Use This Heavy Equipment Loan Calculator (to Estimate Your Monthly Payments)

What’s the difference between equipment operators who secure premium financing terms and those who don’t? It’s not luck – it’s leveraging two powerful tools that most owners underutilize: a heavy equipment loan calculator and an equipment appraisal.

Advanced Heavy Equipment Loan Calculator

Equipment Details

Financial Profile

Loan Terms

Additional Costs

Powered by UltimateCalculators.com, custom calculator maker …because millions are on the line.

In today’s market, where a single percentage point can mean tens of thousands in savings, understanding these tools isn’t just helpful – it’s critical. We’ve seen operators cut their interest rates by up to 2.5% and increase their approved loan amounts by 25% simply by using these tools strategically.

This guide breaks down exactly how to use financing calculators and professional appraisals to secure better terms and maximize ROI. Let's dive into the specific strategies that consistently deliver results across every major equipment category.

Understanding Heavy Equipment Financing Calculators

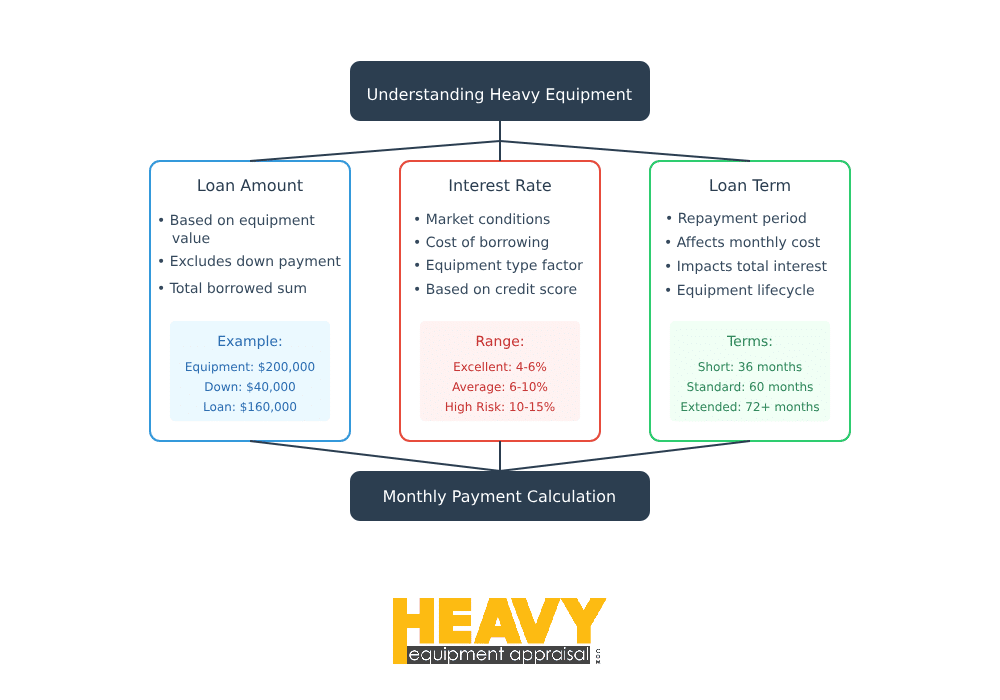

Here's a truth that might surprise you: a financing calculator is more than just a number-crunching tool - it's your first line of defense against suboptimal financing terms. At its core, this tool helps you run scenarios using three critical variables: loan amount, interest rate, and loan term. But it's how you use these variables strategically that makes all the difference.

Key Components of a Heavy Equipment Loan Calculator

Let's break down the three pillars that drive every financing calculation:

The loan amount is your starting point - the total sum you're borrowing for the equipment. This isn't always just the purchase price; it's that number minus your down payment. Smart operators know this distinction matters because it directly impacts both monthly payments and total interest paid.

The interest rate represents your cost of borrowing, expressed as a percentage. But here's what many don't realize: this rate isn't just a number pulled from thin air. Your equipment's value, condition, and market demand all play crucial roles in determining this rate. We've seen time and time again how an accurate appraisal can drive this number down.

The loan term sets your repayment timeline, typically in months or years. While longer terms mean lower monthly payments, they also mean more interest paid over time. We've found that matching your term to your equipment's expected service life often provides the optimal balance.

This seemingly simple calculator becomes a powerful strategic tool when you understand how these components interact. Each variable is a lever you can pull to optimize your financing structure.

Understanding These Components is Crucial

Look, we've seen countless equipment deals succeed or stumble based on how well owners understand these financing fundamentals. When you grasp how each component impacts your bottom line, you're not just filling in numbers – you're architecting your equipment investment strategy.

Think of it this way: every input in your financing calculator is a tactical decision point that shapes your equipment's long-term ROI.

How to Use Our Heavy Equipment Financing Calculator

Let's cut through the complexity and break this down into actionable steps. After walking thousands of equipment owners through this process, here's what works:

- Start with your loan amount. This isn't just about punching in numbers – it's about strategic positioning. Say you're looking at a $200,000 excavator and planning a $40,000 down payment. Your loan amount is $160,000. But here's what most calculators won't tell you: this ratio can significantly impact your interest rate negotiations.

- Next comes your interest rate. From our experience appraising equipment across every sector imaginable, we've seen rates typically range from 4% to 15%. But here's the kicker – your rate depends on three key factors:

- Your credit profile

- The equipment's type and condition

- Your chosen lender's risk assessment

- Then specify your loan term. We're talking months, not years. The sweet spot for heavy equipment usually falls between 36 and 72 months. But remember – this isn't just about what you can afford monthly. It's about matching your payment schedule to your equipment's revenue-generating potential.

- Here's where the magic happens: your monthly payment calculation. But don't stop there. This is your baseline for optimization, not your final answer.

Pro tip: The real power move is experimenting with different scenarios. Run multiple calculations changing one variable at a time. This isn't just number crunching – it's strategic modeling that reveals opportunities for better terms.

Understanding these outputs gives you leverage in financing negotiations. We've seen equipment owners save tens of thousands by simply understanding how these variables interact and using that knowledge strategically.

Running these calculations might feel mechanical, but each number tells a story about your equipment's financial future. It's about finding that sweet spot where monthly affordability meets long-term profitability.

The Critical Role of Equipment Appraisal in Financing

Let's get real about equipment appraisals. After thousands of valuations across every industry imaginable, we've seen one truth play out repeatedly: your equipment's appraised value isn't just a number – it's leverage in financing negotiations.

Think about it. When a lender looks at your heavy equipment, they're not just seeing a machine. They're assessing risk and potential. An accurate appraisal transforms that assessment from guesswork into concrete value. This isn't theoretical – we've watched it influence lending decisions countless times.

How Accurate Appraisals Impact Loan Terms

Here's something most equipment owners don't realize until it's too late: the difference between a quick valuation and a professional appraisal can cost you thousands in higher interest rates or reduced loan amounts.

Picture this scenario: A lender does a quick market check and values your equipment at what seems "about right." But here's where it gets interesting. That same equipment, properly appraised by someone who knows its true market value, maintenance history, and current demand? It could tell a completely different story.

And this isn't just about getting a higher number. It's about getting the right number, backed by real market data and deep industry expertise. When you walk into a financing discussion with this level of documentation, you're not just asking for better terms – you're justifying them.

For example, if an appraisal proves your equipment's value is underestimated, you're not just losing out on loan amount – you're potentially:

- Paying a higher interest rate than necessary

- Getting stuck with less favorable terms

- Missing out on better financing options

- Leaving money on the table that could be used for business growth

Case Study: Improved Financing Through Expert Valuation

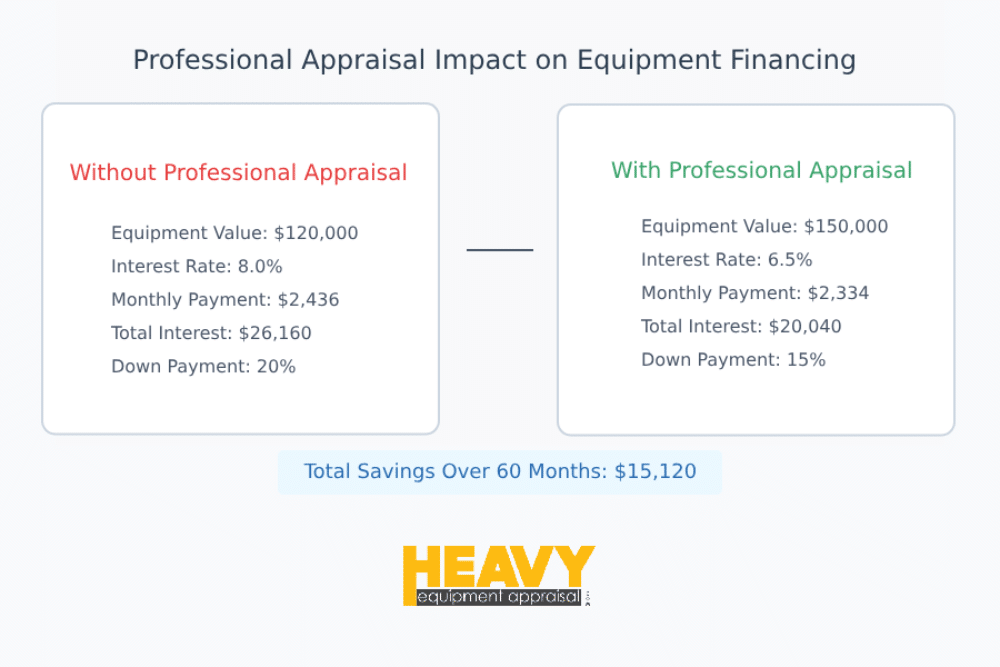

Let's make this concrete. Recently, a construction company came to us about financing a used Caterpillar 336 excavator. The initial lender appraisal? $120,000 with an 8% interest rate. Pretty standard, right?

But here's where it gets interesting. Our detailed appraisal valued the excavator at $150,000. Why the difference? We factored in its excellent condition, recent maintenance records, and current market demand – details that matter to serious equipment buyers but often get overlooked in quick valuations.

The result? They secured a 6.5% interest rate and a higher loan amount. Over a 60-month term, that interest rate difference alone saved them about $15,000. Plus, they kept more working capital in their pocket thanks to the higher loan amount.

This isn't just a story about saving money. It's about using accurate equipment valuation as a strategic tool to create better business outcomes. We see this pattern repeat across industries, equipment types, and deal sizes.

Factors Affecting Your Monthly Payments

After appraising equipment for decades, we've noticed something interesting: many owners focus exclusively on monthly payment amounts without seeing the bigger strategic picture. Let's change that perspective.

Think of your monthly payment as the outcome of a complex equation – one where every variable is an opportunity for optimization. Master these variables, and you've mastered your equipment financing strategy.

Loan Amount and Down Payment

Here's where strategic thinking pays off big time. Your loan amount isn't just about what you can borrow – it's about what you should borrow. Let's break this down:

Take that $250,000 piece of equipment you've got your eye on. Sure, you could finance the whole amount, but consider this: putting down $50,000 doesn't just reduce your loan to $200,000 – it signals to lenders that you're a serious operator who understands risk management. We've seen this approach consistently lead to better interest rates and terms.

But here's the part that often gets overlooked: your down payment strategy should align with your equipment's revenue potential. Sometimes, keeping more capital liquid for operations can be smarter than making a larger down payment. It's about balance.

Interest Rate and Credit Score

Let's get real about interest rates for a moment. They're not just numbers pulled from thin air – they're a direct reflection of how lenders view your risk profile. Here's what you might not know: your credit score is just one piece of the puzzle.

We've seen businesses with identical credit scores get vastly different rates because one had detailed equipment valuations and maintenance records while the other didn't. A 780 credit score might get you that sweet 5% rate, while a 650 could mean living with 8% or higher.

But here's the strategic play: combine a strong credit profile with professional equipment documentation, and you're not just asking for better rates – you're justifying them with hard data.

Loan Term and Residual Value

This is where most financing conversations get interesting. The loan term isn't just about spreading payments out – it's about aligning your financing strategy with your equipment's lifecycle.

Think about it this way:

- A 72-month term means lower monthly payments but more total interest

- A 36-month term means higher payments but potential savings on total interest

- Your equipment's residual value can be leveraged for better terms

Here's what's really fascinating: we're seeing more operators match their loan terms to their equipment's projected value curves. Why? Because understanding how your equipment holds value over time lets you structure payments that make sense for your business cycle.

The residual value piece is particularly crucial. Higher residual values can mean lower monthly payments, but watch out for that balloon payment at the end. It's not just about can you afford the payments today – it's about positioning yourself for success throughout the entire financing cycle.

Interpreting Calculator Results

After spending years in equipment yards from coast to coast, I can tell you – punching numbers into a calculator is the easy part. The real skill? That's in reading between the lines of those results.

Think of your financing calculator as a business intelligence tool, not just a payment estimator. The numbers it spits out? They're telling you a story about your equipment's financial future.

Understanding Total Cost of Ownership

Here's where things get interesting – and where most operators miss crucial opportunities.

That monthly payment staring back at you from the calculator? It's just the tip of the iceberg. The real story lies in your total cost of ownership. Let me break this down the way I would for a veteran operator looking to level up their financing game:

Your total cost includes:

- Monthly payments (the obvious part)

- Total interest over the loan's life (the sneaky part)

- Associated fees (the part most calculators conveniently forget)

Here's what keeps blowing minds in our appraisal work: We regularly see deals where a lower monthly payment actually costs tens of thousands more in the long run. Not because anyone's trying to pull a fast one, but because focusing on monthly payments alone is like judging an engine by its paint job.

Balancing Monthly Payments with Long-Term Value

Let's get tactical about this.

You're probably thinking: "Sure, but I still need those payments to work with my cash flow." Fair point. Here's how the pros play it:

First, they understand the relationship between payments and value retention. That longer term with the tempting lower payment? It might look good now, but if your equipment depreciates faster than you're building equity, you're playing a dangerous game.

We see this play out in real time: Equipment that holds its value well (think certain excavator models or specialized machinery) can actually justify longer terms. Why? Because even at the back end of the loan, you've got solid asset value backing up your position.

Pro tip from the appraisal trenches: The sweet spot is where your equity position stays ahead of market depreciation by at least 15-20%. Any less, and you're one market downturn away from being underwater on your iron.

This isn't just theory – we've documented hundreds of cases where understanding these relationships made the difference between a good deal and a great one. Just last month, an operator used this exact approach to negotiate terms that saved him $23,000 over the life of his loader loan.

Remember: Every number in that calculator represents a strategic choice. Your job isn't just to find payments you can afford – it's to structure a deal that builds equity while protecting your cash flow. It's about making your equipment's value work as hard as the machine itself does.

Advanced Considerations in Heavy Equipment Financing

After two decades of crawling over equipment and diving deep into financing structures, I can tell you this: the real magic happens when you look beyond the basics. Let's explore some of the less obvious factors that can make or break your equipment financing strategy.

Equipment Condition and Market Demand

Here's something that might surprise you: your equipment's condition isn't just about maintenance records and hour meters. It's about market positioning.

The truth? Equipment in excellent condition with high market demand isn't just easier to finance – it's a strategic asset that can transform your entire financing package. Let me share what we're seeing in the field:

A well-maintained excavator with low hours isn't just a good machine – it's leverage in your financing negotiations. We recently appraised two identical models, same year. The difference in financing terms? Nearly 2 percentage points, purely based on condition and documented maintenance. That's tens of thousands in savings over the loan term.

Depreciation Schedules and Residual Value

Now, let's talk about something that keeps equipment finance managers up at night: depreciation schedules.

Think of depreciation like your equipment's financial GPS – it tells you where your value is heading. But here's what most owners miss: depreciation isn't just about tax write-offs. It's about strategic timing.

Consider this scenario:

- Fast-depreciating equipment? You might want shorter terms

- Stable value retention? Longer terms could work in your favor

- High residual value? That's your ace in lease negotiations

Pro tip from the appraisal trenches: Some lenders offer accelerated depreciation options. But before you jump at that, consider how it affects your equipment's book value versus market value. We've seen this gap create unexpected challenges in refinancing situations.

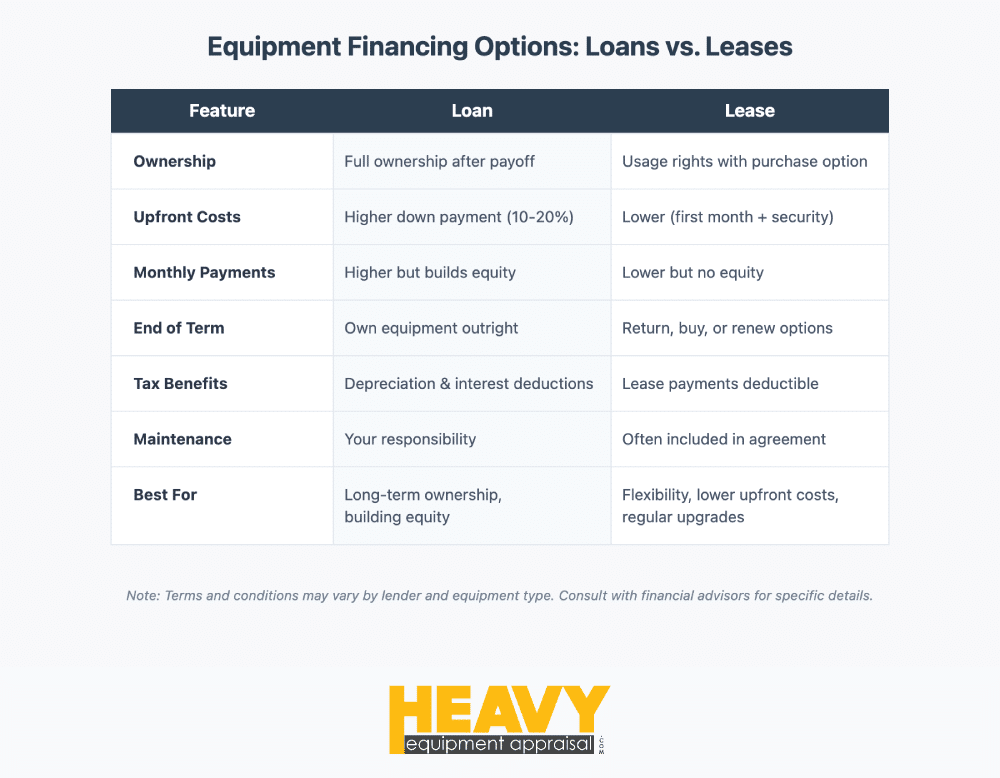

Comparing Financing Options

This is where the rubber meets the road. Let's break down loans versus leases, but not in the usual textbook way. Here's what we've learned from thousands of equipment deals:

Loans vs. Leases for Heavy Equipment

| Feature | Loan | Lease |

|---|---|---|

| Feature | Loan | Lease |

| Ownership | You own it outright after payments | Think of it as a strategic rental with options |

| Upfront Costs | Higher, but builds equity faster | Lower, preserves working capital |

| Monthly Payments | Can vary based on structure | Often lower, but watch the terms |

| End of Term | It's yours - sell it, trade it, keep it | More options, but less equity |

| Flexibility | Less flexible, but builds asset value | More flexible for equipment updates |

| Tax Implications | Depreciation deductions | Payments usually deductible |

| Long-Term Cost | Known from day one | Can be higher if you buy at term end |

| Maintenance | Your responsibility | Sometimes included (read the fine print) |

| Equipment Usage | Complete control | Watch those usage restrictions |

| Best For | Building equity, long-term growth | Flexibility and cash flow management |

Specialized Financing Programs for Construction Equipment

Here's an insider secret: some of the best financing deals aren't advertised. From emissions compliance incentives to manufacturer-backed programs, there's a whole world of specialized financing most owners never discover.

We've helped clients tap into programs offering rates as low as 0.9% through manufacturer incentives. The catch? You need to know they exist and how to qualify. This is where having an expert in your corner really pays off.

Maximizing ROI on Your Equipment Investment

Let me share something that might surprise you: financing terms and accurate appraisals aren't just paperwork – they're your secret weapons for maximizing ROI. After thousands of equipment valuations, I've seen how the right combination can transform a decent investment into a game-changing one.

Strategies for Optimizing Financing Terms

Here's the thing about financing terms: they're not set in stone until you sign. Every single component is negotiable if you know how to play your cards right. Let's break down the strategies that consistently deliver results:

Improving your credit score? That's table stakes. But let me show you what the pros do:

- Make that down payment work harder: Strategic down payments aren't about putting down as much as you can – they're about finding the sweet spot where you maximize leverage while maintaining operational cash flow.

- Get serious about appraisals: A professional appraisal isn't an expense – it's an investment that often pays for itself many times over. We've seen accurate appraisals knock whole percentage points off interest rates.

- Shop smart for lenders: Different lenders specialize in different equipment types. Knowing this landscape can be the difference between average terms and exceptional ones.

- Master the art of negotiation: Walk in with market data, comparative values, and detailed equipment documentation. It's about showing lenders you understand both the asset and the business case.

Leveraging Accurate Appraisals in Negotiations

Want to know what separates good deals from great ones? It's not just having an appraisal – it's knowing how to use it strategically.

Picture this: You walk into a financing discussion armed with a professional appraisal that doesn't just state a value – it tells a story about your equipment's:

- Current market position

- Maintenance history

- Performance metrics

- Future value projections

That's not just documentation – that's negotiating power.

Pro tip from the field: We recently watched a client use their appraisal to challenge a lender's initial valuation. Result? They secured terms that saved them $37,000 over the life of the loan. The kicker? The appraisal cost less than $1,000.

Expert Tips for Securing the Best Heavy Equipment Financing

Think of securing equipment financing like assembling a high-performance engine – every component needs to work together perfectly. After helping countless operators optimize their financing, here's what separates the winners from the rest:

Preparing Your Financial Documents

First move? Get your financial documents in order. But not just any documents – you need a strategic package that tells your equipment's whole story:

- Business financial statements that highlight growth patterns

- Tax returns showing consistent performance

- Bank statements demonstrating solid cash flow

- Equipment specs that emphasize value-adding features

- A business plan that shows exactly how this equipment drives growth

- Personal financial statements (when required) that strengthen your case

Don't just dump these on a lender's desk. Present them strategically, using each document to reinforce your position as a low-risk, high-potential investment.

Timing Your Equipment Purchase and Financing

Think of equipment purchasing like surfing – timing is everything. After two decades of watching market cycles, I've seen how perfect timing can turn a good deal into a great one. But here's the twist: perfect timing isn't about luck. It's about strategy.

Let me share something that might surprise you: the best equipment deals often happen when everyone else is sitting on their hands.

Strategic Timing Considerations

Here's what seasoned operators know that others miss:

High demand periods aren't just about higher prices – they fundamentally shift your negotiating position. Picture this: you're one of twenty buyers eyeing the same excavator. Not exactly a recipe for leverage, right?

But flip the script. During off-peak seasons, we regularly see clients secure:

- More flexible financing terms

- Better interest rates

- Longer grace periods

- Manufacturer incentives you won't find in peak season

One of our clients just landed a premium-grade loader with unprecedented financing terms – all because they moved in December when everyone else was wrapping up their year-end books.

Market Conditions and Timing

Let's get tactical about this. Your timing strategy needs to account for:

- Seasonal business cycles in your industry

- Regional market variations (they're bigger than you think)

- Current regulatory environment

- Economic indicators

- Technology upgrade cycles

- Environmental compliance deadlines

Pro tip: Watch for the convergence of multiple favorable factors. That's your sweet spot.

The Interest Rate Game

Here's where timing gets really interesting. Interest rates aren't just numbers on a screen – they're opportunities in disguise.

Consider this scenario we just saw play out: A client was ready to pull the trigger on financing in a high-rate environment. Instead, we helped them structure a bridge solution that gave them breathing room to wait for better rates. The payoff? A 2.3% lower rate when they finally financed, saving them six figures over the loan term.

Manufacturer Incentives and Programs

Want to know a secret? Manufacturers sometimes offer better financing deals than traditional lenders – but timing is critical.

Watch for:

- End-of-quarter incentives

- Model year changeover specials

- Emissions compliance upgrade programs

- Technology adoption incentives

The real pros stack these incentives. We recently helped a client combine end-of-year manufacturer incentives with their bank's equipment modernization program. The result? Terms that seemed impossible just months earlier.

Remember: Every equipment purchase is a chess game, not a race. Sometimes the best move is waiting for the right moment to strike. But when that moment comes? You need to be ready with everything lined up – financing pre-approval, appraisals in hand, terms negotiated.

Conclusion: Making Informed Decisions with Expert Guidance

A financing calculator combined with professional equipment appraisals gives you both tactical insight and strategic leverage. Success comes from using these tools together to secure optimal financing terms.

Equipment financing isn't just about getting approved – it's about structuring deals that build equity while protecting cash flow. Professional appraisals often pay for themselves through better rates and terms, while strategic timing can unlock manufacturer incentives and favorable market conditions.

Your equipment's value is leverage in negotiations. Each component – from loan terms to down payments – represents an opportunity to improve your position. Use your documentation strategically, focusing on elements that demonstrate asset value and business strength.

The path forward is clear: master your financing calculator, secure professional appraisals, and time your moves strategically. Don't settle for standard terms when your equipment's true value can command better ones.