How to Get an Equipment Loan in 2025: What Bank Data Analysis Reveals

Picture this: Your competitor just landed a major contract because they had the right equipment. Meanwhile, your growth is stalled because that vital piece of machinery sits just out of reach.

It doesn’t have to be this way.

Smart equipment financing isn’t just about getting approved – it’s about leveraging your current fleet’s value to unlock growth opportunities. In today’s market, knowing how to navigate equipment loans often makes the difference between winning and losing bids.

Here’s what most operators miss: Your equipment’s appraised value isn’t just a number – it’s negotiating power. We’ve watched businesses transform $200,000 machinery valuations into $250,000 lending opportunities simply by documenting their equipment’s true market worth.

This “how to get an equipment loan” guide cuts through the noise to show you exactly how to:

Whether you're eyeing that first excavator or managing a fifty-machine fleet, this playbook gives you the insider knowledge to secure financing that fuels growth, not just equipment acquisition.

You'll want to stick around for this part: how equipment appraisals directly impact your financing terms, and why this matters more than most lenders will admit.

Understanding Equipment Loans

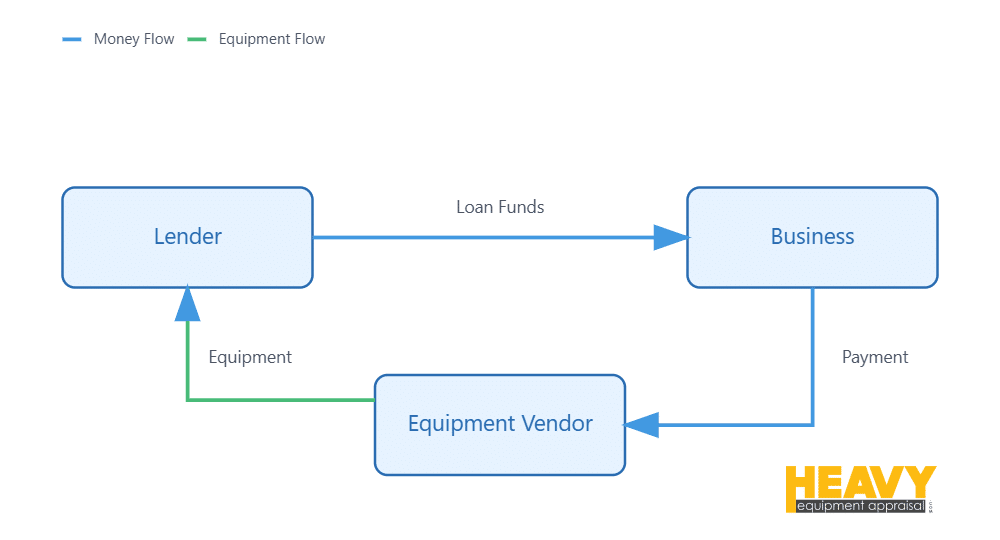

What Is An Equipment Loan?

Let's cut through the financial jargon and talk about what an equipment loan really is in today's market.

Think of an equipment loan as your business's growth lever. Whether you're running a small landscaping outfit or managing a major construction fleet, these loans serve one crucial purpose: they let you acquire the equipment you need without depleting your war chest.

I'll be straight with you – after two decades in equipment valuation, I've seen how the right financing approach can transform a business. Take that small landscaping operation we worked with last month. They used an equipment loan to add a new zero-turn mower to their fleet. Simple enough, right? But here's where it gets interesting: by preserving their cash reserves, they maintained the flexibility to take on larger contracts they would have had to pass on otherwise.

Types Of Equipment Loans

After appraising equipment for thousands of financing deals, I've seen every lending structure imaginable. Let me break down the options that consistently deliver results for operators like you:

Secured Equipment Loan

This is your workhorse financing option. The equipment itself serves as collateral, which typically gets you better rates. We're seeing operators leverage this option more than ever, especially in the current market.

Unsecured Equipment Loan

No collateral required, but you'll need solid financials and credit history. Interest rates run higher, but for some operators – especially those with strong credit and rapid growth needs – this flexibility proves invaluable.

Term Loan

Straightforward and predictable. You get a lump sum and repay it over 1-10 years. The fixed payment schedule helps with budgeting and cash flow planning.

Equipment Financing Agreement (EFA)

This structure keeps things simple: the lender maintains ownership until you've paid in full. It's particularly useful when you want to avoid the complexities of traditional loans.

Sale-Leaseback

Here's a strategic play we've seen work wonders: sell your existing equipment to a lender and lease it back. It frees up capital while keeping your operations running smooth.

Where to Find These Loans

In today's market, you've got options. Each lender brings something different to the table:

- Banks: Your go-to for competitive rates if you've got an established business

- Credit Unions: Often offer favorable terms, especially if you're already a member

- Online Lenders: Fast processing, more flexible on credit requirements

- Equipment Dealers: Direct financing that can streamline your purchase

- Independent Financing Companies: Specialists who understand your industry's unique needs

Benefits Of Equipment Financing

Let's talk strategy. Equipment financing isn't just about getting machines – it's about positioning your business for growth. Here's what we're seeing successful operators achieve:

- Cash Flow Enhancement: Spread costs over time while keeping your capital working for you

- Growth Enablement: Take on larger projects with confidence

- Tax Advantages: Section 179 benefits can significantly reduce your tax burden

- Competitive Edge: Access to the latest tech without massive capital outlays

Qualifying For An Equipment Loan

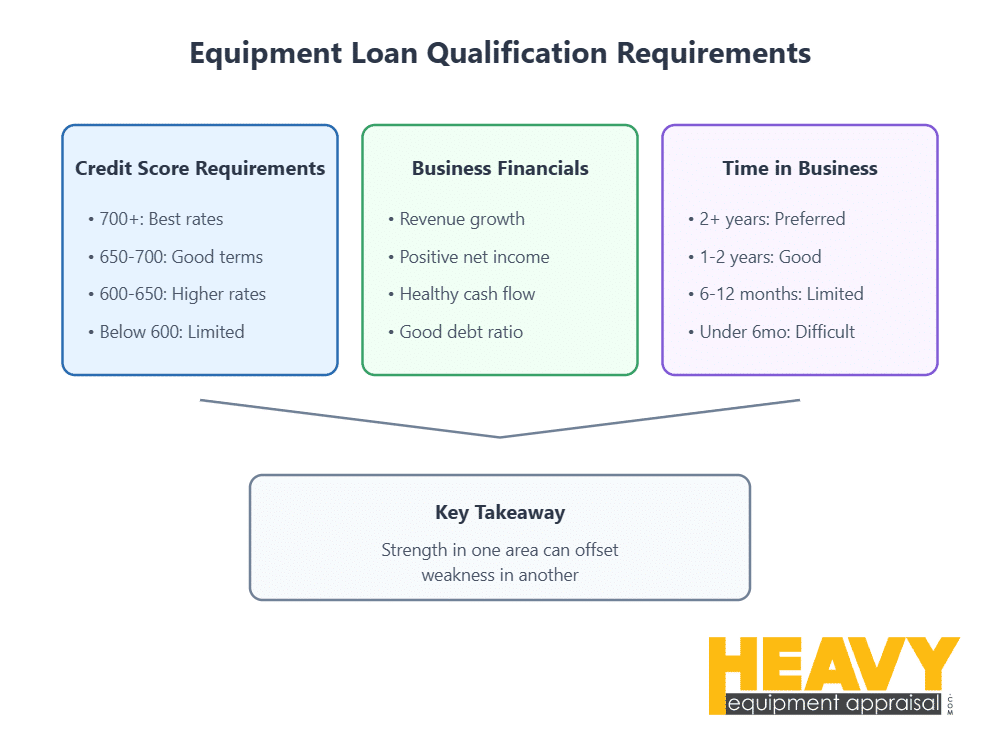

Credit Score Requirements

Let's get real about credit scores for a moment.

After guiding countless operators through the financing process, I can tell you that while credit scores matter, they're not the whole story. Here's what you need to know:

A score above 700? You're in the sweet spot for premium rates. Below 600? You've got options, but they'll come at a price.

But here's something most guides won't tell you: we've seen plenty of successful equipment loans go to operators with less-than-perfect credit when they had strong business fundamentals and proper equipment valuations to back them up.

Business Financial Requirements

This is where the rubber meets the road. Lenders want to see the story your numbers tell about your business health. Here's what catches their eye:

- Revenue trends that show consistent growth

- Profit margins that demonstrate business viability

- Cash flow that can comfortably cover loan payments

- A debt-to-income ratio that makes sense for your industry

Think of these requirements as your business's vital signs. Strong vitals make lenders comfortable. And here's a pro tip we've learned from thousands of appraisals: well-documented equipment value can sometimes help offset weaker financials.

Time In Business Considerations

I'll be straight with you – age matters in business lending. But it's not as simple as "older is better."

We see it all the time: a two-year-old company with solid financials and well-maintained equipment can often secure better terms than a ten-year-old operation with spotty records and aging machinery.

Here's what really counts:

- Your industry track record

- Equipment management history

- Growth trajectory

- Market positioning

Even if you're relatively new, don't count yourself out. Some lenders specialize in financing newer businesses. The key is matching your business profile with the right lending partner.

The Role of Equipment Appraisals in Financing

Why Equipment Appraisals Matter

Let's be direct about something we've learned from decades of equipment valuation: an accurate appraisal isn't just paperwork – it's your strongest negotiating tool. It's a professional assessment of your equipment's fair market value, and it directly influences two critical factors: the loan amount you can receive and the loan-to-value ratio (LTV) that lenders offer.

Think of it this way: When you're looking to finance that used Caterpillar bulldozer, an expert appraisal considers everything from hours of operation to maintenance history and current market demand. We've seen proper appraisals help operators secure financing at rates they didn't think possible, while inaccurate valuations left money on the table or resulted in unfavorable terms.

How Appraisals Affect Loan Terms

Here's something we've witnessed countless times in the field: the difference between a good equipment loan and a great one often comes down to your appraisal. Let me break down exactly how this plays out in real-world financing scenarios.

Picture this: You're looking at that used John Deere combine valued at $250,000 instead of the $200,000 you initially estimated. That $50,000 difference isn't just a number – it's leverage. We've seen this higher valuation translate into:

- Larger available loan amounts

- More competitive interest rates

- Reduced down payment requirements

But here's where it gets interesting: when appraisal values come in lower than expected, you're not just looking at a smaller loan amount. You might face higher down payments or less favorable terms because lenders use these appraisals to gauge their risk. Higher values mean lower risk for them, which translates to better terms for you.

The Equipment Appraisal Process

Let's pull back the curtain on what makes an appraisal truly valuable in the financing process. Every day, we're in the field conducting physical inspections, reviewing maintenance records, and assessing market values. But it's not just about kicking tires – it's about building a comprehensive value story that lenders trust.

A professional equipment appraisal considers:

- Equipment age and condition

- Brand reputation and reliability

- Usage patterns and hour meters

- Maintenance history and documentation

- Current market demand

- Recent modifications or upgrades

Here's what separates a basic valuation from one that actually drives financing success: certification. When you work with a certified equipment appraiser, you're getting more than just a number. You're getting an objective, defensible valuation that follows standardized procedures from organizations like the American Society of Appraisers (ASA).

Take that piece of construction equipment you're eyeing. A certified appraiser doesn't just look at its current condition – they use specific methodologies to determine its remaining useful life, which directly impacts both its appraised value and how lenders view it as collateral. This is where technical expertise meets strategic value: the right appraisal gives you the leverage you need in financing negotiations.

Steps To Apply For An Equipment Loan

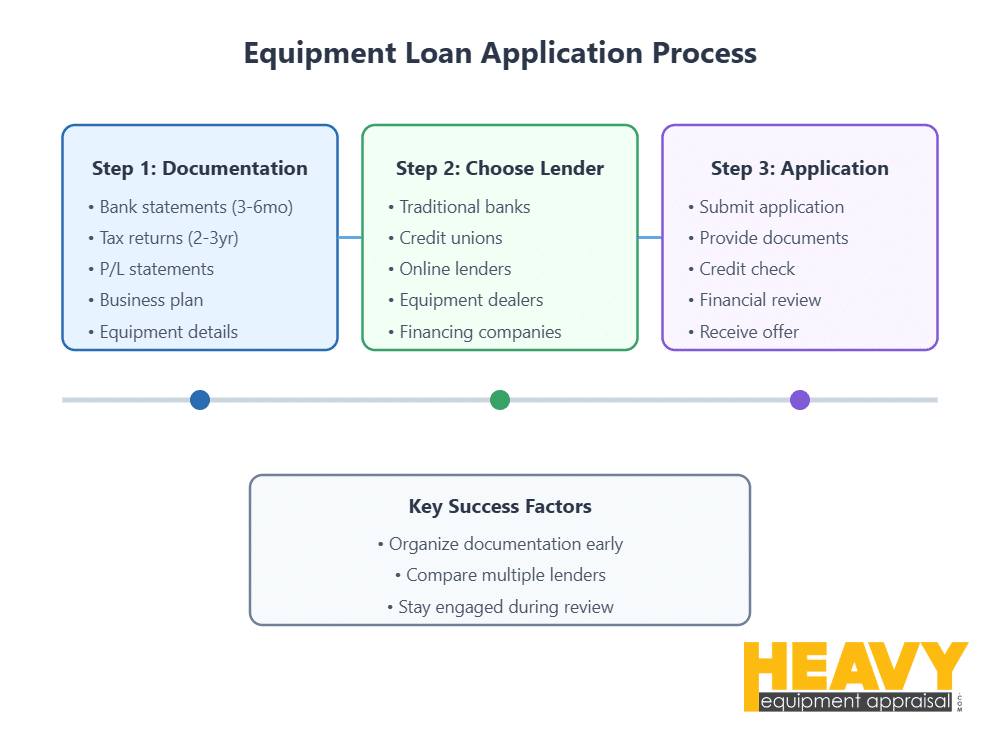

Gather Necessary Documentation

Let's build your loan application arsenal. Based on our experience facilitating equipment financing, here's what you need to have ready:

- Last 3-6 months of business bank statements (showing healthy cash flow)

- Previous 2-3 years of tax returns (demonstrating financial stability)

- Current year P&L statements (proving ongoing profitability)

- Your business plan (especially important for newer operations)

- Detailed equipment specifications (make, model, condition)

- Personal financial statements (if required)

Pro tip: Having detailed equipment documentation ready – including maintenance records and usage logs – can significantly strengthen your application. We've seen this level of preparation make the difference in borderline cases.

Choosing The Right Lender

Let me share something I've learned after two decades in equipment valuation: the right lender isn't always the one with the lowest rate.

Think of choosing a lender like choosing a strategic partner. Each brings their own playbook to the table:

Traditional Banks

You know them. They know you. But here's what most guides won't tell you: while banks offer competitive rates for established businesses, they often struggle with specialized equipment valuations. We've seen perfectly good deals fall apart because a traditional bank couldn't properly assess the value of industry-specific machinery.

Credit Unions

Here's an interesting trend we're seeing: credit unions are becoming increasingly sophisticated in equipment lending. They're often more willing to consider the full context of your business, not just the numbers. Plus, their community focus means they might better understand your local market dynamics.

Online Lenders

Speed demons of the lending world. Their tech-forward approach means faster decisions, but don't let the quick process fool you – you'll need to be just as prepared with documentation. They're particularly good for:

- Newer businesses with limited credit history

- Situations requiring quick turnaround

- Operators with less-than-perfect credit scores

Equipment Dealers

Want to know a secret? Sometimes the best financing comes from folks who know your equipment inside and out. Dealer financing can offer:

- Streamlined purchase process

- Better terms on specific brands

- More flexible maintenance agreements

But watch those interest rates – they're not always competitive.

Independent Financing Companies

The specialists of equipment lending. They often understand niche equipment better than traditional lenders, which can translate into more accurate valuations and better terms.

Complete The Application Process

After helping countless operators through this process, here's what I know works:

Step 1: Initial Application

Don't just fill out forms – tell your business's story. Include:

- Detailed equipment specifications

- Usage projections

- Revenue potential from the new equipment

- Market opportunity analysis

Pro tip: Remember that equipment appraisal we talked about earlier? This is where it becomes your secret weapon.

Step 2: Documentation Deep Dive

Here's where most applications live or die. Get methodical:

- Financial statements? Check.

- Tax returns? Ready.

- Bank statements? Organized.

- Equipment specs and appraisals? Front and center.

Step 3: Underwriting Process

This is where patience pays off. During underwriting, lenders will:

- Review your credit history

- Analyze business financials

- Assess equipment values

- Calculate risk metrics

Here's something most people miss: stay engaged during underwriting. Be ready to provide additional context about your business model or equipment usage patterns. We've seen this level of engagement turn initial rejections into approvals.

Step 4: Offer and Negotiation

This is where all your preparation pays dividends. With a proper equipment appraisal and solid documentation, you're negotiating from a position of strength.

Remember: your first offer isn't always your best offer. We've seen terms improve dramatically when operators could demonstrate deep understanding of their equipment's value and market position.

Tips To Improve Your Chances Of Approval

Boost Your Credit Score

Let's talk about credit scores for a minute.

You know what's funny? After two decades in equipment valuation, I've watched countless operators obsess over their credit scores while overlooking something far more valuable – their equipment's documented market value.

Don't get me wrong. Credit matters. But here's the real deal:

"I've seen operators with 650 scores get better terms than those with 750s," one of our veteran appraisers told me last week. "The difference? Rock-solid equipment documentation and smart preparation."

Still, let's optimize what we can:

- Pay everything on time. Basic? Yes. Critical? Absolutely.

- Keep those credit card balances low. Think 30% or less of your limits.

- Check your credit report like you check your equipment – regularly and thoroughly.

- Hold off on that new credit card application until after your equipment loan closes.

Strengthen Your Business Financials

Time for some straight talk about business financials.

Picture your financial statements as your business's maintenance log. Just like you wouldn't run a machine without proper maintenance records, you can't expect premium financing without clean, organized financials.

Here's your financial tune-up checklist:

Revenue Growth

Remember that construction company we worked with last quarter? They boosted their approval odds by documenting how each previous equipment purchase led to specific revenue increases. Smart.

Cost Management

It's not just about cutting costs. It's about showing strategic cost management. One client saved their application by documenting how their higher maintenance costs actually extended equipment life and reduced long-term expenses.

Cash Flow Optimization

Here's something most guides won't tell you: lenders love seeing seasonal cash flow variations that match your industry patterns. It shows you understand your business cycle.

Debt Management

Think of your debt-to-income ratio like your equipment's load capacity – there's an optimal range for peak performance.

Consider A Larger Down Payment

Let me share something I've seen work time and time again:

A larger down payment isn't just about reducing your loan amount. It's about demonstrating skin in the game. We recently had a client who turned a likely rejection into an approval by offering a 30% down payment instead of the standard 20%.

But here's the strategic play: before increasing your down payment, get an updated equipment appraisal. We've seen proper valuations reduce down payment requirements by showing lenders the true collateral value they're working with.

Think about it this way: every dollar you put down is a dollar you're investing in better terms. It's like preventive maintenance – a little extra upfront can save you significantly over time.

Pro tip: If you're considering a larger down payment, run the numbers both ways. Sometimes that capital might be better used for business expansion or maintaining cash reserves. It's about finding the sweet spot between equity and opportunity cost.

Understanding Loan Terms And Conditions

Interest Rates And APR

You know what keeps me up at night?

Not the interest rate on equipment loans. It's watching operators fixate on interest rates while missing the bigger picture.

Here's a truth bomb from the trenches: Interest rate is just one piece of your financing puzzle. APR (Annual Percentage Rate) tells the real story.

Think of it this way: Interest rate is like your equipment's list price. APR? That's your total cost of ownership, including maintenance and operating costs.

Let me share something I saw last month: An operator jumped at a 5% interest rate, ignoring the loan's 7.5% APR. Those origination fees and closing costs? They added up to more than what they'd have paid with a "higher" 6% interest rate but lower overall APR.

Pro tip: When comparing loans, line up the APRs side by side. It's like comparing equipment specs – you need the full picture to make an informed decision.

Repayment Terms

Ready for some strategic thinking about repayment terms?

Longer terms mean lower monthly payments. Shorter terms mean less total cost. But here's what really matters: matching your payment structure to your revenue patterns.

Consider this real-world scenario: A logging company we worked with opted for a 60-month term instead of 36 months. Why? Their equipment generated revenue on a seasonal basis. The longer term meant lower monthly payments they could handle during slow seasons.

Here's how to think about term length:

- Stable cash flow? Consider shorter terms to reduce total cost

- Variable income? Longer terms might provide needed flexibility

- Growing business? Match terms to your expansion timeline

- Seasonal operation? Align payments with your high-revenue periods

Collateral Requirements

Let's get real about collateral for a minute.

In equipment financing, your iron is usually your insurance policy. But here's something most guides won't tell you: how you document that collateral can be as important as the collateral itself.

Picture this: Two operators, same excavator model, same loan application. One gets premium terms, the other doesn't. The difference? A comprehensive equipment appraisal that demonstrated not just current value, but future market potential.

Smart collateral strategy includes:

- Professional equipment appraisals

- Detailed maintenance records

- Market value documentation

- Usage history and projections

- Condition assessments

Remember: In equipment financing, collateral isn't just about securing the loan – it's about optimizing your terms.

Here's a secret from the field: Some operators bring additional collateral to the table voluntarily. Not because they have to, but because it helps them negotiate better terms. It's like bringing extra insurance to the job site – sometimes it's worth it for the peace of mind and better contract terms.

Think of your equipment portfolio like a strategic asset. We've seen operators leverage older, fully-paid equipment as additional collateral to secure better terms on new financing. It's not about needing more security – it's about using your assets strategically.

Alternative Financing Options

Equipment Leasing

Remember the first time you rented a piece of equipment instead of buying it? That moment when you realized flexibility could be more valuable than ownership?

That's equipment leasing in a nutshell.

I used to be firmly in the "ownership or nothing" camp. Then I watched a clever operator use leasing to outmaneuver his competition during a market downturn. While others were stuck with aging equipment and hefty payments, he could adapt his fleet to changing market demands.

Here's what makes leasing worth a serious look:

- Keep your iron current without major capital outlays

- Maintain flexibility in a shifting market

- Turn those lease payments into tax deductions

- Free up working capital for growth opportunities

Consider that high-tech printer example we mentioned earlier. In tech-heavy equipment, leasing lets you stay current without getting locked into obsolete machinery. One of our clients in digital fabrication saved thousands by leasing rather than buying equipment that became outdated within three years.

SBA Loans For Equipment

Let me tell you about the hidden gem in equipment financing: SBA loans for equipment.

They're like that versatile piece of equipment in your fleet – not always the fastest option, but incredibly reliable when you need it.

Here's what makes them special:

- Lower down payments than conventional loans

- Longer repayment terms (think marathon, not sprint)

- Competitive interest rates backed by Uncle Sam

- More flexibility in qualification requirements

But let's be real – they're not for everyone. The application process can feel like rebuilding an engine. Detailed, time-consuming, but worth it if you're looking for optimal performance.

Pro tip: We've seen operators successfully use SBA loans to finance entire equipment fleets by bundling multiple purchases into one application. Strategic thinking at its finest.

Working Capital Loans

Think of working capital loans as your operational fuel tank.

They're not specifically for equipment, but they can be your ace in the hole when you need:

- Quick funding for smaller equipment purchases

- Bridge financing until long-term funding comes through

- Flexibility in how you use the funds

- Fast deployment for time-sensitive opportunities

Here's a strategy we saw work beautifully last quarter: An operator used a working capital loan for the down payment on a larger equipment loan. Unorthodox? Maybe. Effective? Absolutely.

But remember – these loans typically come with:

- Higher interest rates than traditional equipment loans

- Shorter repayment terms

- More frequent payment schedules

- Less focus on collateral value

They're like high-performance fuel – more expensive, but sometimes exactly what you need for that extra boost.

Pro tip: We've seen savvy operators use working capital loans strategically during their high season, when the increased revenue easily offsets the higher interest rates. It's all about timing and cash flow management.

Managing Your Equipment Loan

Making Timely Payments

You wouldn't run your equipment without a maintenance schedule. Your loan payments deserve the same disciplined approach.

I used to think loan management was just about making payments on time. Then I watched a savvy operator turn their payment history into leverage for future financing. Mind blown.

Here's what the pros do:

- Set up automatic payments (because even the best operators can forget)

- Build a 30-day payment buffer (think of it as your financial emergency kit)

- Keep detailed payment records (they're like your maintenance logs, but for money)

- Monitor your account for any hiccups (prevention beats cure, every time)

One operator I work with treats his payment schedule like his PM schedule - it's not just about keeping things running, it's about optimizing performance.

Tax Implications

Let's talk about everyone's favorite topic. (Just kidding. But stick with me here.)

Equipment financing comes with some serious tax advantages. Miss them, and it's like leaving money on the table. Or worse - letting your competition grab it.

Here's what you need to know:

Interest Deductions:

- Every dollar of interest paid is potentially deductible

- Keep those payment records organized (your accountant will thank you)

- Track any loan-related fees (they might be deductible too)

Equipment Depreciation:

- Section 179 is your friend (think of it as a tax-saving superpower)

- You might be able to deduct the full purchase price in year one

- Depreciation strategies can significantly impact your tax liability

Pro tip: We recently saw an operator save enough on taxes through proper depreciation planning to fund their next equipment purchase. Strategic thinking at its finest.

When To Refinance

Picture this: You're running a machine that's still getting the job done, but you know there's a more efficient model out there. That's basically what refinancing is about - optimizing your loan's performance.

Here's when to consider refinancing:

- Interest rates have dropped significantly

- Your credit score has improved

- You need to adjust your payment structure

- You've built up substantial equity in your equipment

But remember - refinancing isn't always the answer. Just like you wouldn't replace a perfectly good machine just because a newer model exists, sometimes sticking with your current loan makes more sense.

Real talk: Last month, I advised against refinancing for a client despite lower available rates. Why? The transaction costs would have eaten up the savings. Sometimes the best strategy is staying the course.

Want to know if refinancing makes sense? Run these numbers:

- Total cost of the new loan (including fees)

- Net savings over the loan term

- Break-even timeline

- Impact on monthly cash flow

Pro tip: Use your equipment's current appraised value as leverage in refinancing negotiations. Strong collateral value can help you secure better terms, even if other factors haven't changed much.

Conclusion: Securing The Right Equipment Loan For Your Business

Equipment financing isn't just about getting approved – it's about leveraging your assets to secure terms that fuel growth.

Success comes down to four key elements:

- Professional equipment appraisals that give you negotiating power

- Strategic documentation that tells your business story

- Smart timing that aligns with market conditions

- The right lender relationship for your business model

Think of equipment financing as building your operational foundation. Each element – from valuation to final terms – should align with your growth strategy. We've watched countless operators transform good deals into great ones by understanding how equipment value drives lending decisions.

Ready to put your equipment value to work? Contact us for a professional appraisal. It's your first step toward financing that doesn't just fund equipment – it fuels opportunity.