Rent-to-Own Heavy Equipment Guide: A Smart Path to Ownership?

While traditional equipment loans and leases are the well-worn paths to acquisition, rent-to-own heavy equipment agreements offer a unique route that, when structured properly, can be a powerful tool for business growth.

But here’s the key insight that too many operators miss: these agreements aren’t set in stone. In fact, they’re highly negotiable – if you know how to leverage equipment valuation to your advantage.

Ready to stop leaving money on the table? Let's dig into how a little strategy can transform your next rent-to-own equipment deal from a standard financing arrangement into a powerful tool for business growth.

Understanding Rent-To-Own For Heavy Equipment

What Is Rent-To-Own?

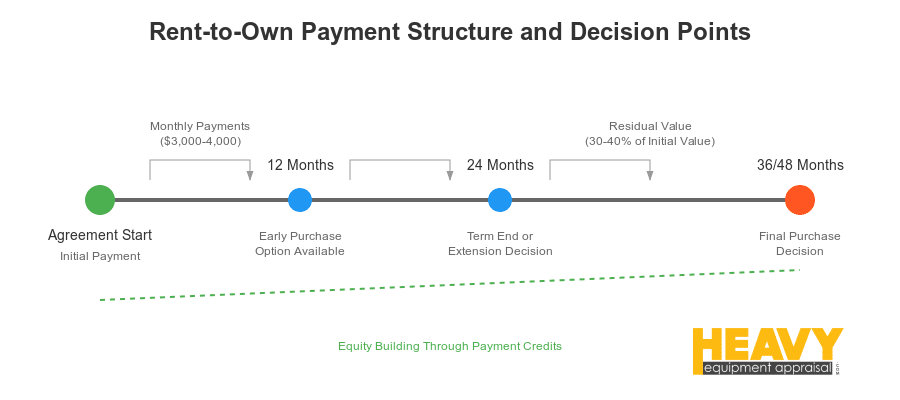

Think of a rent-to-own agreement as a hybrid between a rental and a financing arrangement. You get immediate access to the equipment you need, making regular payments over a defined period - typically 24, 36, or 48 months.

Here's the strategic advantage:

Unlike a traditional lease where your payments just buy time with the equipment, a portion of each payment in a rent-to-own setup is credited toward eventual ownership. You maintain the option - not the obligation - to purchase the equipment when the term ends.

How Does Rent-To-Own Heavy Equipment Work?

The mechanics are straightforward, but understanding the nuances is where real value gets unlocked.

During your rental term, you make your monthly payments, which cover both equipment use and your path to ownership. A predetermined percentage of each payment gets credited toward your purchase price.

When the term ends, you've got a choice to make: buy the equipment for the remaining balance (based on its residual value) or walk away. That residual value? It's the equipment's estimated market value at term's end, accounting for depreciation and wear. And this is exactly where having a professional appraisal in your corner can save you thousands.

Pros And Cons Of Rent-To-Own

In our decades of equipment valuation experience, we've seen rent-to-own work brilliantly for some operations and become a burden for others. It's particularly powerful for businesses that:

- Need quick equipment access without tying up capital

- Are working with less-than-perfect credit

- Want to test equipment in real operations before committing

The advantages are clear: immediate equipment access, potential ownership, and the flexibility to test before you commit. But let's be candid about the downsides: you're typically looking at higher overall costs compared to traditional financing, you don't own the equipment until you exercise that purchase option, and if you don't complete the purchase, those payments you've made? They're gone.

The Impact Of Equipment Appraisals On Rent-To-Own Terms

Let's cut straight to what matters in equipment valuation: how it affects your bottom line. After appraising equipment across every sector imaginable, we've seen firsthand how the right valuation can be the difference between a good deal and a great one.

Why Equipment Condition Matters

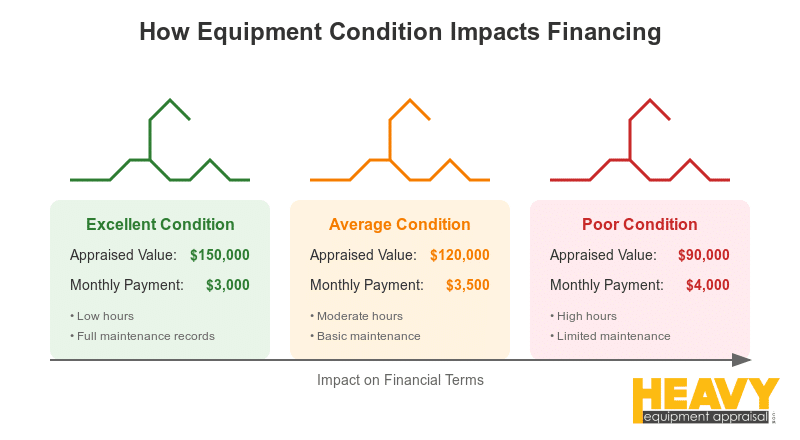

Here's where your operational expertise becomes a financial advantage. The condition of heavy equipment isn't just about whether it runs well - it's about how that condition translates into appraised value.

Think about it this way: When we assess equipment condition, we're looking at the whole picture:

- Age of the machine

- Usage hours on the clock

- Maintenance records (they're worth more than you think)

- Existing wear patterns

- Component life remaining

A professional equipment appraisal transforms these factors into negotiating power. Take two identical excavators: One has 5,000 hours and maintenance records that would make a fleet manager proud. The other's got 10,000 hours and a "run it till it breaks" history. Same model, dramatically different appraised values.

How Appraisals Influence Financing Terms

Let's talk leverage. Your equipment's appraised value isn't just a number - it's the foundation of your entire rent-to-own agreement. Here's what we've seen in the field:

- Higher appraised value → Lower monthly payments

- Higher appraised value → Reduced purchase price at term end

- Higher appraised value → Less risk for the lender = Better terms for you

It works the other way too. A lower appraised value often means higher monthly payments and a steeper purchase price at the end. This isn't just theory - a recent Equipment Leasing and Finance Foundation report found that accurate appraisals can cut financing costs by up to 15%.

Case Study: Appraisal-Driven Savings

Let me share a real-world win we recently saw. A construction outfit was eyeing a used bulldozer through rent-to-own. The lessor's initial offer was based on a quick once-over of the machine - pretty standard practice, but not exactly thorough.

Here's where it gets interesting: After getting a professional appraisal that documented the bulldozer's excellent condition and surprisingly low hours, this company walked back to the negotiating table with real leverage. The result? They shaved over $10,000 off the purchase price.

Key Factors In Heavy Equipment Appraisals

Let's break down what actually moves the needle on equipment value. After thousands of appraisals, we've zeroed in on the factors that matter most to your bottom line.

Age And Usage Hours

Every piece of heavy equipment tells a story through two key metrics: age and usage hours.

Think of age as the calendar view - how many years the equipment's been in service. But usage hours? That's where the real story unfolds. It's the equivalent of mileage on a car, showing how hard that machine's actually worked.

Here's the reality we see in the field: A 5-year-old backhoe with 8,000 hours typically commands less value than a 3-year-old model with 4,000 hours - assuming similar maintenance. It's not just about time; it's about intensity of use.

Maintenance History

If usage hours tell us how much a machine has worked, maintenance history tells us how well it's been cared for. And let me tell you - this factor can swing value dramatically.

Equipment with documented service records showing regular:

- Oil changes

- Filter replacements

- Routine maintenance

- Timely repairs

These maintenance logs aren't just paperwork - they're proof of value. We consistently see higher appraised values for well-maintained equipment, while machines with spotty maintenance histories take a hit due to increased mechanical risk.

Market Demand

Market demand isn't just some abstract economic concept - it's cold, hard cash in your pocket. High demand for that late-model skid steer loader? That translates directly into higher appraised value.

But markets shift. Older specialized equipment often sees declining appraised values as demand drops off. It's not about the machine becoming less capable - it's about what the market's willing to pay.

Technological Obsolescence

Here's where timing gets crucial. Technological obsolescence can hit equipment value hard, even when everything's running perfectly.

Take that 10-year-old bulldozer with manual controls. Solid machine, probably works great. But put it next to a new model with GPS-guided technology? The value gap isn't just about age - it's about capability and efficiency.

When newer models hit the market with advanced features, older equipment values often take a hit. It's not fair, but it's reality - and it's something you need to factor into your equipment strategy.

Comparing Rent-To-Own With Other Financing Options

Let's cut through the financing fog. After analyzing thousands of equipment deals, here's what you need to know about each path to equipment ownership.

| Feature | Rent-to-Own | Traditional Loan | Lease | Cash Purchase |

|---|---|---|---|---|

| Ownership | Option to own at term end | Immediate ownership | No ownership | Immediate ownership |

| Monthly Payments | Moderate ($3,000-3,500) | High ($3,500-4,000) | Low ($2,500-3,000) | None |

| Upfront Costs | Minimal (1-2 payments) | Down payment (10-20%) | Security deposit | Full amount |

| Flexibility | High - option to buy or walk away | Low - locked in | Medium - return option | Very low - capital tied up |

| Overall Cost | Higher than loan, lower than lease | Moderate (4-15% interest) | Highest total cost | Lowest total cost |

This table uses standard markdown formatting that should paste cleanly into WordPress. The bold headers and simple structure make it easy to read and understand. Would you like any adjustments to the format or content?

Traditional Loans

Here's where equipment acquisition gets interesting. While rent-to-own builds equity over time, traditional loans put you in the driver's seat from day one.

Think of a heavy equipment loan as the straightforward path: borrow money, buy equipment, make payments. You own it from the start - but that also means you're on the hook for those loan payments, come what may.

A word about the numbers: The Small Business Administration tells us equipment loan interest rates typically run 4% to 15%, depending on your credit profile. This is where the rubber meets the road in terms of total cost.

Leasing

Now let's talk leasing - the "try before you buy" of the equipment world.

A heavy equipment lease keeps those monthly payments lower, but here's the catch: when the music stops, you don't own the chair. At lease end, that equipment goes back to the lessor.

We've seen leasing work beautifully for:

- Businesses needing equipment flexibility

- Operations wanting lower monthly payments

- Projects with specific equipment timelines

- Companies avoiding long-term commitments

Lease terms typically run 12 to 60 months. Your mileage may vary based on equipment type and lessor requirements.

Cash Purchase

Sometimes the old ways are the best ways. A cash purchase is exactly what it sounds like: you pay cash, you own equipment. Simple.

The upside? No financing costs, immediate ownership, and total control. The downside? You're tying up significant capital that could be used elsewhere in your operation.

This strategy shines when:

- You've got the capital available

- You want to avoid financing costs

- Tax advantages align with your strategy

- You're confident about long-term equipment needs

But remember - capital tied up in equipment isn't working anywhere else in your business.

Navigating The Rent-To-Own Process

After guiding countless businesses through equipment acquisitions, we've developed a roadmap that turns complex financing decisions into strategic advantages. Here's where the rubber meets the road.

Determining Your Equipment Needs

This is where smart operators separate themselves from the pack.

Start by drilling down into your exact equipment needs. We're talking specifics here:

- Equipment type

- Make

- Model

- Required condition

Every project has its own demands. A landscaping operation might need a compact track loader that can dance through tight spaces, while a construction outfit might require an excavator that can move mountains.

This isn't just about what you need today - it's about positioning your operation for tomorrow's opportunities.

Getting A Professional Appraisal

Here's where we see too many operators leave money on the table.

Before you sign anything, get a professional equipment appraisal. This isn't just paperwork - it's your negotiating leverage. A certified appraiser digs into the details that matter:

- Equipment condition

- Age

- Usage hours

- Maintenance history

Think of this as your secret weapon in negotiations. We've seen solid appraisals save operators tens of thousands in purchase price adjustments.

Negotiating Terms

Let's talk strategy. Once you've got your appraisal in hand, you're ready to negotiate. Focus on three key areas:

- Monthly payments

- Purchase price

- Associated fees

Don't just accept the first offer. Research similar equipment rates. Know your market. And most importantly - use your appraisal data to back up your position.

Pro tip: The best deals often come from showing lessors you understand both the equipment and the numbers.

Understanding The Contract

Time for the fine print. Here's what you absolutely must review:

- Payment schedule

- Purchase option details

- Early termination clauses

- Late payment penalties

But don't just read - understand. If something's unclear, ask. If you need legal eyes on it, get them. We've seen too many solid operators get burned by contract details they glossed over.

Remember: This document determines your financial commitment for years to come. Take the time to get it right.

Tips For Maximizing Value In A Rent-To-Own Agreement

After decades in equipment valuation, here's what separates the deals that build wealth from those that drain it. This is where equipment value becomes a strategic asset - if you know how to play it right.

Maintaining Equipment Properly

Let's talk brass tacks about maintenance.

Here's what smart operators know: Every maintenance record is a value-building document. We're talking about:

- Regular oil changes

- Filter replacements

- Routine inspections

- Documented repairs

This isn't just about keeping equipment running - it's about maintaining its condition and protecting your future purchase price.

Those maintenance logs you're keeping? They're not just paperwork - they're negotiating power. We've seen proper documentation knock thousands off final purchase prices.

Understanding Residual Value

Here's where the real money is made (or lost).

The residual value is your equipment's estimated worth at agreement's end. But here's what most operators miss: this number isn't set in stone. It's a key negotiating point that directly impacts your final purchase price.

Smart play? Negotiate that residual value upfront. Because surprises in equipment financing? They usually come with dollar signs attached.

Planning For Potential Purchase

Time to think chess, not checkers.

If you're eyeing that purchase option - and our data shows most operators are - start planning now. Here's your playbook:

- Start saving for that final purchase price early

- Set aside a portion of monthly payments

- Build your purchase fund systematically

- Keep your options open

This isn't just about having cash ready. It's about maintaining flexibility as market conditions change.

And here's something we've seen repeatedly: operators who plan their purchase strategy from day one typically secure better terms than those scrambling at the last minute.

One client put it perfectly: "The machine was great, but having a clear purchase plan from the start? That's what saved me thousands."

Common Pitfalls To Avoid In Rent-To-Own Agreements

Listen, we've seen enough deals to write a book about what not to do. But let's focus on the biggest value-killers.

Overlooking Hidden Fees

You know what can turn a good deal sour real quick? Those sneaky fees nobody mentioned upfront:

- Origination fees

- Late payment penalties

- Processing charges

Every fee you don't spot is profit you're leaving on the table. Always ask about ALL potential charges. Then ask again.

Ignoring Early Purchase Options

Here's something that might surprise you: Sometimes the best deal is the one you make early.

Many agreements include early purchase options at a discount. Miss these, and you might be paying full term when you didn't have to. We've seen operators save up to 20% by exercising early purchase options strategically.

Neglecting Insurance Requirements

This one's simple but critical: Know your insurance obligations.

Throughout the rental term, you need proper coverage. But here's what we often see overlooked:

- Specific coverage requirements

- Deductible limits

- Notification procedures

One missing insurance detail can cost you more than years of careful negotiation saved you.

Future Trends In Heavy Equipment Rent-To-Own

The equipment financing landscape isn't standing still. After tracking market shifts across every sector, we're seeing evolution in real time.

What's catching our eye? The industry is moving toward more flexible agreements that match your actual business cycles. Think customized payment structures that align with your cash flow patterns.

Technology integration isn't just changing the equipment - it's revolutionizing how we track and manage it. Some cutting-edge operators are already using rent-to-own agreements that include GPS tracking and remote diagnostics. This isn't just about knowing where your equipment is - it's about predicting maintenance needs before they become expensive problems.

And here's something that's reshaping the market: sustainability and eco-friendly equipment options. We're seeing growing demand for energy-efficient machines, and financing terms are starting to reflect this shift.

Conclusion: Is Rent-To-Own Right For You?

In today's equipment market, the real challenge isn't just acquiring machines - it's structuring deals that build your operational strength while protecting your capital.

That's where rent-to-own shines, when done right. It bridges the gap between immediate needs and long-term ownership, giving you flexibility that traditional financing can't match. But here's the key: your negotiating power lives and dies by your appraisal strategy.

We've seen it time and again across every sector - operators who leverage professional appraisals consistently secure better terms, lower monthly payments, and more favorable purchase options. One construction outfit recently saved $10,000 on a single bulldozer deal, simply by bringing solid valuation data to the table.

Ready to explore rent-to-own for your operation? Start with a certified equipment appraisal. Because in this market, knowledge isn't just power - it's profit in your pocket.