Heavy Equipment Line of Credit (ELOC): How It Works

Your equipment fleet is worth more than banks think. We’ve seen expert appraisals unlock credit lines 40% above standard offers, turning idle iron into financial leverage. A heavy equipment line of credit (ELOC) lets you tap this value on your terms—borrow only what you need, when you need it.

Let’s show you how to unlock your fleet’s true borrowing power.

Understanding Heavy Equipment Lines of Credit

What Is a Heavy Equipment Line of Credit?

A heavy equipment line of credit isn't just another financing option—it's a powerful tool that provides access to a revolving credit account specifically for purchasing heavy equipment. Unlike a traditional loan where you're paying interest on the full amount from day one, you only pay interest on what you actually borrow against your credit limit.

Construction equipment financing is surging:

New business volume jumped to 16.5% of all equipment financing in 2023, up from 15.4% in 2022 (ELFA Survey 2024). In raw numbers, that's billions in additional financing flowing into construction—a clear signal that flexible funding options like lines of credit are becoming essential growth tools in the industry.

We've seen this flexibility become a game-changer for businesses with varying equipment needs. Take one of our clients in earthmoving: they used their line of credit to purchase a bulldozer for a major project, then repaid the funds once the project started generating revenue. This kind of strategic equipment acquisition keeps working capital exactly where you need it.

How Does a Line of Credit Work?

A line of credit operates as your equipment acquisition arsenal, allowing you to borrow and repay funds as needed, up to your pre-approved credit limit. Picture it as a dynamic financial tool: draw funds to purchase equipment, repay the borrowed amount, and maintain the flexibility to borrow again within your credit limit and draw period.

The mechanics are straightforward but powerful:

- The draw period is your window of opportunity for accessing funds

- The repayment period defines your timeline for settling borrowed amounts

- Interest rates and fees apply only to your outstanding balance

Through thousands of appraisals, we've seen how this revolving nature provides businesses with the agility to respond to market opportunities. It's like having a strategic reserve you can deploy precisely when needed to expand or upgrade your fleet.

The Role of Equipment Appraisals in Financing

How Appraisals Impact Credit Limits and Terms

Let's talk about the hidden MVP of equipment financing: the appraisal.

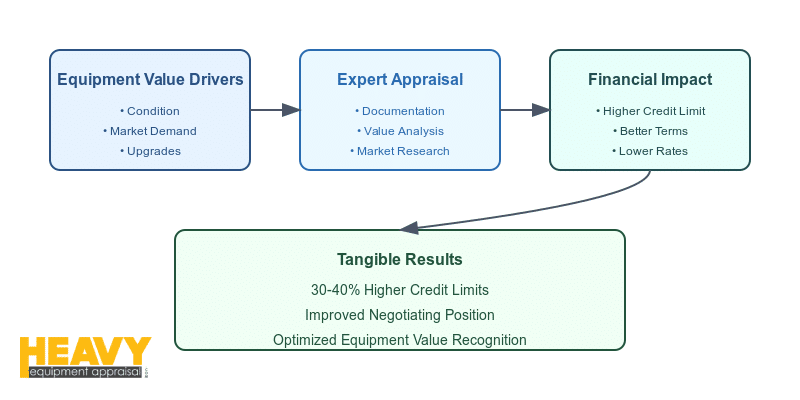

In our two decades of equipment valuation, we've seen firsthand how equipment appraisals can make or break a financing deal. Think of your equipment's appraised value as your financial foundation—it directly influences the credit limit a lender will offer.

Here's where it gets interesting: a higher appraised value doesn't just look good on paper; it demonstrates to lenders that your equipment is a rock-solid investment. We've seen this unlock higher credit limits and terms that can transform a decent deal into a game-changing opportunity.

Every day, we watch lenders pore over appraisal reports to assess both equipment value and lending risk. Pretty heady stuff, but here's what really matters: these reports need to capture not just the nuts and bolts of equipment condition but also the broader market trends that influence value.

Take this recent example: We appraised a used excavator for a client in Texas. On paper, it was just another piece of yellow iron. But our deep-dive revealed excellent maintenance records and high regional demand—factors that helped secure a credit limit 30% above what they initially expected.

The Importance of Accurate Appraisals

Here's a truth bomb from the trenches of equipment valuation: precision isn't just nice to have—it's your secret weapon for maximizing financing options.

We've seen it countless times: an inaccurate appraisal can kneecap your credit limit or saddle you with less favorable terms, potentially leaving that perfect piece of equipment just out of reach. It's like trying to build a skyscraper on a shaky foundation—technically possible, but why take the risk?

This is where deep expertise makes all the difference (and no, we're not just saying that because we're equipment nerds). An independent and certified appraiser brings something crucial to the table: an unbiased assessment of your equipment's value that gives you serious negotiating muscle with lenders.

Quick story: Last month, a client came to us after a lender undervalued their specialized material handling equipment. The lender's generalist approach missed key value drivers—custom attachments, recent upgrades, and strong regional demand. Our comprehensive appraisal captured these elements, leading to a valuation that better reflected the equipment's true worth in today's market.

The takeaway? In the world of equipment financing, precision creates opportunity. A professional appraisal ensures every value-driving factor gets its due, from basic specs to those market sweet spots that generalists often miss.

Benefits of Using a Line of Credit for Heavy Equipment

Flexibility In Equipment Purchases

Let's talk about something we see every day in equipment financing: the power of flexibility.

A heavy equipment line of credit isn't just another financing tool in your arsenal—it's your secret weapon for strategic growth. Here's why: instead of being locked into a fixed loan amount, you can draw funds as needed, adapting to market opportunities like a pro.

Think of it as your equipment acquisition Swiss Army knife. Need a skid steer for a surprise contract? Draw the funds. Project completed ahead of schedule? Pay it back early. This flexibility is particularly valuable for businesses riding the seasonal waves of construction, agriculture, or landscaping.

Real talk from the field: Last quarter, we worked with a landscaping company that needed to quickly expand their fleet for a major municipal contract. Instead of taking out a hefty loan, they used their line of credit to purchase a new skid steer loader. The kicker? They could time their equipment acquisition perfectly with their project timeline, then repay the funds as revenue started flowing.

That's the kind of strategic agility that makes all the difference in today's market.

Improved Cash Flow Management

Here's where things get interesting (yes, even in equipment finance).

The beauty of a line of credit lies in its precision: you only pay interest on what you actually borrow. It's like having a financial sniper rifle instead of a blunderbuss—you hit exactly what you're aiming for, with minimal spread.

Let's break it down with some real numbers we've seen in action:

- Traditional loan for $100,000? You're paying interest on the full amount from day one

- Line of credit with $100,000 limit? Draw $50,000 for that critical piece of equipment, and you're only paying interest on the $50,000

The math isn't just theoretical—we've watched businesses transform their cash flow management using this approach. One of our clients in earthmoving saved over $12,000 in interest payments last year by using a line of credit instead of a traditional loan for their equipment purchases.

This level of control over your borrowing costs isn't just about saving money (though that's nice). It's about having the financial flexibility to:

- Respond quickly to market opportunities

- Manage seasonal fluctuations

- Keep your working capital exactly where you need it

In the equipment-intensive industries we serve, from construction to agriculture, this kind of precise financial control can mean the difference between good growth and explosive growth.

Qualifying For a Heavy Equipment Line of Credit

Credit Score And Business History Requirements

Let's cut straight to the chase: getting a heavy equipment line of credit isn't just about having a nice fleet—it's about proving you're a solid bet.

Through thousands of equipment valuations, we've watched the qualification dance from front-row seats. Lenders scrutinize your applicant credit score and business age like seasoned equipment inspectors examining a used excavator. They're looking for signs of reliability and longevity.

Here's the straight talk on what typically moves the needle:

- Credit score target: 680 or higher (though we've seen flexibility here)

- Business history: Two years plus in operation

- A track record that shows you know your way around heavy iron

But here's something interesting we've noticed: these aren't always hard-and-fast rules. Some lenders will work with businesses that don't quite hit these marks, especially when they've got other strengths in their corner. They might charge higher interest rates or want additional collateral, but the door isn't automatically closed.

Financial Documentation Needed

Now, let's talk paperwork—yes, it's everyone's favorite topic (insert eye roll here).

But stick with me, because this is where many businesses leave money on the table. Lenders need to see more than just a handshake and a promise. They want:

- Tax returns (clean and organized)

- Bank statements (showing healthy cash flow)

- Financial projections (realistic, not just optimistic)

Here's what catches many off guard: lenders also dive deep into your annual revenue and debt-to-income ratio. Think of these numbers as your business's vital signs—they tell the story of your financial health.

Pro tip from the trenches: We've seen businesses dramatically improve their chances of securing a line of credit by getting their documentation house in order before they apply. It's like prepping equipment for an inspection—you want everything tuned up and ready to show.

The key here isn't just having the documents; it's about what they say about your business's ability to manage debt. Lenders love seeing:

- Consistent revenue streams

- Manageable debt levels

- Clear evidence of equipment expertise

- Strong project pipelines

Remember: thorough documentation isn't just busywork—it's your chance to demonstrate that you're as serious about financial management as you are about equipment operations.

Interest Rates And Fees

Equipment Credit Limit Calculator

Estimated Maximum Credit Limit:

*Estimate based on typical lender criteria. Actual limits may vary.

Factors Affecting Interest Rates

Let's dive into everyone's favorite topic: interest rates. (Just kidding—we know this isn't exactly Netflix material.)

But here's the thing: understanding interest rates on a heavy equipment line of credit is like reading the diagnostic codes on a piece of equipment. Once you know what you're looking at, patterns emerge that can save you serious money.

From our vantage point in the equipment valuation world, we've watched how multiple factors influence these rates:

- Market conditions (the big-picture economic stuff)

- Your applicant credit score (your financial report card)

- Business age (your industry track record)

- Debt-to-income ratio (your financial breathing room)

Think of your credit score as your business's credit GPS—the higher the number, the smoother the financing road ahead. Combine that with a healthy debt-to-income ratio, and you're positioning yourself for better rates.

Here's something interesting we've noticed in our appraisal work: the type of equipment you're financing can actually move the needle on your interest rate. Remember that used excavator we mentioned earlier? Because it was newer and maintained immaculately (and we documented this thoroughly in our appraisal), it qualified for a significantly better rate than older, less valuable equipment.

Common Fees Associated With Lines Of Credit

Now, let's talk about the fees that often hide in the financing shadows. (Don't worry—we're about to shine a light on all of them.)

In our experience working with equipment-intensive businesses, there are three main fees you'll encounter:

- Origination fees: Think of these as your line of credit's "startup costs"—typically a percentage of your total credit limit, charged when your line of credit is established.

- Annual fees: Your yearly membership dues to the credit club. They keep your line of credit active and available.

- Draw fees: The price of admission each time you tap into your line of credit.

Quick story from the field: Last month, a client nearly signed on with a lender offering a lower interest rate, until we helped them run the numbers on the fee structure. Turns out, the higher fees would have eaten up any interest savings within eight months.

Pro tip: When comparing financing options, look beyond the headline interest rate. We've seen cases where a slightly higher rate paired with lower fees actually saved businesses money in the long run.

Understanding these fees isn't just about avoiding surprises—it's about strategic planning for your total cost of borrowing. And yes, some lenders might throw in prepayment penalties or late payment fees, so read those terms like you'd read an equipment maintenance manual: thoroughly and with an eye for details.

Comparing Lines Of Credit To Other Financing Options

Let's clear the fog around equipment financing options. After appraising thousands of machines across every sector imaginable, we've seen what works—and what doesn't—in real-world situations.

Lines Of Credit Vs. Term Loans

When it comes to heavy equipment financing, you've got choices. Think of lines of credit and term loans as different tools in your financial toolbox—each designed for specific jobs.

Here's the real talk from the equipment trenches:

A term loan is your financial straightedge:

- Fixed loan amount

- Fixed interest rate

- Fixed repayment period

Meanwhile, a line of credit is more like your adjustable wrench:

- Revolving credit limit

- Variable interest rate

- Flexible repayment period

Through our work with equipment-intensive businesses, we've noticed something interesting: term loans shine when you need a specific amount for a planned purchase. Picture buying that new excavator you've been eyeing—you know the exact cost and have a solid repayment plan.

But lines of credit? They're your ace in the hole for businesses that need to pivot quickly. We've watched contractors use them to seize unexpected opportunities or manage seasonal demands without missing a beat.

Lines Of Credit Vs. Equipment Leasing

Now, let's throw equipment leasing into the mix.

Equipment leasing is like renting an apartment instead of buying a house. You get the use of the equipment without the commitment of ownership. The structure is straightforward:

- Fixed lease term

- Fixed monthly payment

- No ownership at the end (though some leases offer purchase options)

Here's where our equipment valuation expertise comes in handy: Leasing can look attractive upfront—lower initial costs, predictable payments. But we've done the long-term value calculations countless times. Unless you're in a highly specialized field where equipment becomes obsolete quickly, leasing often ends up being more expensive than purchasing equipment outright.

Let's break it down visually:

| Feature | Line of Credit | Term Loan | Equipment Leasing |

| Flexibility | High | Low | Low |

| Ownership | Yes | Yes | No |

| Repayment | Flexible | Fixed | Fixed |

| Interest | Variable | Fixed | Implicit in lease payments |

| Initial Cost | Lower | Higher | Lower |

| Long-Term Cost | Lower if managed well | Higher | Higher |

Pro tip from our appraisal experience: Don't just look at the monthly numbers. Consider residual value—it's like equity in your equipment. We've seen businesses build substantial fleet value through strategic purchasing, while their leasing competitors had nothing to show for years of payments.

Here's a real-world example that brings this home: Last year, we worked with a mid-sized construction company facing this exact decision. They were tempted by an attractive lease offer on a fleet of skid steers. But after we ran the numbers, including projected residual values (our specialty), they opted for a line of credit. Twelve months later, they've built equity in their equipment while maintaining the flexibility to adapt to market changes.

How To Apply For A Heavy Equipment Line Of Credit

Step-By-Step Application Process

Let's demystify the application process. After guiding countless clients through equipment valuations for financing, we've seen what makes applications shine—and what makes them sink.

First things first: gathering your documentation. Think of this like prepping equipment for a major inspection. You'll need:

- Financial statements (your business's health records)

- Business licenses (your operational credentials)

- Equipment appraisals (your value verification—and yes, this is where we come in)

Here's where many businesses hit their first speed bump: incomplete documentation. We've seen solid companies with great equipment get stalled in the application process simply because they weren't prepared for the paper chase.

Next up: submitting your application. This kicks off the lender's review of your application steps and required documents. They'll be checking your eligibility for that line of credit like a seasoned mechanic going over a used dozer—thoroughly and methodically.

Tips For A Successful Application

Now, here's where our years in the equipment valuation trenches really pay off. Want to stack the deck in your favor? Let's talk strategy.

First, about that equipment appraisal—it's not just another box to check. A professional appraisal is your secret weapon. We've seen it time and again: a solid appraisal that really digs into your equipment's value can be the difference between a good offer and a great one.

Think of it this way: your equipment's value is like your business's collateral credit score. The more accurately and professionally it's documented, the stronger your negotiating position becomes.

Quick story from last month: A client came to us frustrated after getting lowball credit offers. The problem? Their previous appraisal missed key value drivers in their fleet. Our comprehensive valuation captured everything from recent upgrades to market demand patterns. Result? They secured a credit line 40% higher than their best previous offer.

Pro tips from the field:

- Shop around: Different lenders have different appetites for equipment lending

- Be prepared for questions about:

- Your business growth plan

- Your equipment utilization patterns

- Your market positioning

- Have your seasonal revenue patterns documented

- Keep maintenance records handy (they matter more than you'd think)

Remember: This isn't just about getting approved—it's about getting the best possible terms. In our experience, preparation isn't just half the battle—it's the whole war.

Think of your application package as a business story, with your equipment value as a central character. The better you tell that story (backed by solid documentation and professional appraisals), the better your chances of securing terms that support your growth plans.

Conclusion: Is A Line Of Credit Right For Your Heavy Equipment Needs?

Equipment financing often feels like a maze of trade-offs between flexibility and terms. Our deep dive into equipment values across every major sector reveals a clear pattern: a heavy equipment line of credit, backed by expert appraisals, consistently outperforms traditional options for businesses with dynamic needs.

The math is compelling. You'll pay interest only on what you borrow while maintaining the agility to seize opportunities as they arise. We've watched businesses transform their growth trajectory simply by matching their financing structure to their operational rhythm.

Ready to unlock your equipment's true borrowing power? Start with a certified appraisal—it's your key to maximizing terms and optimizing your financing strategy.