Heavy Equipment Loan vs Lease Strategy: Beyond Monthly Payments

Equipment loan vs lease decisions impact far more than your monthly payments. In fact, choosing the wrong equipment financing structure could cost your operation $50,000+ per million in equipment value – yet most businesses miss the strategic implications of this choice.

We’re seeing a shift in today’s market: traditional equipment loans provide ownership and tax advantages, while equipment leases offer flexibility and lower upfront costs. But here’s what really drives value: your ability to leverage each option’s unique advantages for different parts of your fleet.

Consider this: Top-performing equipment fleets often combine both loans and leases strategically – financing core machinery while leasing specialized or seasonal gear. This hybrid approach preserves capital while building long-term equity.

Ready to optimize your equipment acquisition strategy? Let's explore how to structure loans and leases for maximum operational impact.

Understanding Heavy Equipment Financing Options

Heavy equipment financing and heavy equipment leasing represent two distinct paths to acquiring the equipment your business needs. Understanding these fundamental approaches is crucial for making decisions that align with your operational and financial objectives.

What is Heavy Equipment Financing?

Heavy equipment financing refers to the process of obtaining funds to purchase heavy equipment through a loan. This is where ownership begins day one - once you've secured financing, that excavator or loader becomes a true business asset. The borrower makes regular payments over a set period, and after the loan is paid off, they own the equipment outright.

Think of it as similar to a traditional auto loan, but with terms and conditions specifically designed for the heavy equipment industry. These arrangements often involve larger loan amounts and longer repayment periods to match the substantial investment these machines represent.

What is Heavy Equipment Leasing?

Heavy equipment leasing takes a different approach. Instead of building ownership, you're securing the right to use the equipment for a specified period, with options to purchase, return, or renew when the lease term ends. With a heavy equipment lease, the lessee doesn't take immediate ownership. Instead, they make regular payments to the lessor for equipment use.

At lease end, you typically have three paths forward:

- Purchase the equipment at a predetermined price

- Return it to the lessor

- Renew the lease

This structure mirrors commercial property leasing - you're paying for use rather than building equity. For seasonal operations or businesses needing equipment flexibility, this can be an advantage rather than a limitation.

Key Factors to Consider: Equipment Loans vs. Leases

When evaluating financing versus leasing, several key factors come into play. Each impacts your business's cash flow and long-term financial health in distinct ways.

| Factor | Equipment Loan | Equipment Lease |

|---|---|---|

| Upfront Cash | 15-25% down payment Typically $15-25K per $100K value |

0-5% down payment Often just first/last payment |

| Monthly Payment | Lower $1,600-1,800 per $100K borrowed |

Higher $2,000-2,200 per $100K value |

| Tax Impact | Interest + Depreciation Section 179 eligible |

100% Payment Deductible Simpler tax treatment |

| Total Cost (5-Year $100K Example) |

$116K Total Plus equipment ownership |

$132K Total Plus purchase option |

Pro tip: These numbers reflect industry averages - professional appraisals often unlock better terms.

Ownership and Equity

With a heavy equipment loan, you gain immediate ownership of the equipment and begin building equity over time. Each payment increases your ownership stake, and eventually, the equipment's full value becomes an asset for your business.

Leasing operates differently - you don't own the equipment during the lease term. While you have full use rights, you're not building equity. However, you may have the option to purchase the equipment at lease end, but until then, no equity accumulates.

Financial Implications

The financial dynamics of loans and leases differ significantly:

With a loan:

- Larger upfront cost via down payment

- Interest payments on the loan amount

- Generally lower monthly payments

- Equipment ownership after final payment

- Maintenance responsibility falls to you

With a lease:

- Little or no down payment required

- Higher monthly payments typically

- No equity building

- More accessible for businesses with limited capital

Tax Benefits

Tax implications vary between financing and leasing, and this is where strategic planning becomes crucial. With a loan, you can:

- Deduct loan interest as a business expense

- Depreciate equipment value over time

- Reduce taxable income through these deductions

Leasing often allows for full lease payment deductions as business expenses, potentially offering significant tax savings. However, specific benefits depend on your individual circumstances and current tax laws, such as Section 179 of the IRS code.

The Role of Heavy Equipment Appraisal in Financing and Leasing

A professional heavy equipment appraisal isn't just paperwork - it's leverage in securing favorable financing terms.

We've seen firsthand how the appraised value directly impacts both loan amounts and interest rates. This unbiased, objective assessment provides a clear market value foundation that both lenders and borrowers can trust, especially crucial given the diverse range of equipment types, from excavators to specialized agricultural machinery.

How Appraisals Impact Loan Terms

Let's talk real numbers - this is where precise valuations unlock better terms. The appraised value of heavy equipment directly determines what a lender will offer. A higher appraisal can mean a lower interest rate and larger loan amount, while a lower appraisal often results in less favorable terms.

Consider a Caterpillar 336 excavator scenario we recently handled:

- Appraised at $250,000 → $225,000 loan at 5.5% interest

- Same machine at $180,000 → $162,000 loan at 6.75% interest

According to the Equipment Leasing and Finance Association (ELFA), these valuation discrepancies create significant financial risks for both parties. These figures reflect current market conditions, though actual rates and amounts vary based on multiple factors.

Influence of Appraisals on Lease Rates

The impact of professional appraisals extends even further into leasing arrangements. The residual value - what the equipment is worth at lease end - becomes a critical factor. A higher initial appraisal typically leads to lower monthly lease payments because lessors can project stronger resale value.

Take a recent John Deere 824L wheel loader case:

- $300,000 appraisal → $4,000 monthly lease payment

- $220,000 appraisal → $4,700 monthly lease payment (Assuming identical lease terms)

The Importance of Professional Equipment Appraisal

This is where experience in equipment valuation becomes crucial. A certified appraiser delivers something online valuation tools can't match: an unbiased, market-calibrated assessment that reflects current conditions, including regional variations and equipment-specific factors. This comprehensive evaluation provides the documentation lenders and lessors require for their due diligence processes, adhering to industry standards like those set by the American Society of Appraisers (ASA).

Comparing Financing and Leasing Options

Both financing and leasing have their own set of advantages and disadvantages. The best option for your business will depend on your specific needs and priorities, and a thorough analysis of your situation is crucial.

| What You Get | Equipment Loan | Equipment Lease |

|---|---|---|

| Control & Ownership | Full control from day one Modify it, paint it, name it Bob - it's yours |

Limited control Think of it like a rental with benefits |

| Cash Flow Impact | Bigger bite upfront But lower monthly payments keep cash flowing |

Walk in light, walk out equipped Higher monthly, but minimal upfront hit |

| Long-term Value | Build equity with every payment Like forcing savings into iron & steel |

No equity building Trading ownership for flexibility |

| Equipment Updates | You're in it for the long haul Upgrades mean new financing |

Swap up when tech changes Keep your fleet cutting-edge |

| Maintenance Reality | It's all on you But you control quality & timing |

Often included Less hassle, more predictable costs |

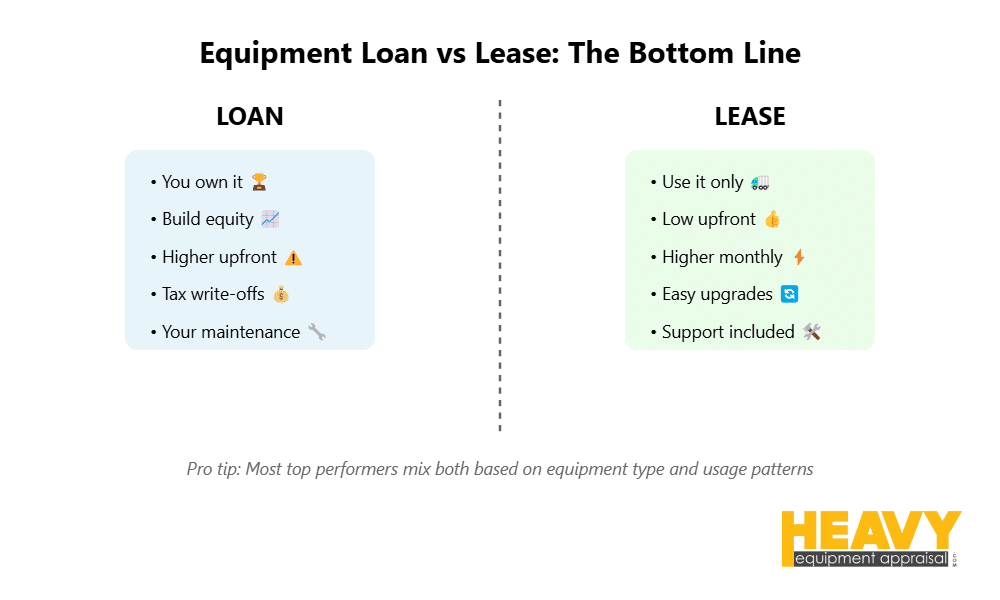

Strategic insight: Most top performers mix both - financing core fleet while leasing specialized gear. This isn't about picking sides - it's about playing to each option's strengths.

Pros and Cons of Equipment Financing

Equipment financing offers the advantage of ownership and the potential to build equity over time. Pretty interesting shift we're seeing here - operators who take the ownership route gain complete equipment control, opening doors for custom modifications that boost productivity. Those tax deductions? They're not just paperwork - interest and depreciation benefits can transform your bottom line.

But here's the real talk: equipment financing isn't all upside. You're looking at higher long-term costs, less wiggle room with upgrades, and that upfront investment hits different. Just last week, we worked with a construction outfit that financed their bulldozer fleet - made perfect sense for them because they're in it for the long haul, planning to run these machines for the next decade.

Pros and Cons of Equipment Leasing

Equipment leasing provides greater flexibility and lower upfront costs. This is where things get interesting - we're seeing more operators secure the gear they need with minimal down payment, making growth accessible even with limited capital. Want to stay cutting-edge? Leasing lets you upgrade when technology shifts, rather than getting stuck with yesterday's specs.

The trade-off? No ownership at lease end, and those tax benefits hit differently than with financing. Real example: Recently watched a landscaping crew make this work beautifully - they needed specialized trenchers but only for seasonal pushes. Leasing gave them exactly what they needed: flexibility without the long-term commitment.

Comparative Cost Analysis

The overall cost implications of financing versus leasing run deeper than most equipment dealers will tell you. Here's what we've learned from thousands of equipment valuations: your financing structure impacts everything from maintenance budgets to future buying power.

Feature Comparison: Equipment Financing vs. Leasing

Let's break down the key differentiators that actually matter in the field:

| Feature | Equipment Financing | Equipment Leasing |

|---|---|---|

| Ownership | Yes | No |

| Upfront Cost | Higher | Lower |

| Monthly Payments | Lower | Higher |

| Long-Term Cost | Potentially Higher | Potentially Lower |

| Flexibility | Lower | Higher |

| Equity | Yes | No |

| Tax Benefits | Depreciation & Interest Deductions | Potential Lease Payment Deductions |

Making the Right Choice for Your Business

This is where equipment expertise meets business strategy. We're looking at a decision that impacts not just your current operations, but your long-term growth trajectory. The right choice depends on your specific business needs, financial position, and operational goals.

Assessing Your Business Needs

Every business we work with has unique equipment requirements. Take a moment to consider:

- Your budget realities

- Expected equipment lifespan

- Usage frequency

- Growth projections

- Whether you'll need future upgrades

If you plan to use equipment for a long time and want to build equity, financing often proves the better path. However, if you need greater flexibility and lower upfront costs, leasing might better serve your objectives. Consider how a startup construction company might choose leasing to preserve capital, while an established operator may prefer financing to build long-term assets.

Long-term vs. Short-term Considerations

Here's something we see often in the field: Long-term considerations go beyond simple monthly payments. A comprehensive evaluation must include:

- Total cost of ownership

- Potential for building equity

- Equipment's long-term value

- Future buying power

For example, a farm using a combine harvester for just a few weeks each year might find leasing more practical than purchasing. The equipment's value proposition changes dramatically based on usage patterns.

When to Choose Financing

Financing typically makes more sense when:

- Your operation requires long-term equipment use

- You want to build equipment equity

- You have sufficient down payment capital

- Equipment customization matters

- Tax depreciation benefits align with your strategy

When Leasing Makes More Sense

Consider leasing heavy equipment when you need:

- Minimal upfront costs

- Equipment upgrade flexibility

- To avoid maintenance responsibility

- Off-balance-sheet financing

- To maximize lease payment tax deductions

Additional Considerations

Beyond the core financial and ownership aspects, several other factors influence your equipment acquisition strategy. Let's examine what actually moves the needle in real-world operations.

Maintenance and Repair Responsibilities

This is where the rubber meets the road in equipment operations. With a heavy equipment loan, you're the owner - which means every maintenance decision and repair cost falls to you. While this represents an additional expense, it also gives you complete control over your equipment's care and upkeep.

Under a lease, maintenance responsibilities vary significantly based on your agreement type:

- Full-service lease: The lessor handles maintenance and repairs

- Net lease: You manage all maintenance requirements

- Customized agreements: Responsibilities get divided based on negotiated terms

For example, a full-service lease on an excavator might include regular maintenance and repairs, while a net lease leaves these costs entirely in your hands. This isn't just about monthly costs - it's about operational control and equipment reliability.

Flexibility and Upgradability

Equipment needs evolve. In construction and heavy industry, staying competitive often means keeping pace with technological advances. Here's how your financing choice impacts your ability to adapt:

Leases often provide greater flexibility for equipment upgrades, allowing you to:

- Switch to newer equipment at lease end

- Adapt to changing project requirements

- Access the latest technology

- Avoid getting locked into outdated machinery

With financing, you're typically committed to the equipment for the duration of the loan term. While this builds equity, it might leave you operating older technology longer than ideal.

End-of-Term Options

Your end-game matters as much as your entry strategy. Each path offers distinct advantages as you approach term completion:

End-of-term options typically include:

| Financing (Loan) | Leasing |

|---|---|

| Complete ownership | Purchase option at preset price |

| Asset sale flexibility | Equipment return |

| Trade-in potential | Lease renewal |

| Continued use without payments | Equipment upgrade opportunity |

Understanding these options early helps you plan your equipment strategy. Consider a construction company that needs to maintain cutting-edge technology - the equipment return option in leasing might align perfectly with their upgrade cycle.

Additional Operational Factors

Consider these real-world impacts:

- Seasonal business cycles

- Regional market variations

- Industry-specific regulations

- Current economic conditions

- Technology advancement trends

- Environmental requirements

Each factor influences your total cost of operation. A mining operation in Alaska faces different considerations than a construction company in Florida - your equipment strategy needs to reflect these realities.

Equipment Loan vs Lease Decision Time: Balancing Cost, Flexibility, and Ownership

In equipment financing, the difference between adequate and optimal terms often comes down to valuation. The best strategies we see combine financing and leasing elements based on specific operational needs and growth trajectories.

Here's what drives success in today's market:

- Professional appraisals that give you leverage in negotiations

- Strategic mix of financing and leasing based on usage patterns

- Tax-optimized structure that matches your cash flow

- Flexibility reserves for technology upgrades and market shifts

Your most powerful next step? Get professional appraisals for your critical equipment. In a market where lenders scrutinize every detail, certified valuations don't just document worth - they create negotiating power.

Looking to optimize your equipment strategy? Let's talk about how professional valuation can strengthen your position.