7 Best Excavator Financing Options in 2025

Heavy iron doesn’t come cheap, and neither do the mistakes people make financing it. Every day, contractors are leaving money on the table by jumping into the wrong financing deal. The best excavator financing options include equipment loans, leases, and dealer financing.

Excavator financing allows businesses to purchase equipment through loans, leases, or equipment financing agreements. Loan terms typically range from 24 to 72 months with interest rates between 4% and 10%. Approval depends on credit score, business history, and equipment value.

Banks and credit unions offer loans with lower interest rates, while leasing provides lower monthly payments. Manufacturers like Caterpillar and Komatsu offer in-house financing with flexible terms.

| Best Overall 🏆 | Crest Capital |

| Best for Startups | SBA Loans |

| Best for Leasing | Caterpillar |

| Best for Bad Credit | Triton Capital |

| Most Flexible | Komatsu |

Excavator Types and Financing Options

Before we dive into the money talk, let’s make sure we’re speaking the same language about the different kinds of excavators you’re looking to put in your fleet.

Here’s what’s out there:

- Crawler Excavators: The workhorses of the industry. These track-mounted machines are what most folks picture when they think “excavator.” They’ll eat up rough terrain for breakfast and give you the stability you need when you’re digging deep.

- Wheeled Excavators: Think of these as the more mobile cousins of crawlers. They’re perfect when you need to move between jobsites without calling in a lowboy. They’ll zip around on pavement without tearing it up, though they’ll cost you a bit more upfront.

- Mini Excavators: Don’t let the name fool you – these compact performers can be worth their weight in gold when you’re working in tight spaces or doing precision work. They’re also typically easier on the wallet and simpler to finance.

Now, let’s talk about how to get one of these machines working for you without breaking the bank. Here are your main equipment loan options:

flowchart LR

Start[Business Need] --> Decision{How long do\nyou need it?}

Decision -->|Long Term| Own{Want to own?}

Decision -->|Short Term| Rental[Rental]

Own -->|Yes| Loan[Traditional Loan]

Own -->|Maybe| Lease[Lease Options]

Loan --> Features1[["• Full ownership\n• Higher payments\n• Tax advantages"]]

Lease --> Features2[["• Flexible terms\n• Lower payments\n• Upgrade options"]]

Rental --> Features3[["• No commitment\n• Highest per-month\n• Full maintenance"]]

style Start fill:#f9f9f9,stroke:#333,stroke-width:2px

style Decision fill:#e1f3f8,stroke:#333,stroke-width:2px

style Own fill:#e1f3f8,stroke:#333,stroke-width:2px

style Loan fill:#d4edda,stroke:#333,stroke-width:2px

style Lease fill:#d4edda,stroke:#333,stroke-width:2px

style Rental fill:#d4edda,stroke:#333,stroke-width:2pxTraditional Loans

Think of this as your classic equipment loan – you get the machine, make monthly payments (plus interest), and it’s yours when you’re done. The excavator itself serves as collateral, which usually means better rates than an unsecured loan.

Equipment Leases

This is essentially a long-term rental arrangement with benefits. You’ll make a down payment, followed by monthly payments, and at the end of the lease term, you’ve got options – return it, renew the lease, or buy it at market value. It’s worth noting that equipment leases can be more flexible than traditional loans.

Rental Programs

Need an excavator for a specific project or just testing the waters? Excavator rental might be your best bet. You get the machine without the long-term commitment, though you’ll pay a premium for that flexibility. Excavator rent-to-own programs could be an option.

Working Capital Loans

Here’s an interesting twist – if you’ve got equity in your existing equipment, you can leverage that to secure funding for other business needs. Think of it as making your current fleet work harder for you, whether you’re bidding on new projects or need to expand operations.

Eligibility Criteria for Excavator Financing

Let’s cut to the chase – what do lenders actually look at when you’re trying to finance that shiny new (or well-maintained used) excavator? Here’s the real deal on what matters and why.

The Credit Score Dance

Look, we all know credit scores aren’t the whole story, but they’re the first thing lenders check. Most want to see a minimum FICO of 640, though you’ll get better terms with higher scores. Here’s a pro tip: some lenders offer “soft credit checks” to pre-qualify you. Take advantage of this – it won’t ding your credit score, and you’ll know where you stand before making a full application.

Business Financials: The Story Behind the Numbers

Your financial statements are like your business’s report card. Lenders want to see:

- Income statements that show you can handle the payments

- Balance sheets that prove you’re not over-leveraged

- Cash flow statements that demonstrate you can keep the lights on while making payments

And here’s something they don’t always tell you: seasonal businesses should highlight their peak periods and explain their off-season strategy. Lenders get it – not every business has smooth, year-round income.

Time in Business: The Experience Factor

Let’s be real – the longer you’ve been pushing dirt, the more comfortable lenders feel. Established businesses generally have an easier time getting approved, but don’t let that discourage you if you’re newer to the game. Some lenders specialize in working with younger companies, especially if you can show solid contracts or project pipelines.

Down Payment: The Commitment Question

Here’s where it gets interesting. While some lenders advertise no-money-down deals (and yes, they do exist), putting more money down often gets you better terms. Think of it this way: the bigger your stake in the game, the more skin you have in it, and lenders like that. Plus, a larger down payment usually means lower monthly payments – something to consider when you’re mapping out your cash flow.

The Unwritten Rules

Beyond the official criteria, here are some things that can tip the scales in your favor:

- Industry experience (even if your business is new)

- Existing relationships with equipment dealers

- Strong references from suppliers or larger contractors

- A solid business plan that shows how the excavator fits into your growth strategy

Remember, these aren’t just boxes to check – they’re ways to show lenders you know what you’re doing and can be trusted with their money. The more of these bases you can cover, the better your chances of getting approved with terms that won’t keep you up at night.

Interest Rates and Fees

Let’s talk money – specifically, what it’s going to cost you to get that excavator working for you instead of sitting pretty in the dealer’s yard. And no, we’re not going to give you that “rates as low as…” nonsense without explaining what actually determines your rate.

The Four Horsemen of Interest Rates

Here’s what really moves the needle on your financing costs:

Type of Financing

Here’s something they don’t put in the brochures: loans typically come with higher interest rates than leases. Why? Because you’re buying the thing outright. That beautiful machine is going to be yours when all is said and done, and lenders price that ownership premium into the rate.

Lender Selection

Remember that old saying about shopping for boots? Same thing applies here. Different lenders, different appetites for risk, different rates. Some focus on perfect-credit customers and offer rates that’ll make you smile. Others specialize in helping folks with a few dings in their credit history – for a price, of course.

Your Financial Report Card

Let’s be real – the stronger your credit and financials look, the better your rate options. But here’s a pro tip: some lenders will work with you even if your credit’s seen better days, especially if you can show solid contracts or reliable cash flow.

Equipment Age and Condition

Want the best rates? Look at new iron. But don’t write off used equipment – plenty of lenders offer competitive rates on late-model used machines, especially if they’re coming from reputable dealers with documented maintenance histories.

The “Special Offer” Game

Speaking of rates, let’s talk about those too-good-to-be-true dealer specials. You know the ones:

- Volvo’s running 0% for 48 months on select models

- DEVELON (yeah, that’s what Doosan’s calling themselves now) is offering 1.49% for 60 months

- Other manufacturers are jumping in with similar promos

Are these deals legit? Absolutely. But remember – there’s usually a catch. Maybe it’s only on certain models, or you need tier-1 credit, or there’s a hefty down payment requirement. Still, if you qualify, these programs can save you serious cash.

The Real Cost of Financing

Here’s what your monthly payment ticket actually includes:

- Base interest rate (what everyone talks about)

- Any origination fees (what they mention in the fine print)

- Documentation fees (what they mumble about at closing)

- Insurance requirements (what they remember to mention after you’ve signed)

Pro tip: Ask about all fees upfront, and get them in writing. There’s nothing worse than thinking you’ve budgeted correctly only to get hit with “administrative fees” at closing.

Remember, the lowest rate isn’t always the best deal. Sometimes a slightly higher rate with lower fees or more flexible terms makes more sense for your operation. It’s about the total cost of financing, not just the number that goes on the sales flyer.

Repayment Terms

Let’s talk about the part that’ll show up in your checking account every month for the next few years. You know, the numbers that matter when you’re trying to sleep at night.

The Timeline Tango

Here’s the deal – most excavator financing runs anywhere from 24 to 72 months. That’s a pretty wide spread, right? Well, there’s a method to the madness:

- 24-36 months: You’ll feel those payments, but you’ll own that iron free and clear while it still has plenty of life left

- 48-60 months: The sweet spot for most contractors – payments won’t break the bank, and you’re not still paying for it when it’s ready for major repairs

- 72 months: Lowest monthly payments, but remember – you might be making payments on a machine that’s starting to show its age

Pro tip: Match your loan term to how long you actually plan to keep the machine. Nobody wants to be writing checks for an excavator they traded in two years ago.

The Monthly Payment Reality Check

Ever notice how dealers love to talk about the monthly payment but get squirrely when you ask about the total cost? Here’s why: longer terms mean lower monthly payments but higher total costs. It’s like that old country song – you get the girl, but you’re paying for it forever.

Let’s break it down with some straight talk:

- Short term = Higher monthly pain, lower total cost

- Long term = Easier monthly digest, but you’re feeding that loan a lot more dollars overall

The Flex Factor

Here’s something they don’t always advertise: seasonal payment options. Yeah, they exist, and they’re a game-changer if your work follows the seasons. We’re talking about:

- Skip payments during your slow months

- Lower payments in winter, higher in summer

- Quarterly “balloon” payments that match up with your big project payouts

Just remember – these flexible terms aren’t charity. The lender’s getting their money one way or another, but at least you can time it with your cash flow.

The Fine Print Festival

Before you sign anything, let’s talk about what should be keeping your attention:

- Early payoff penalties (yes, some lenders will actually punish you for being responsible)

- Payment due dates (and what happens if you’re a day late)

- Default triggers (because sometimes “default” doesn’t mean what you think it means)

- Insurance requirements (hint: they’re usually higher than what you’d pick on your own)

Online Calculators: Trust But Verify

Sure, every lender’s website has a payment calculator. They’re great for ballpark figures, but remember – they usually assume:

- You have perfect credit

- You’re buying new equipment

- You’re not asking for any payment flexibility

- You’re okay with their standard terms

Real world numbers? Usually add about 10-15% to whatever that calculator tells you. Not trying to be negative – just keeping it real.

Now that I’ve just crap-talked most equipment finance calculators…click the link to check ours out. 😎

Tax Implications

Alright, let’s talk about everyone’s favorite topic (said no one ever) – taxes. But stick with me here, because this is where you can actually save some serious cash on that iron you’re eyeing.

The Good News You Didn’t Know You Were Waiting For

First off, Uncle Sam actually wants you to buy heavy equipment. No, really. They’ve set up the tax code to reward businesses that invest in iron. Here’s the deal:

- Those interest payments you’re making? Tax-deductible. Every single penny.

- Depreciation? Oh, you’re going to like this part.

- Section 179? Think of it as the government’s way of saying “thanks for keeping America moving.”

Section 179: The Gift That Keeps On Giving

Let’s talk about Section 179 because if you’re not taking advantage of this, you’re leaving money on the table. For 2024, you can write off up to $1,160,000 of equipment costs. Yeah, you read that right – over a million bucks.

Here’s what that means in real money:

- Buy a $400,000 excavator

- Write off the full amount in year one

- Instead of spreading depreciation over 5+ years like your grandpa had to do

But remember – you need to actually put that machine to work before December 31st. Ordering it isn’t enough – it needs to be on your job site, moving dirt.

State-Level Plot Twists

Now, here’s where it gets interesting. Every state’s got their own take on equipment taxes:

- Some states love you so much they’ll exempt your equipment from sales tax

- Others have special rules for leases (looking at you, Texas)

- A few have personal property tax rules that’ll make your head spin

Pro tip: This is where a good tax advisor earns their keep. Not your cousin who “knows about taxes” – someone who actually speaks equipment financing for a living.

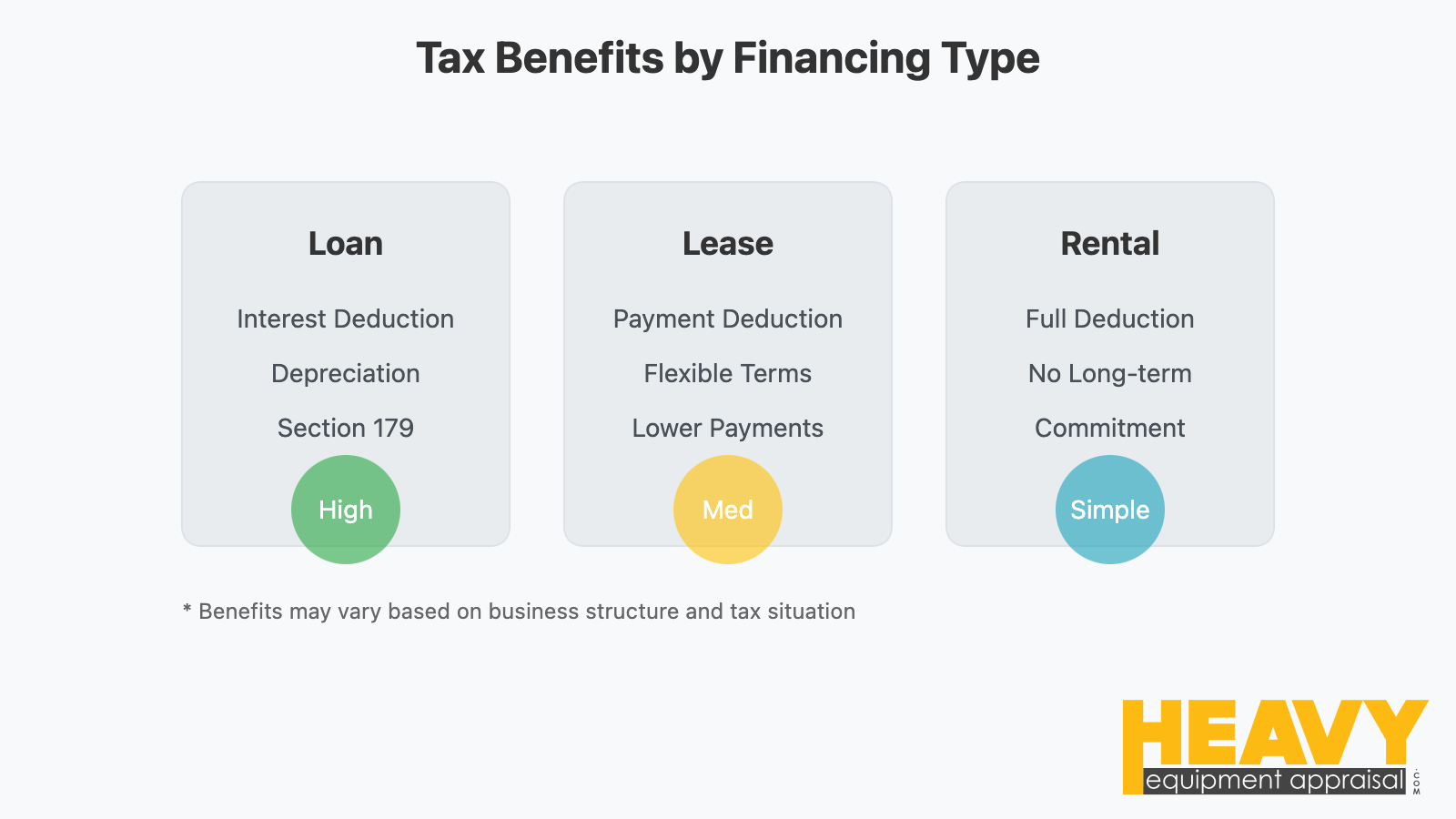

Lease vs. Buy: The Tax Edition

Remember how we talked about leasing versus buying? Well, there’s a tax angle here too:

- Purchasing: You get depreciation and interest deductions

- Leasing: The entire payment might be deductible as a business expense

- Either way: You’re reducing your tax bill, just through different doors

The Documentation Dance

Here’s something they don’t teach you in contractor school: Keep. Every. Paper.

- Purchase agreements? File it.

- Maintenance records? Keep ’em.

- Financing statements? You better believe it.

Why? Because if the IRS ever comes knocking (and let’s hope they don’t), you want to be the one with all the receipts.

The Fine Print Nobody Reads

And before you glaze over, here’s a nugget worth its weight in gold: timing matters. Buying in December versus January can make a huge difference in when you can take deductions. Sometimes waiting a few days can push your tax benefits into next year – which might be exactly what you want, or exactly what you don’t want.

Remember: This isn’t just about saving on taxes – it’s about using the tax code to help you afford better equipment. Because at the end of the day, the best iron is the iron you can afford to keep running.

Market Trends in Excavator Financing

Look, if you’ve been in this game for more than five minutes, you know the equipment financing market moves faster than a skid steer with a new operator. But here’s what’s actually happening on the ground in 2024, beyond the glossy brochure talk.

The Big Picture

First off, let’s talk numbers that matter: The construction equipment finance market is headed to $128.15 billion by 2033. That’s billion with a B, growing at 9.20% annually from 2028. But what’s driving this growth? Grab your coffee – this gets interesting.

The Great Reshoring Revolution

Remember when “Made in China” was on everything you touched? Well, the winds are shifting. Companies are bringing manufacturing back stateside faster than a wheeler can load a truck. Why does this matter to you? Because:

- More domestic manufacturing = More construction projects

- More projects = More demand for iron

- More demand = Better financing options (usually)

And here’s the kicker – banks are actually getting excited about funding equipment for these projects. When’s the last time you saw a banker excited about anything?

Equipment-as-a-Service: The New Kid on the Block

Yeah, it sounds like one of those fancy Silicon Valley terms, but stick with me here. EaaS is changing the game whether we like it or not. It’s like Netflix, but for excavators (sort of):

- Pay for what you use

- Always have access to newer models

- Someone else handles the maintenance headaches

Is it right for everyone? Heck no. But for some operations, especially smaller ones or those with variable workloads, it’s worth a hard look.

The Green Machine Movement

Look, whether you believe in climate change or think it’s all hot air, the money folks have made up their minds. Green financing is here to stay:

- Better rates for fuel-efficient machines

- Special programs for electric equipment

- Extra points if you’re working on sustainable projects

And manufacturers aren’t just painting their machines green – they’re actually building stuff that uses less fuel while getting more done. Your wallet might end up thanking the tree-huggers.

Digital Financing: Welcome to 2025

Remember when getting equipment financing meant a three-hour meeting with a guy in a bad tie? Those days are going the way of the manual transmission:

- Online applications that don’t require a PhD

- Digital documents you can sign from your phone

- Automated underwriting that doesn’t take three weeks

Sure, you can still do it the old-school way if that’s your thing. But when you can get approved while sitting in your excavator between jobs, why would you?

What This Means for Your Bottom Line

Here’s how these trends translate to dollars and sense:

- More competition among lenders = Better terms for you

- Greener equipment = Lower operating costs

- Digital processing = Faster approvals

- Flexible options = Better cash flow management

The smart money? It’s on being flexible. The market’s changing faster than dealer coffee gets cold, and the winners are going to be the ones who adapt while keeping their eyes on the fundamentals.

Used Excavator Financing

Let’s talk about the elephant in the equipment yard – used excavators. You know, the ones with a few scratches, a couple thousand hours on the meter, and a price tag that doesn’t make your accountant break out in hives.

The Used Equipment Reality Check

Here’s something the dealer’s shiny new machine brochure won’t tell you: a well-maintained used excavator can be worth its weight in gold. We’re talking about machines that:

- Have worked out all their factory quirks

- Come with a known performance history

- Cost substantially less than their showroom-fresh cousins

- Still have plenty of life left in them

And here’s the best part – you can finance these veterans just like you would a new machine. Different terms? Sure. Impossible to get approved? Not even close.

Finding the Sweet Spot

Want to know where the smart money is playing in the used market? Look for:

- Machines with 2,000-4,000 hours (broken in but not broken down)

- Major brand names (Cat, Komatsu, Volvo – you know the usual suspects)

- Documented maintenance history (bonus points if it’s been dealer-serviced)

- One or two previous owners (fewer owners usually means fewer headaches)

The Money Talk

Let’s get real about financing these pre-loved dirt movers:

- Down payments might be a bit higher (banks like insurance)

- Terms might be shorter (nobody wants you paying for a paperweight)

- Interest rates could be a point or two above new equipment

- But your total investment will still be way below new sticker price

Pro tip: Some dealers’ CPO (Certified Pre-Owned) programs come with special financing rates that’ll make you wonder why anyone buys new.

The Pre-Purchase Tango

Before you sign anything, here’s your used excavator checklist:

- Get that hour meter verified (hour meter fraud is still a thing)

- Check the undercarriage (it’s usually your biggest future expense)

- Pull the maintenance records (or lack thereof)

- Run the serial number (theft is rare but expensive)

- Get an independent inspection (best few hundred bucks you’ll ever spend)

The Fine Art of Timing

Here’s an insider secret: the best time to buy used isn’t when you need it – it’s when everyone else doesn’t. Think:

- End of fiscal quarters (when dealers need to hit numbers)

- Winter months (when work slows in northern states)

- Right after new model releases (when trade-ins flood the market)

Making the Numbers Work

Remember this: a used machine that makes you money is better than a new one that keeps you up at night. When you’re running the numbers:

- Factor in immediate maintenance needs

- Budget for upcoming major service intervals

- Consider the machine’s remaining useful life

- Calculate your real hourly operating cost

Don’t let the lower sticker price fool you – used equipment needs a buffer in your budget for the unexpected. But play it smart, and you’ll end up with a reliable money-maker that paid for itself while the new machine buyers are still writing checks to the bank.

Technological Advancements and Excavator Financing

Remember when an excavator was just an excavator? These days, they’re rolling out of the factory with more computing power than the stuff that put astronauts on the moon. Let’s talk about what that means for your wallet – and your financing options.

The Tech Revolution Nobody Asked For (But Everyone’s Buying)

Look, technology is doing to excavators what smartphones did to flip phones. We’re talking:

- GPS grade control that makes your best operator even better

- Telematics that tell you everything except what your operator had for lunch

- Electric and hybrid options that make the EPA happy

- Automation features that have old-timers shaking their heads

And here’s the kicker – this stuff isn’t just fancy bells and whistles anymore. It’s becoming standard equipment faster than you can say “increased productivity.”

The Price Tag Reality

Let’s address the elephant in the equipment yard: all this tech ain’t cheap. A machine that would’ve cost you $300K five years ago? Now it’s pushing $400K or more with all the goodies. But here’s where it gets interesting:

- Lenders actually like these higher-tech machines

- They hold their value better

- They’re more productive (when used right)

- They’re easier to track and monitor

Translation? You might get better financing terms on a tech-heavy machine than on its “dumber” cousin.

The Skills Gap Nobody Wants to Talk About

Here’s the dirty little secret about all this technology: somebody’s got to know how to use it. And fix it. And that somebody needs to be paid accordingly. When you’re planning your financing, you need to factor in:

- Training costs for operators

- Software updates (yeah, that’s a thing now)

- Specialized maintenance personnel

- Potential downtime when something goes sideways

Making the Numbers Work

Before you sign up for that fully-loaded digital dirt mover, consider this:

- Will the productivity gains offset the higher payments?

- Do you have the infrastructure to support it?

- Can you charge enough to justify the investment?

- Are your operators ready for the transition?

Sometimes the base model with a few key upgrades makes more sense than the full-package machine that nobody knows how to use.

The Future Is Coming Whether You Like It or Not

Here’s what’s rolling down the pike:

- More autonomous features

- Better integration with project management software

- Enhanced safety systems

- Improved fuel efficiency (or no fuel at all)

And here’s what that means for financing:

- Shorter terms (technology moves fast)

- More flexible upgrade options

- New insurance requirements

- Different residual value calculations

The Smart Money Play

Want to stay ahead of the curve without betting the farm? Consider:

- Phasing in new technology gradually

- Looking for machines with upgradeable systems

- Negotiating training packages as part of the purchase

- Building tech adoption costs into your financing plan

Because at the end of the day, the goal isn’t to have the fanciest machine in the county – it’s to have equipment that makes you money while letting you sleep at night.

Economic Impact on Excavator Financing

Let’s talk about the elephant in the boardroom – how the broader economy is messing with your equipment financing options. And boy, has it been a wild ride lately.

The Inflation Situation

Remember when a quarter-million dollars bought you a decent excavator with all the bells and whistles? Yeah, those days are gone like $2 diesel. These days, inflation’s doing to equipment prices what a rookie operator does to grade stakes – making everything higher than it should be.

What this means for your wallet:

- Higher sticker prices on new iron

- Used equipment values through the roof

- Financing costs that’ll make your accountant sweat

- Parts and maintenance costs that keep climbing

The Interest Rate Tango

The Fed’s been busier than a rental fleet during construction season, and those rate hikes? They’re hitting equipment financing harder than a hammer on a stuck pin:

- Variable rates are bouncing around like a skid steer on washboard

- Fixed rates are higher than we’ve seen in years

- Lenders are getting pickier about who they’ll dance with

- Terms are shorter than a summer workday in Alaska

But here’s the thing – the equipment financing sector isn’t just taking it lying down. It’s actually showing more resilience than a Cat undercarriage.

The Silver Linings Playbook

Despite all this economic drama, there are some bright spots:

- Reshoring is driving demand for heavy equipment

- Infrastructure projects are still rolling

- Tech advances are making machines more productive

- Smart operators are finding ways to make it work

Making It Work in the Real World

So how do you play this hand? Here’s what the smart money’s doing:

- Locking in fixed rates while they can

- Looking harder at lease options

- Getting creative with payment structures

- Keeping their powder dry for strategic purchases

The Long Game

Remember folks – this isn’t our first rodeo with economic turbulence. The equipment financing market’s been through:

- The 2008 crash (yeah, that was fun)

- The pandemic chaos

- Supply chain nightmares

- More “once in a lifetime” events than we care to count

And guess what? The industry’s still here, still moving dirt, still making it happen.

What This Means for You

If you’re in the market for financing right now:

- Don’t panic-buy (the market rewards patience)

- Do your homework (knowledge is cheaper than mistakes)

- Keep your options open (flexibility is your friend)

- Build relationships with multiple lenders (because options matter)

Because at the end of the day, the economy’s like the weather – it’ll do what it’s gonna do. Your job is to figure out how to keep moving dirt no matter what it throws at you.

Best Practices for Managing Excavator Financing

Look, buying an excavator isn’t like picking up a new pickup truck. You can’t just walk in, wave your checkbook around, and drive off into the sunset. Let’s talk about how to actually manage this investment without turning your equipment loan into a money pit.

The Art of Negotiation (Or How Not to Get Taken for a Ride)

First up – let’s talk about getting the best deal. And no, we don’t mean arm-wrestling the sales rep (though some of you have probably tried).

Shop Like You Mean It

- Get quotes from at least three lenders (and make sure they know it)

- Play different dealers against each other (they expect it)

- Don’t be the guy who falls in love with the first machine he sees

- Remember: Everything’s negotiable. EVERYTHING.

Pro tip: If a dealer won’t budge on price, start talking about extras. Training packages, extended warranties, first service visit – there’s always something they can throw in.

The Payment Game

Making payments isn’t just about remembering to mail a check (who even does that anymore?). It’s about:

- Setting up auto-pay (because late fees are for suckers)

- Keeping your credit profile clean (your next deal depends on it)

- Building a relationship with your lender (trust me, you’ll need it someday)

- Documenting everything (because memory is great, paper is better)

Reading the Fine Print (Without Going Cross-Eyed)

Yeah, we know – contract language is about as exciting as watching paint dry. But here’s what you absolutely need to understand:

- Interest rate mechanics (fixed vs. variable isn’t just financial jargon)

- Early payoff terms (because sometimes you want to ditch that payment)

- Default triggers (it’s not just about missing payments)

- Insurance requirements (hint: they’re usually higher than you think)

The Maintenance Money Dance

Want to know the difference between a money-making machine and an expensive lawn ornament? Maintenance. Here’s your game plan:

- Budget 15-20% above your payment for maintenance

- Keep records like your financing depends on it (because it does)

- Don’t skip service intervals (even when you’re busy)

- Build a relationship with your service provider (they’ll remember you when you’re in a jam)

Planning for Tomorrow (While Paying for Today)

Smart operators think ahead:

- Watch your utilization rates (idle iron is expensive iron)

- Keep an eye on the market (both up and down)

- Build an upgrade strategy (before you need one)

- Know your exit options (because sometimes you need to pivot)

The Future-Proof Strategy

Here’s what the veterans do:

- Choose financing terms that match their business cycle

- Keep some powder dry for opportunities

- Build flexibility into their equipment planning

- Never max out their credit capacity

Red Flags to Watch For

If you see any of these, run (don’t walk) to your nearest exit:

- Pressure to decide “right now”

- Rates that sound too good to be true

- Hidden fees buried in the paperwork

- Maintenance restrictions that lock you into one provider

Remember: The best deals are the ones that let you sleep at night and keep working during the day. Everything else is just noise.

The Final Showdown: Comparing Your Options

Look, by now you’ve probably got more financing information bouncing around in your head than specs in a product manual. Let’s break this down into something you can actually use when you’re sitting across from that finance guy tomorrow morning.

The Tale of the Tape

First, let’s lay out the fighters in our main event – Loans vs. Leases vs. Rentals. Each one’s got their own style, their own strengths, and yes, their own ways of keeping you up at night.

The Championship Belt Comparison

| What You Care About | Loan | Lease | Rental |

|---|---|---|---|

| Ownership | She’s all yours after the last payment | Maybe yours (if you play your cards right) | Just borrowing the dance partner |

| Monthly Pain | Highest hit to the wallet | Easier to swallow | Varies by how long you need it |

| Upfront Costs | Better bring your checkbook | First and last month’s rent (usually) | Security deposit and you’re rolling |

| Tax Games | Interest and depreciation write-offs | Might be able to write off the whole payment | It’s a business expense, baby |

| Flexibility | About as flexible as a frozen hydraulic line | More moves than a seasoned operator | Float like a butterfly |

| Long-Term Cost | Cheapest in the long run (usually) | Middle of the road | Most expensive if you go long |

The Bottom Line (Because That’s What Really Matters)

Let’s wrap this whole thing up with some real talk about what all this means for your business:

When to Pull the Trigger on a Loan

- You know this iron’s gonna be with you longer than your last marriage

- You’ve got the down payment locked and loaded

- Your credit score doesn’t make bankers cry

- You like writing off depreciation and interest

When Leasing Makes All the Sense

- You want to keep your monthly nut manageable

- You like the idea of upgrading every few years

- Tax advantages matter to your bottom line

- You’re not sure if you want to marry this particular machine

When Rental Is Your Best Friend

- You need it for that one big job (you know the one)

- Your crystal ball’s a little foggy on future work

- You want to try before you buy

- Your accountant likes keeping things simple

Parting Shots (The Stuff Nobody Tells You But Should)

Before you run off to sign papers, remember:

- The lowest payment isn’t always the cheapest option

- Read the fine print like your business depends on it (because it might)

- Don’t be afraid to walk away – there’s always another deal

- Nobody ever went broke by doing their homework first

Conclusion

Let’s cut to the chase – excavator financing isn’t rocket science, it’s just dollars and sense.

Your three options each tell a different story: loans build equity but cost more monthly, leases give you flexibility with lower payments, and rentals are perfect for that one-off project without the commitment hangover.

But here’s what separates the pros from the rookies: they match their financing to their business rhythm, not just whatever deal has the shiniest brochure. They know their utilization numbers cold, keep their options open, and always leave some financial powder dry for when opportunity knocks.

Remember this: the best financing deal isn’t the one with the lowest monthly nut – it’s the one that lets you keep moving dirt while your competition is stuck explaining cash flow problems to their banker. Everything else is just paperwork.

FAQ

Is it hard to finance an excavator?

Financing an excavator isn’t inherently difficult, but approval depends on factors like credit score, business stability, and equipment value. Lenders typically require a down payment and offer terms up to 5–7 years.

Who finances excavators?

Excavators are financed through banks, equipment finance companies, and manufacturer-backed programs. These lenders specialize in heavy machinery and offer tailored terms.

How many years can you finance a excavator?

Excavator financing terms typically range from 3 to 7 years, depending on the lender and equipment value. Longer terms may require higher credit scores.

What credit score do you need to finance heavy equipment?

A credit score of 600+ is generally recommended for heavy equipment financing, though some lenders accept lower scores with larger down payments. Strong business credit history can also improve approval chances.