Documents Needed for an Equipment Appraisal (Complete Checklist)

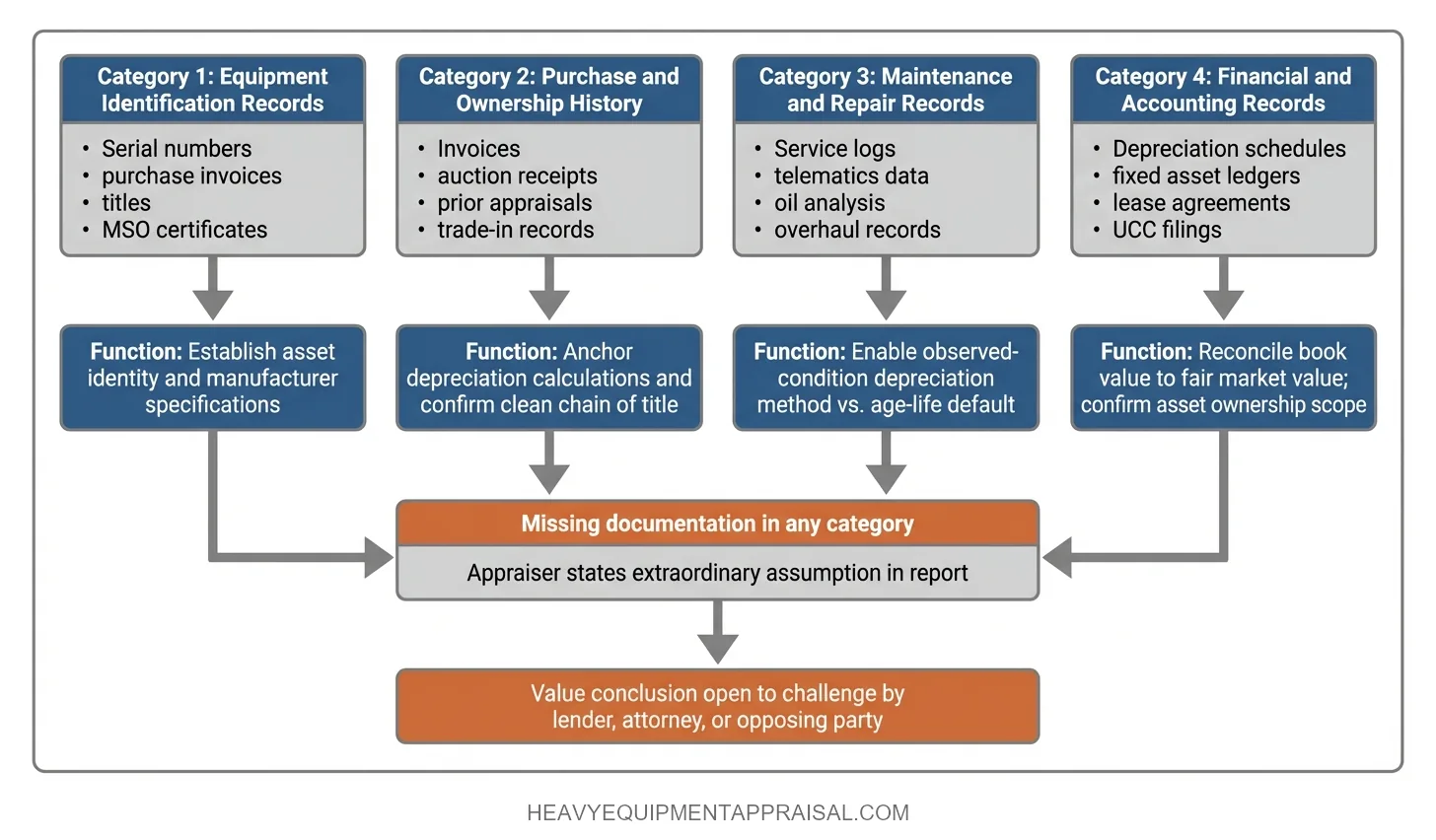

An equipment appraisal requires 4 core document categories:

- Equipment identification records

- Purchase and ownership history

- Maintenance and repair logs

- Use-case-specific financial or legal documents

The exact mix varies by appraisal purpose. For example, an SBA loan collateral review, an insurance claim, and a divorce proceeding each demand different supporting records.

Incomplete documentation forces the appraiser toward broader market assumptions, which typically produces a less precise and often less favorable value conclusion.

Why Documents Matter to the Appraisal Outcome

The documents an owner provides directly control how precisely an appraiser can determine value.

Every record serves one of three functions:

- Establishing the equipment’s identity (make, model, year, serial number)

- Confirming its condition history (maintenance performed, components replaced, hours of use)

- Supporting the depreciation adjustments that translate replacement cost into current value

Without these inputs, the appraiser must fill gaps through inference, broader market averages, and conservative assumptions. Well-documented equipment allows the appraiser to make unit-specific adjustments.

A 2018 excavator with 4,200 hours, a documented undercarriage rebuild at 3,000 hours, and original purchase records gives the appraiser concrete data points for both the cost approach and sales comparison approach.

The depreciation estimate reflects this specific unit’s history, not a statistical average for its class.

Undocumented equipment receives no such benefit.

When maintenance records are absent, the appraiser assumes typical wear for the asset’s age and reported hours. When hour meter readings are unavailable or suspect, the appraiser defaults to industry-average annual usage. These defaults rarely favor the owner.

The appraiser is also required to disclose in the report what information was available, what was relied upon, and what was absent. Missing documentation becomes a stated limitation of the appraisal process, visible to any lender, attorney, or counterparty reviewing the report. A value conclusion built on verified records carries more weight in negotiation, litigation, and lending decisions than one qualified by data gaps.

Complete documentation does not guarantee a higher value, but it removes the downward pressure that incomplete records create.

Equipment Identification Documents

Serial numbers are the single most important data point an appraiser uses to verify equipment identity, retrieve manufacturer specifications, and locate comparable sales.

Every appraisal starts with confirming what the asset actually is, and the following documents serve that function:

- Purchase invoices

- The original invoice from the dealer or manufacturer confirms make, model, year, serial number, and the equipment’s configuration at the time of sale. Invoices also document optional attachments, packages, or upgrades that affect the unit’s specification profile and its replacement cost.

- Certificates of origin / manufacturer’s statements of origin (MSO)

- Issued by the manufacturer, these certificates establish the unit’s production details and original equipment specifications. They are particularly relevant for newer assets or units purchased directly from the factory.

- Titles and registration documents

- Required for titled assets (trucks, trailers, certain mobile equipment), titles confirm legal ownership and VIN or serial number. For assets that cross state lines or change hands frequently, title history helps the appraiser confirm chain of ownership and flag encumbrances.

- Serial number documentation (nameplates, data plates, manufacturer records)

- The serial number is the primary key that links a physical asset to the manufacturer’s build records, including model variant, factory options, and production date. Appraisers use serial numbers to pull spec sheets, decode configuration, and search auction databases for transactions involving the same or comparable models.

When serial numbers are missing, illegible, or altered, the appraiser must establish identity through alternative means: physical configuration analysis, capacity measurements, and cross-referencing available records. This adds scope to the engagement and is disclosed as a limitation in the report.

An asset whose identity cannot be verified against manufacturer data is effectively cut off from the sales comparison approach, limiting the appraiser to less precise valuation methods.

Purchase and Ownership History

Original purchase invoices, auction receipts, and prior appraisal reports establish the acquisition cost and acquisition date that anchor depreciation calculations in the cost approach. These records also create a chain of ownership that lenders and attorneys rely on to confirm the asset is unencumbered and legally available as collateral or for transfer.

Purchase invoices and dealer agreements

Document the original transaction price, the date of acquisition, and the buyer-seller relationship. The acquisition cost gives the appraiser a known starting point for the cost approach: rather than estimating replacement cost new from catalog data alone, the appraiser can cross-reference the actual price paid against published pricing for the same year and configuration. Dealer agreements may also document trade-in allowances, financing terms, or bundled service packages that affect the net cost attributable to the equipment itself.

Auction Receipts

Auction receipts serve as the primary ownership record when equipment was acquired through liquidation or resale channels rather than a dealer. The receipt confirms the hammer price, buyer’s premium, and sale date. Because auction-sourced equipment often lacks the documentation trail of a dealer purchase, the receipt may be the only record linking the current owner to a specific acquisition cost and timeline.

Prior Appraisal Reports

Prior appraisal reports provide historical value benchmarks. They are not binding on the current appraiser, but they establish what the equipment was valued at in a previous period and can inform time-based adjustments. In litigation or divorce proceedings, a prior appraisal dated close to a relevant legal event (separation date, filing date) carries particular weight.

Trade-In Records

Trade-in records clarify situations where the owner acquired equipment as part of an exchange. Without these records, the appraiser cannot isolate the cost basis of the current asset from the bundled transaction.

Ownership history matters beyond depreciation math. In SBA loan appraisals and divorce or estate proceedings, a lender or court needs confidence that the asset’s chain of title is clean. Gaps in ownership documentation raise questions about liens, prior encumbrances, or disputed title that can render an otherwise sound value conclusion unusable for the intended purpose.

Maintenance and Repair Records

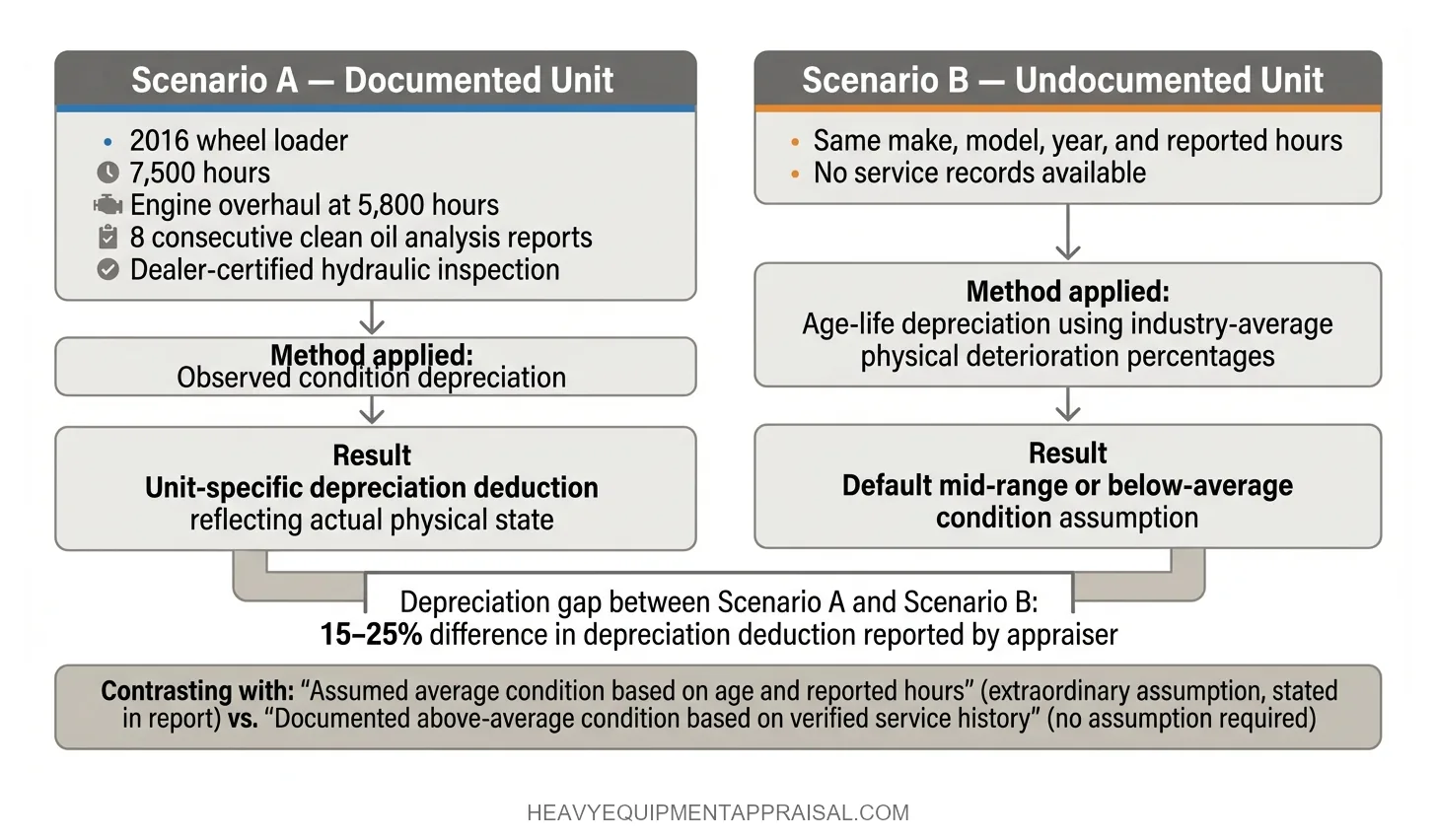

Documented service history is the primary input that separates a unit-specific condition rating from a generic age-based depreciation estimate.

Service logs, dealer inspection reports, oil analysis results, overhaul records, hour meter readings, and telematics reports each provide evidence of how the equipment has actually been maintained, not how a statistical average unit of the same age and class would be expected to perform. The appraiser uses this evidence to assign a condition rating that reflects observed reality rather than default assumptions.

The distinction matters in dollar terms.

When maintenance records are available, the appraiser can apply the observed condition method of depreciation, which calibrates physical deterioration to specific events: a transmission rebuild at 6,000 hours, clean oil analysis reports across eight consecutive intervals, or a dealer-certified inspection confirming hydraulic system integrity. A 2016 wheel loader with 7,500 hours and a documented engine overhaul at 5,800 hours receives a materially different depreciation deduction than the same model and hours with no service records. Without records, the appraiser defaults to the age-life method, applying industry-average physical deterioration percentages that trend toward mid-range or below-average condition assumptions.

Undocumented equipment rarely receives the benefit of the doubt.

Telematics data from OEM platforms (John Deere JDLink, Caterpillar Product Link, Komatsu KOMTRAX) adds a layer of verification that paper logs alone cannot provide. These systems track cumulative hours, idle time ratios, fault codes, and geographic operating history. An appraiser reviewing telematics data can confirm that reported hours are consistent with system-recorded hours, identify whether the unit operated in severe-duty conditions, and verify maintenance interval compliance flagged by the system.

Owners should gather service logs from in-house maintenance staff, dealer service records, third-party repair invoices, fluid analysis reports, and any telematics exports available from the manufacturer’s portal.

Hour meter photographs taken at regular intervals also establish a usage timeline the appraiser can reference. The more granular the maintenance documentation, the more precisely the appraiser can position the asset’s condition within the range of comparable units used in the sales comparison approach and the cost approach.

That precision directly affects the concluded value: well-maintained equipment with records to prove it consistently appraises above otherwise identical units whose condition can only be assumed.

Financial and Accounting Records

Depreciation schedules, fixed asset ledgers, and lease agreements provide the financial context an appraiser needs to reconcile book value with market value and to confirm the scope of assets under appraisal.

These records are not valuation inputs in the same way that maintenance logs or serial numbers are. They are reference documents that help the appraiser understand how the owner has treated the asset for accounting and tax purposes, which often diverges significantly from what the equipment is worth in the open market.

Depreciation Schedules and Fixed Asset Ledgers

Depreciation schedules and fixed asset ledgers show the owner's cost basis, placed-in-service date, depreciation method (straight-line, MACRS, bonus depreciation), and current book value for each asset.

The appraiser reviews these to identify what assets the owner believes are on the books, to cross-reference against physical inventory, and to flag discrepancies. Book value and fair market value are calculated from entirely different frameworks: accounting depreciation follows IRS or GAAP rules on predetermined schedules, while appraisal depreciation reflects observed physical deterioration, functional obsolescence, and economic obsolescence as they exist in the market.

A CNC machining center fully depreciated to $0 on a 7-year MACRS schedule may still carry a fair market value of $85,000 based on comparable sales. That gap between book and appraised value is the central issue in purchase price allocations, tax-related appraisals, and M&A transactions.

Prior Insurance Valuations

Prior insurance valuations give the appraiser a historical reference point for insured value, which is typically replacement cost based. These reports are useful for triangulating replacement cost new figures, but they do not substitute for a current appraisal because insured values reflect a different premise and may be outdated.

Lease Agreements and UCC Filings

Lease agreements and UCC filings clarify which assets the owner actually owns versus those held under operating leases, capital leases, or secured financing arrangements. An appraiser cannot value what the client does not own. UCC-1 filings identify secured creditors with a recorded interest in specific equipment, which matters directly in SBA lending and liquidation scenarios where lien position determines whose collateral claim the appraisal supports.

When financial records are absent or incomplete, the appraiser loses the ability to reconcile the physical asset list against the owner's accounting records, increasing the risk that assets are double-counted, omitted, or misattributed between real and personal property.

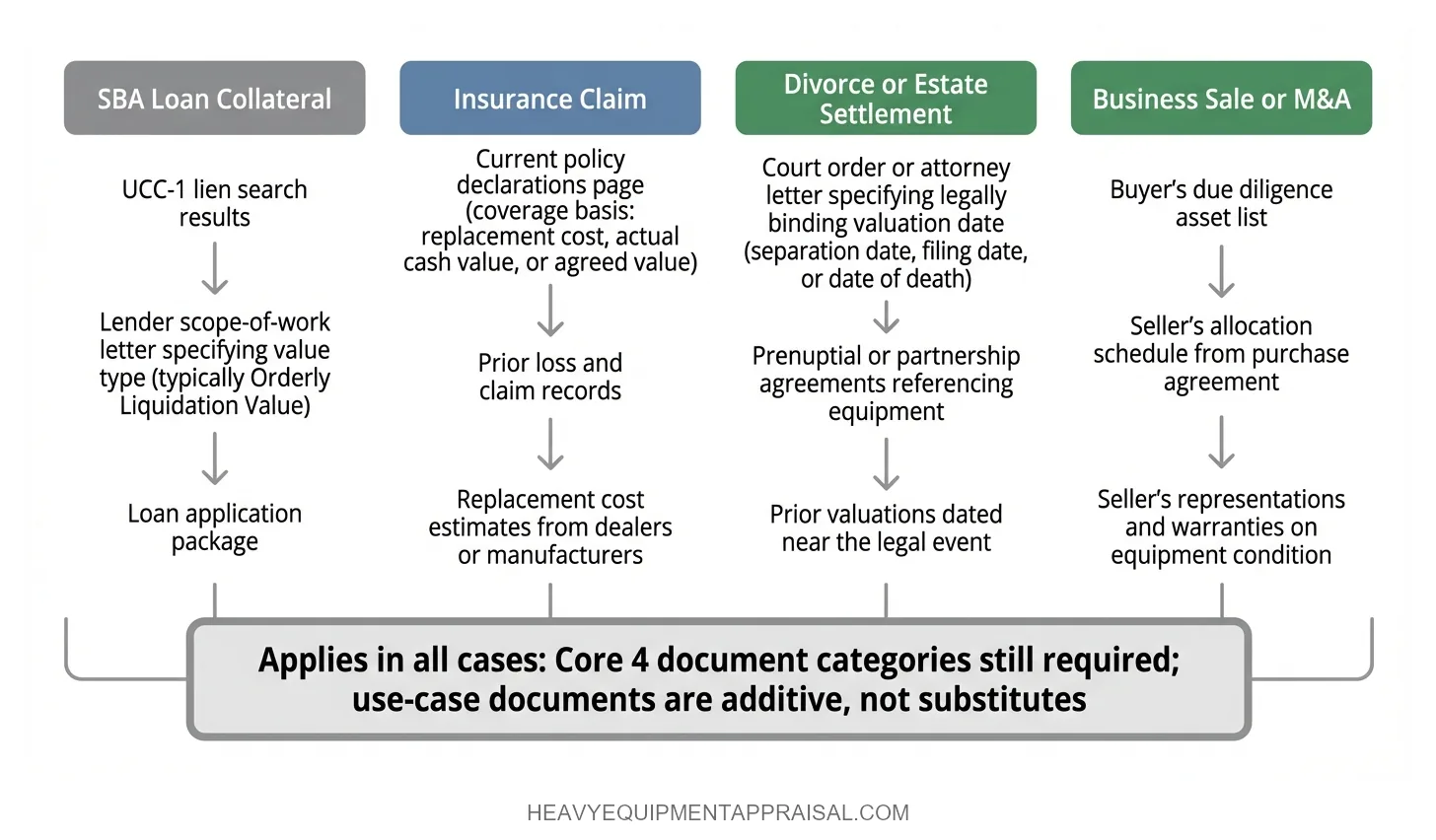

Use-Case-Specific Documents

Different appraisal purposes require different supporting documents beyond the core set of identification, ownership, maintenance, and financial records.

An SBA lender, an insurance carrier, a divorce attorney, and an M&A advisory team each need the appraisal to answer a different question, and the documents that support each answer vary accordingly.

The table below summarizes the additional documents by use case. Prose follows with context on why each set matters.

| Use Case | Additional Documents Required |

|---|---|

| SBA loan collateral | UCC-1 lien search results, loan application package, lender's scope-of-work letter specifying value type (typically OLV) |

| Insurance | Current policy declarations page, prior loss or claim records, replacement cost estimates from dealers or manufacturers |

| Divorce or estate settlement | Court order or attorney engagement letter specifying valuation date, prenuptial or partnership agreements referencing equipment, any prior valuations dated near the separation or death event |

| Business sale or M&A | Allocation schedules from the purchase agreement, seller's representations and warranties regarding equipment condition, due diligence asset list from the buyer's advisory team |

For SBA loan appraisals, the lender's scope-of-work letter is the controlling document. It specifies the value type, the effective date, and any SOP requirements the appraiser must follow. UCC lien search results confirm that the collateral is not already pledged to another creditor. Without the lender's letter, the appraiser cannot confirm the engagement parameters, which risks producing a report the lender rejects on procedural grounds.

Insurance appraisals require the current declarations page because it establishes the insured value and coverage basis (replacement cost, actual cash value, or agreed value). Prior claim records reveal whether the equipment has sustained damage that was repaired or partially settled, both of which affect the appraiser's condition analysis.

Divorce and estate proceedings hinge on the valuation date. A court order or attorney letter that specifies the legally relevant date (date of separation, date of death, date of filing) determines which market conditions the appraiser must reflect. A report valued as of the wrong date is procedurally deficient regardless of its accuracy.

In M&A transactions, the buyer's due diligence asset list and the seller's allocation schedule define what is being valued and how the concluded values feed into the purchase price allocation. Misalignment between the appraiser's asset list and the deal documents creates reconciliation problems that delay closing.

Each use case adds a layer of purpose-specific documentation that shapes not just the value conclusion but the report's admissibility and acceptance by the intended user. An appraisal that reaches the right number but omits required use-case documents may fail its intended function entirely.

What Happens When Documents Are Unavailable

Missing documentation does not prevent an appraisal from proceeding, but it changes the scope of work, introduces extraordinary assumptions, and reduces the precision of the value conclusion.

Under USPAP Standards Rule 1-2, the appraiser must identify all information necessary to correctly identify the subject property and develop credible results.

When that information is unavailable, the appraiser does not stop. Instead, the appraiser documents the gap, states the extraordinary assumption that substitutes for the missing fact, and discloses the potential impact on the concluded value.

A typical extraordinary assumption reads: "Condition assumed to be average based on age and reported hours due to absence of maintenance records." If that assumption is later found to be false, the entire value conclusion may be invalidated.

The practical consequences are predictable:

- Without purchase records, the appraiser estimates replacement cost new from published indices and manufacturer price lists rather than a documented cost basis.

- Without service logs, the appraiser defaults to age-life depreciation instead of the more favorable observed condition method.

- Without serial numbers, comparable sales searches narrow or collapse entirely.

Each substitution trades specificity for generalization, and generalizations in equipment valuation trend toward the middle of the range or below. The cumulative effect of multiple documentation gaps compounds: an asset missing both purchase records and maintenance history carries more assumed risk than one missing either alone.

Owners facing an upcoming appraisal with incomplete records can take steps to reconstruct documentation before the effective date. Contacting the original dealer for duplicate invoices, requesting service history from third-party shops, downloading telematics data from the manufacturer's portal, and photographing serial number plates and hour meters all produce usable inputs.

Even partial reconstruction narrows the appraiser's reliance on assumptions.

A single dealer service printout covering major repairs can shift the condition rating from "assumed average" to "documented above-average," a distinction that directly changes the depreciation deduction applied in the cost approach. Every extraordinary assumption stated in the report is a point where a lender, attorney, or opposing party can challenge the conclusion's credibility, so fewer assumptions mean a more defensible appraisal.

How to Organize and Deliver Documents to Your Appraiser

Delivering documents organized by individual equipment unit, in digital format, before the scheduled inspection or desktop review date produces the fastest turnaround and the fewest follow-up requests. The following sequence covers preparation through delivery.

- Create a folder per asset. Name each folder with a consistent convention: manufacturer, model, serial number (e.g., "Caterpillar_336F_CAT00336FHWBK01234"). Place every document related to that unit in its folder: purchase invoice, title, service records, hour meter photo, lease agreement, and any prior appraisals.

- Build or update a master asset list. A single spreadsheet listing every unit with columns for make, model, year, serial number, hours or miles, and location gives the appraiser a framework to check each folder against. This list becomes the index the appraiser uses to confirm nothing is missing or duplicated.

- Convert paper records to PDF. Scan or photograph paper invoices, handwritten service logs, and title documents. Legibility matters more than resolution. Name each file descriptively ("Service_Log_2019–2023.pdf"), not generically ("scan001.pdf").

- Flag known gaps. If a serial number plate is illegible or a purchase invoice was never retained, note it in the master list rather than leaving the folder empty with no explanation. Identifying gaps upfront lets the appraiser plan field verification before arriving on site.

- Deliver the complete package at least 5–7 business days before the scheduled date. Use a shared cloud folder (Google Drive, Dropbox, OneDrive) or a single compressed archive sent via email. Early delivery gives the appraiser time to review the records, identify missing items, and request supplements before the inspection rather than after.

Organized, early delivery reduces the number of extraordinary assumptions the appraiser must state in the report, which strengthens the conclusion's standing with any third party who reviews it.

FAQ

What documents do I need for an equipment appraisal for an SBA loan?

Provide appraisal request documents by submitting an equipment schedule, purchase invoices, and financing details. Include asset descriptions, serial numbers, locations, and current use. Add maintenance logs, condition reports, and photos. Provide ownership proof, lien information, and prior appraisals to support SBA-compliant valuation standards.

Can an equipment appraisal proceed without maintenance records?

An equipment appraisal can proceed without maintenance records, but missing records reduce valuation accuracy and may lower appraised value by 10–30%. Appraisers rely on maintenance history to confirm condition, useful life, and risk. Without records, appraisers apply conservative assumptions and stricter inspection standards for SBA compliance.

How does a serial number affect an equipment appraisal?

A serial number increases equipment appraisal accuracy by verifying identity, age, manufacturer, and specifications. Appraisers use serial numbers to match assets with market data, confirm ownership, and detect liens or theft records. Missing serial numbers increase risk and can reduce appraised value by 5–20% due to uncertainty.

What happens if I cannot find the original purchase invoice for my equipment?

An equipment appraisal can still proceed without the original purchase invoice, but the appraiser will require substitute proof of ownership and cost. Provide bank statements, canceled checks, tax depreciation schedules, financing documents, insurance records, or vendor confirmations. Missing invoices increase uncertainty and may reduce appraised value by 5–15%.

What telematics data should I provide to an equipment appraiser?

Provide telematics data by submitting engine hours, mileage, fuel usage, idle time, GPS location history, and utilization rates. Include fault codes, maintenance alerts, and duty cycles. Appraisers use this data to verify usage intensity, condition, and remaining life, which can shift appraised value by 10–25%.

How far in advance should I send documents to my equipment appraiser?

Send equipment appraisal documents 5–10 business days before inspection or report start. Early submission allows document review, data verification, and scheduling adjustments. Complex equipment portfolios require 10–15 business days. Late or incomplete documents delay reporting timelines by 2–7 days and can reduce appraisal accuracy.

Does a prior appraisal report count as documentation for a new appraisal?

A prior appraisal report counts as supporting documentation but does not replace a new appraisal. Appraisers use prior reports to verify asset history, valuation methods, and market trends. SBA guidelines require a current, independent appraisal, so outdated reports only support analysis and may influence value by 5–15%.

What documents does a divorce attorney need from an equipment appraisal?

Provide divorce appraisal documents by including a certified appraisal report with a defined valuation date, asset identification, and condition support. Include serial numbers, ownership history, and prior appraisals near the separation date. Add court orders or attorney letters to ensure the appraisal meets legal standards for asset division.