–$800 when market data is readily available and no physical inspection is required.

An on-site equipment appraisal for standard construction equipment ranges from $500–$1,500, rising to $2,500 or more for specialty or high-value assets like crawler cranes, large mining trucks, or custom-fabricated processing equipment.

These figures reflect USPAP-compliant certified reports from credentialed appraisers, not dealer quotes or online valuation tools.

Where scope is uncertain at the outset or the asset demands specialized research, appraisers often bill hourly rather than quoting a flat fee. Certified appraisers typically charge $150–$300 per hour depending on credential level, geographic market, and asset complexity.

| Appraisal Type | Typical Range | Best For |

|---|---|---|

| Desktop (single asset) | $300–$800 | Common equipment with strong market comps |

| On-site (single asset, standard) | $500–$1,500 | Construction equipment, titled vehicles, general industrial |

| On-site (single asset, specialty) | $1,500–$2,500+ | Cranes, mining equipment, custom or rare assets |

| Hourly rate | $150–$300/hr | Complex or undefined scope |

The price difference between desktop and on-site reflects the appraiser's time, travel, and the depth of physical condition data collected during inspection:

A desktop report relies on reported condition and available documentation. An on-site inspection produces direct observation of wear, modifications, damage, and operating status, all of which feed into more precise depreciation estimates under the cost approach.

An appraisal priced well below these ranges likely omits the scope of work, methodology documentation, or credential requirements that lenders and courts expect. The fee funds the defensibility of the final value opinion, not just the number itself.

What Drives the Price Up (or Down)

Six variables account for most of the variance between a $300 desktop report and a $2,500+ on-site engagement. Understanding each one explains why two appraisals for seemingly similar equipment can carry different fees.

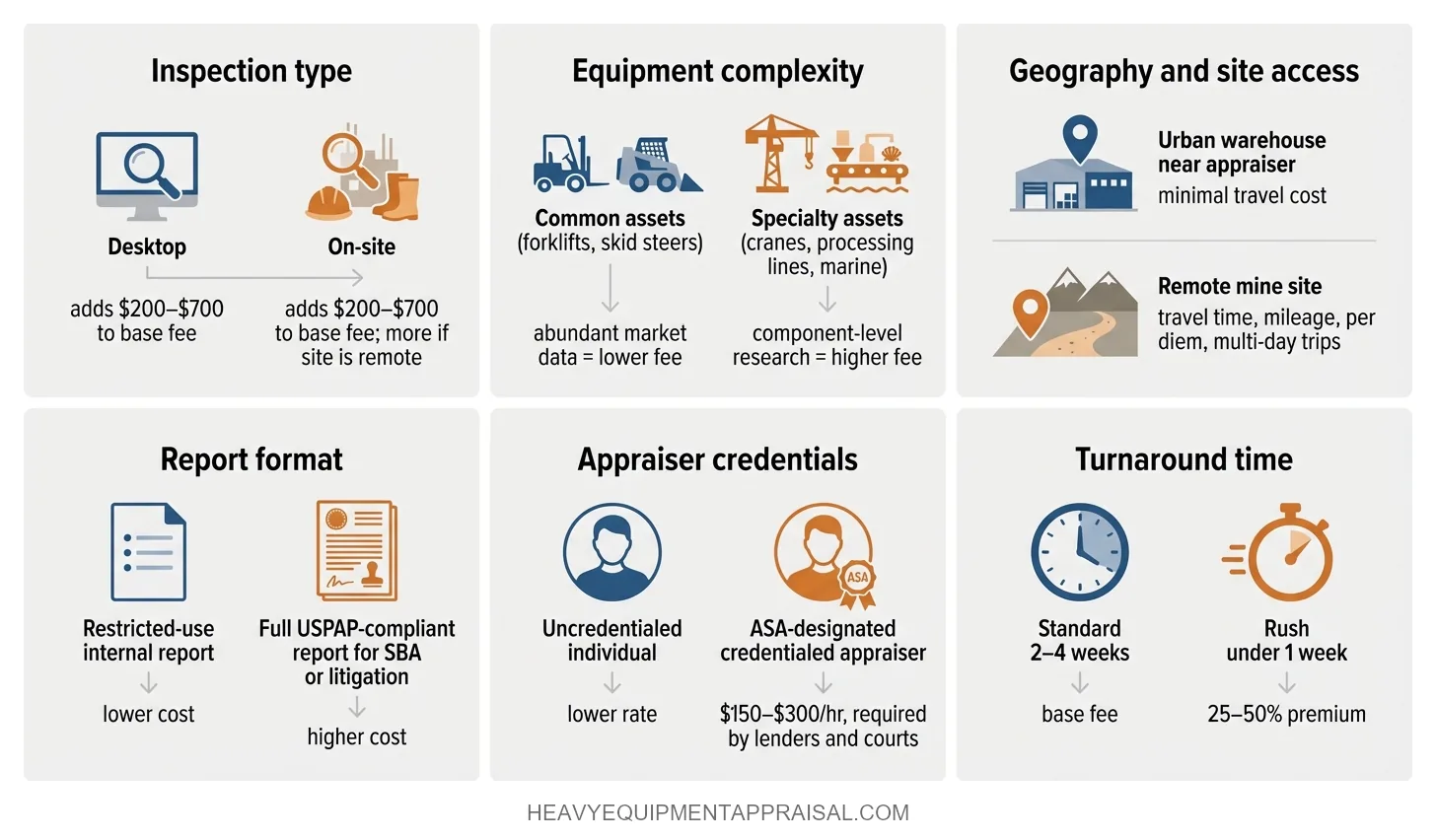

1. Inspection type (desktop vs. on-site)

The single largest cost lever. A desktop appraisal eliminates travel time and relies on photos, serial number data, and reported condition. An on-site inspection adds travel, physical examination, and direct observation of wear, modifications, and operating status. The jump from desktop to on-site typically adds $200–$700 to the base fee, more if the site is remote.

2. Equipment type and complexity

Common assets with active resale markets (forklifts, skid steers, boom lifts) appraise faster because comparable sales data is abundant. Specialty assets (custom-fabricated processing lines, bridge cranes, marine equipment) require deeper research, component-level analysis, or the cost approach with engineered depreciation. Research-intensive assets push fees toward the higher end of every range.

3. Geography and site access

An appraiser traveling three hours to a mine site in rural Nevada incurs costs that a warehouse inspection 20 minutes from the office does not. Travel time, mileage, per diem, and multi-day trips for remote locations are typically billed separately or built into the quoted fee.

4. Report format and intended use

A restricted-use summary report for internal decision-making costs less than a full USPAP-compliant appraisal report prepared for SBA lending or litigation. The more detailed the report's intended audience requirements, the more documentation, methodology narrative, and credential disclosure the appraiser must include.

5. Appraiser credentials

Credentialed appraisers holding ASA and CMEA designations command higher hourly rates than uncredentialed individuals. Those credentials signal peer-reviewed competency and adherence to professional standards, which is precisely what lenders and courts require for the report to be accepted.

6. Turnaround time

Standard delivery runs 2–4 weeks for most engagements. Rush assignments (under one week) typically carry a 25–50% premium because the appraiser must reprioritize existing work and compress research timelines.

Each of these variables maps directly to the scope of work an appraiser must perform. A broader scope produces a more thorough report, which in turn supports a value opinion that holds up under the scrutiny of lenders, attorneys, or the IRS.

Fleet and Multi-Asset Appraisal Pricing

Fleet appraisals are not priced by multiplying the single-asset rate by the number of units. Appraisers scope multi-asset engagements based on fleet homogeneity, total asset count, site logistics, and the research effort required per asset class. This produces a lower per-unit cost as volume increases.

A homogeneous fleet (50 identical late-model telehandlers across three sites, for example) appraises faster per unit than a mixed fleet because the appraiser establishes comparable sales data and depreciation models once, then applies them across the group.

Per-asset rates for homogeneous fleets of 20+ units commonly fall to $75–$200 per asset, depending on whether the engagement is desktop or on-site. A mixed fleet containing dozers, excavators, generators, welding rigs, and shop-built attachments requires distinct research for each equipment class and pushes per-unit costs higher, often $150–$400 per asset.

For large assignments (100+ assets or multi-day site inspections), appraisers frequently shift to day-rate billing rather than quoting per-unit fees. Day rates for credentialed appraisers typically run $1,500–$3,000, covering on-site inspection time, travel, and a defined volume of assets per day.

A skilled appraiser can inspect and document 25–50 pieces of common construction equipment per day on-site, fewer for complex or specialty assets that require component-level analysis. The total engagement fee then reflects the number of inspection days plus the research and report-writing time billed separately at hourly rates.

Multi-asset assignments for manufacturing facilities or integrated processing plants fall into a different tier entirely, with total fees of $3,000–$8,000+ depending on asset count, complexity, and whether the engagement involves purchase price allocation or financial reporting requirements that expand the scope of work.

The per-unit cost reduction in fleet appraisals does not mean less rigor per asset. It reflects the efficiency of inspecting and researching similar equipment in a single mobilization. Lenders reviewing collateral packages for SBA loans or ABL facilities expect each asset in the fleet to carry an individual value opinion supported by the same methodology and documentation standards as a standalone report.

How Appraisal Purpose Affects Cost

The intended use of an appraisal dictates the value type, report depth, and compliance requirements. Those scope differences produce materially different fees for what may be the same piece of equipment. An SBA lender needs a different report than a divorce attorney, and a litigation expert witness engagement carries obligations that a basic insurance valuation does not.

| Purpose | Typical Value Standard | Report Requirements | Typical Cost Impact |

|---|---|---|---|

| SBA lending | OLV (most common) | Full USPAP-compliant report per SBA SOP, individual asset values, credential disclosure | Moderate ($500–$1,500 single asset) |

| Insurance (placement/claim) | Replacement cost or FMV | Detailed cost-new research, condition documentation, coverage-grade report | Moderate to high ($500–$2,000+) |

| Litigation / expert witness | Varies (FMV, OLV, or FLV depending on case) | Full narrative report, methodology defense under cross-examination, deposition and testimony prep | High ($2,000–$5,000+ before testimony fees) |

| Estate or divorce | FMV (IRS standard for estate, court-directed for divorce) | IRS-defensible report for estate, court-admissible for divorce, detailed methodology narrative | Moderate ($500–$2,000) |

| M&A / purchase price allocation | FMV or FV (ASC 805) | Multi-asset valuation tied to financial reporting standards, coordination with transaction advisors | High ($3,000–$8,000+ for full plant) |

Litigation engagements cost the most not because the equipment is different but because the appraiser's work product must withstand adversarial challenge. Report preparation expands to include detailed methodology narratives, rebuttal analysis of opposing valuations, and time budgeted for depositions or court testimony billed at hourly rates on top of the base appraisal fee.

An M&A engagement carries comparable costs for a different reason: the asset count is typically large, the financial reporting standards (ASC 805 or ASC 360) impose specific documentation requirements, and the appraiser must coordinate timing with the transaction close.

Insurance appraisals sit in the middle range.

They require current replacement cost research and thorough condition documentation but rarely demand the adversarial-grade narrative that litigation does. SBA appraisals follow a well-defined scope under SBA Standard Operating Procedures, which keeps the process predictable and fees relatively contained for single assets.

Requesting the wrong value type for a given purpose does not just waste the fee. It produces a report that the intended user (lender, court, IRS) will reject outright, requiring a second engagement at full cost.

What Is Not Worth Paying For

A blue book estimate, dealer quote, online calculator, or report from an uncredentialed individual is not a substitute for a certified appraisal, regardless of how reasonable the price looks. These alternatives produce a number but not a defensible value opinion, and the distinction matters the moment that number must withstand scrutiny from a lender, court, or regulatory body.

Equipment blue books aggregate historical auction data into statistical averages. They do not account for the specific asset's condition, installed context, modifications, or remaining useful life.

A dealer quote reflects what one buyer would pay at one moment for resale purposes. It carries no methodology documentation, no stated assumptions, and no credential behind it. Online calculators operate on the same principle as blue books but with even less transparency about the underlying data set. None of these sources meets USPAP standards, and none produces a report that identifies a defined value type (FMV, OLV, or FLV) with the supporting methodology narrative that intended users require.

Uncredentialed reports present a subtler risk. They may look like appraisals, use appraisal terminology, and arrive in a professional format. But when a report's author lacks recognized credentials and the document does not comply with USPAP's scope of work, methodology, and reporting requirements, it is vulnerable to challenge. In litigation, courts have disqualified equipment valuations where the appraiser could not substantiate comparables or demonstrate a recognized methodology, leaving the party that relied on the report without admissible evidence and facing the cost of a replacement engagement under deadline pressure.

The FDIC draws a parallel regulatory distinction between appraisals and evaluations, accepting only USPAP-compliant reports from credentialed appraisers for transactions above certain thresholds.

The cheapest option is not the one with the lowest fee. It is the one that does not need to be repeated. A $200 report that gets rejected by an SBA lender or struck from evidence in a divorce proceeding costs the client the original fee plus $500–$2,500 for the compliant appraisal that should have been ordered first, along with whatever delays or missed deadlines the failed report caused.

How to Evaluate Whether the Cost Is Justified

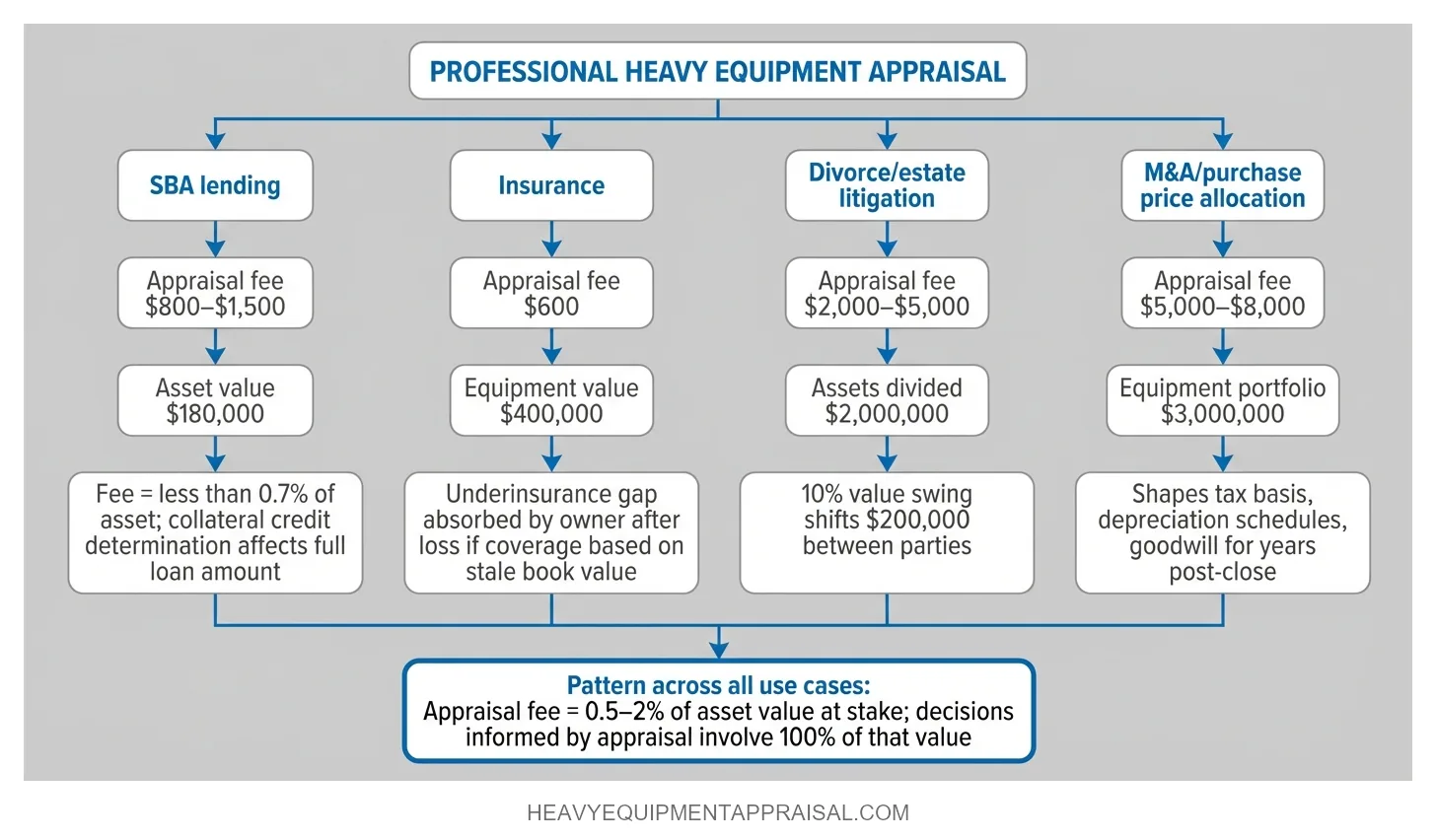

The appraisal fee is almost never the largest number in the transaction it supports. A $1,200 appraisal on a $180,000 crawler excavator backing an SBA loan represents less than 0.7% of the asset value and a fraction of a percent of the total loan package. The relevant question is not whether the fee seems high in isolation but whether the decision riding on the appraisal justifies the cost of getting the value right.

In lending, the appraisal determines how much collateral credit a lender will extend. An SBA loan secured by $500,000 in equipment hinges on the appraised orderly liquidation value. If that value comes in 15% lower because the appraiser missed installed attachments or applied generic depreciation instead of asset-specific analysis, the borrower loses access to tens of thousands of dollars in available credit. The $800–$1,500 appraisal fee is trivial against that gap.

In litigation, the stakes compound.

A divorce or estate proceeding dividing $2 million in business assets allocates real dollars based on the equipment valuation. A 10% swing in the appraised value of a fleet shifts $200,000 between parties. The appraisal fee of $2,000–$5,000 is not a cost to minimize. It is the price of a defensible position that survives cross-examination.

Insurance presents a different but equally concrete risk.

Underinsuring a $400,000 piece of equipment because the coverage was based on a stale book value rather than a current replacement cost appraisal means the owner absorbs the gap after a loss. A $600 appraisal that ensures accurate coverage pays for itself the moment a claim is filed.

M&A transactions carry the highest absolute dollar exposure. Purchase price allocation across dozens or hundreds of assets determines tax basis, depreciation schedules, and goodwill calculations for years after closing. A $5,000–$8,000 appraisal engagement on a $3 million equipment portfolio shapes annual tax deductions that dwarf the one-time fee.

The pattern across every use case is the same: the appraisal fee runs 0.5–2% of the asset value at stake, while the decisions it informs involve 100% of that value. Evaluating cost in proportion to exposure, rather than as a standalone line item, is how the fee becomes clearly justified.

An accurate, USPAP-compliant appraisal does not add cost to a transaction. It prevents the far larger cost of a flawed valuation reaching a decision-maker who acts on it.

FAQ

How much does an equipment appraisal cost for an SBA loan?

Expect an equipment appraisal for an SBA loan to cost $500 to $2,500 for standard assets and $3,000 to $10,000 for complex or high-value equipment.

What is the difference in cost between a desktop and on-site equipment appraisal?

Desktop equipment appraisals usually cost $300 to $1,000, while on-site equipment appraisals usually cost $750 to $3,000 or more because they include physical inspection and travel.

How are fleet equipment appraisals priced?

Fleet equipment appraisals are priced by the number of assets, inspection scope, and travel, with small fleets often costing $1,000 to $3,000 and large or multi-location fleets costing $5,000 to $15,000 or more.

Why does a litigation equipment appraisal cost more than an insurance appraisal?

A litigation equipment appraisal costs more than an insurance appraisal because it requires court-ready analysis, stronger documentation, and more detailed reporting.

What is the hourly rate for a certified equipment appraiser?

A certified equipment appraiser usually charges $150 to $400 per hour, depending on experience, equipment type, report purpose, and travel requirements. Standard assignments often stay near the lower end of that range, while litigation, expert witness work, and complex industrial appraisals can exceed $500 per hour.

Does appraisal purpose affect the cost of valuing the same piece of equipment?

Appraisal purpose affects equipment valuation cost because insurance and internal-use reports require less support, while SBA, tax, IRS, and litigation appraisals require stricter analysis and more detailed reporting.

How much extra does a rush equipment appraisal cost?

A rush equipment appraisal usually costs 25% to 100% more than a standard appraisal, depending on turnaround time, asset complexity, and appraiser availability. A standard $1,000 appraisal may increase to $1,250 to $2,000 on a rush basis. Same-day or next-day delivery usually creates the highest rush fee.

What makes specialty equipment appraisals more expensive than standard assets?

Specialty equipment appraisals cost more than standard asset appraisals because they require deeper market research, fewer comparable sales, higher technical knowledge, and more detailed reporting. Specialized assets such as medical, aviation, laboratory, or custom manufacturing equipment often need extra analysis to support value, which increases appraisal time and cost.

Is a blue book estimate or dealer quote a substitute for a certified equipment appraisal?

A blue book estimate or dealer quote is not a full substitute for a certified appraisal when a lender, court, IRS matter, SBA loan, or insurance carrier requires formal valuation support. Blue book estimates and dealer quotes provide pricing reference points, but a certified appraisal delivers a documented opinion of value with scope, methodology, and signed professional support.

How do I know if an equipment appraisal fee is justified for my transaction?

Justify an equipment appraisal fee by confirming that it is scope-based, set up front, and independent of the value conclusion, not tied to asset value or a percentage of value.