Equipment Appraisal for Selling a Business or M&A Transaction

A certified equipment appraisal in a business sale or M&A transaction establishes supportable asset values that protect both parties during due diligence, support purchase price allocation under IRS requirements, and provide the documented basis for post-closing tax filings.

Any business where machinery, vehicles, or equipment represent a material portion of total asset value needs independent valuation before the deal closes.

This article covers the specific points in the deal process where an equipment appraisal is required, strategically important, or both.

Why Equipment Value Is a Deal Variable, Not a Detail

In any business sale where equipment constitutes a material asset class, an unsupported or informally estimated equipment value creates negotiation risk, post-closing tax exposure, and potential dispute liability.

Buyers and sellers routinely disagree on what equipment is worth because they start from different reference points. The seller sees replacement cost and operational value. The buyer sees depreciated book value and resale potential.

The gap between these perspectives is not trivial:

A $2M equipment line on a company's balance sheet reflects GAAP book value, which is the original cost minus accounting depreciation. That number may bear no relationship to what FMV assumes about buyer and seller behavior. Fully depreciated CNC machining centers still running production carry zero book value but may hold $400,000 or more in market value. Conversely, recently purchased equipment may carry inflated book value that exceeds what any buyer would pay on the secondary market.

Without an independent appraisal, the equipment component of a purchase price is negotiated on assumptions rather than evidence. The buyer anchors to book value. The seller anchors to replacement cost. Neither number reflects the actual market.

The result:

A disputed allocation, an IRS challenge, or a deal that stalls in due diligence because neither party can substantiate their position.

An independent appraisal replaces assumption with documentation, giving both parties a credentialed, methodology-backed number that holds up under audit or litigation.

Purchase Price Allocation Requires a Certified Equipment Appraisal

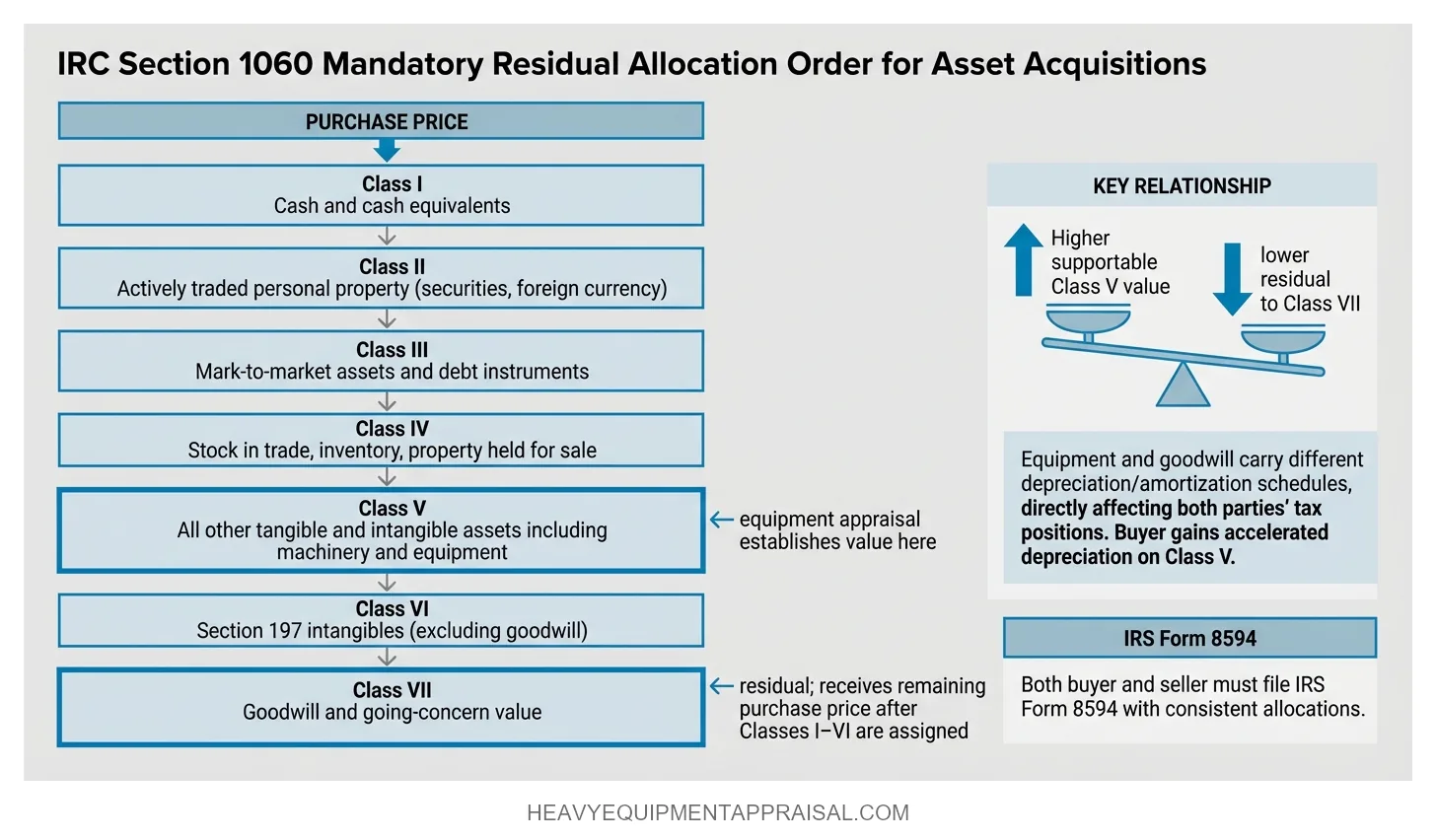

IRC Section 1060 requires that the purchase price in any asset acquisition be allocated across seven asset classes using fair market value (FMV), with machinery and equipment falling under Class V.

Both buyer and seller must file IRS Form 8594 (Asset Acquisition Statement) with their tax returns for the year of the sale, and there is no dollar threshold below which this requirement is waived.

The seven classes are allocated in a mandatory residual order:

| Class | Asset Type |

|---|---|

| I | Cash and cash equivalents |

| II | Actively traded personal property (securities, foreign currency) |

| III | Mark-to-market assets and debt instruments |

| IV | Stock in trade, inventory, property held for sale |

| V | All tangible and intangible assets not in other classes (including machinery and equipment) |

| VI | Section 197 intangibles other than goodwill |

| VII | Goodwill and going-concern value |

The residual structure means that the more value supportably assigned to Class V assets, the less residual flows to Class VII (goodwill). Equipment and goodwill carry different depreciation and amortization schedules, and the allocation between them directly affects both parties' tax positions.

A buyer who can support a higher Class V allocation gains accelerated depreciation on tangible assets. A seller who agrees to a lower Class V allocation may be shifting value into goodwill, which changes the tax character of the gain.

The IRS requires that buyer and seller report consistent allocations on their respective Form 8594 filings. If the two filings conflict, the IRS may reallocate based on its own determination. A certified equipment appraisal by an independent, credentialed appraiser is the primary mechanism for establishing a mutually supportable Class V figure. Allocations backed by such an appraisal are substantially harder to challenge on audit than allocations agreed to solely between the parties without independent documentation.

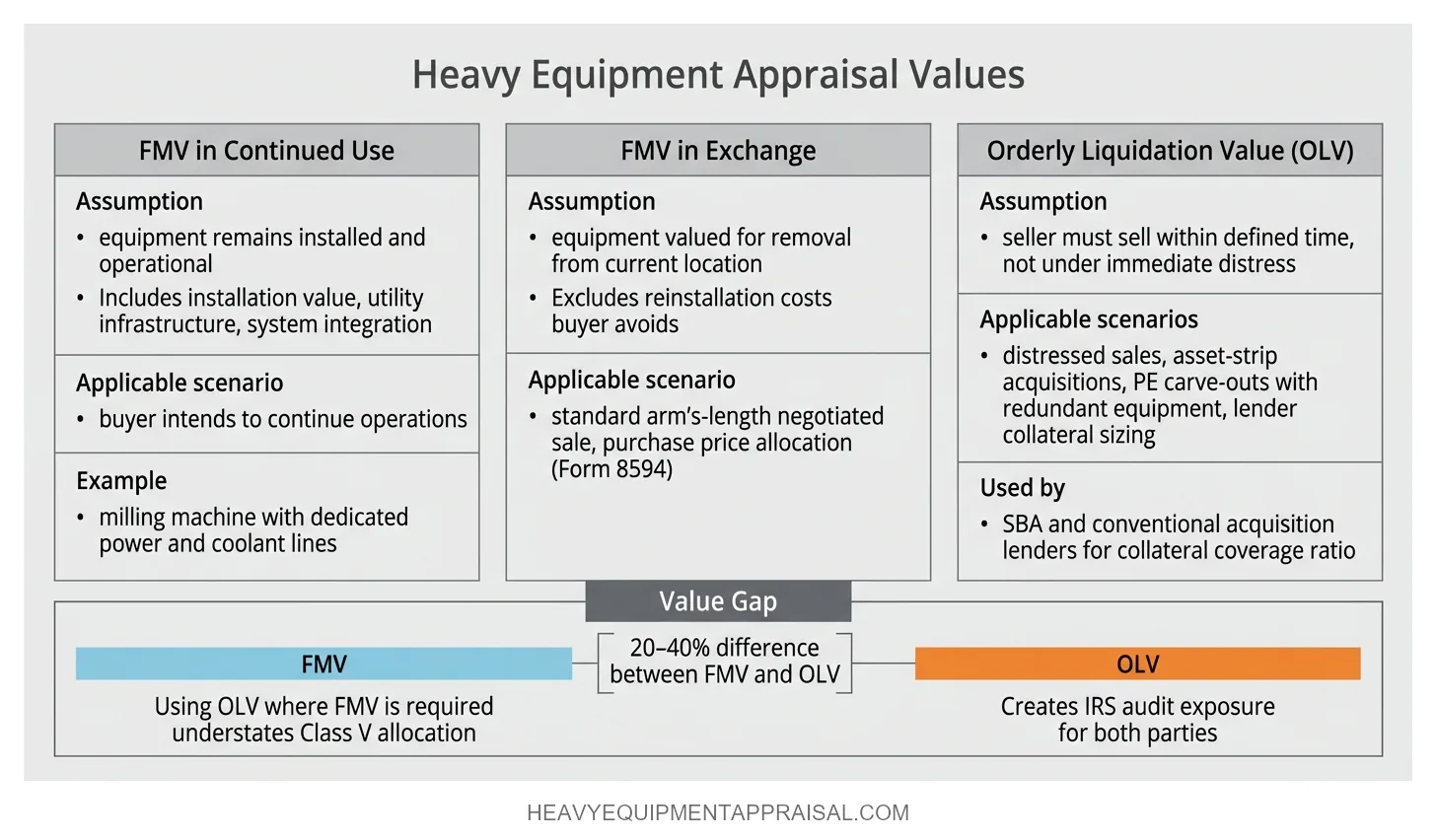

Which Value Standard Applies: Fair Market Value or Orderly Liquidation Value?

Fair market value is the correct standard for purchase price allocation and most M&A equipment appraisals. FMV assumes a hypothetical willing buyer and willing seller, neither under compulsion, both with reasonable knowledge of relevant facts. That assumption mirrors the arm's-length conditions of a negotiated business sale.

Within the FMV standard, the premise of value matters.

FMV in continued use assumes the equipment will remain installed and operational in the business. FMV in exchange assumes the equipment is valued for removal from its current location.

For an acquisition where the buyer intends to continue operations, FMV in continued use is the appropriate premise. It captures the installation value, utility infrastructure, and system integration that disappear the moment equipment is removed. A milling machine bolted to a production floor with dedicated power and coolant lines has measurably higher value in continued use than in exchange because the buyer avoids removal, transport, and reinstallation costs.

Orderly liquidation value (OLV) enters the picture in specific scenarios: distressed sales where the seller must liquidate, asset-strip acquisitions where the buyer plans to resell portions of the equipment portfolio, or private equity carve-outs with redundant equipment destined for disposal.

The distinction between FMV and OLV is not semantic. The same equipment can carry a 20–40% difference in reported value depending on which standard is applied. Using OLV where FMV is required understates the Class V allocation and distorts the entire purchase price allocation, creating exposure for both parties on audit.

When in the Deal Process to Order the Appraisal

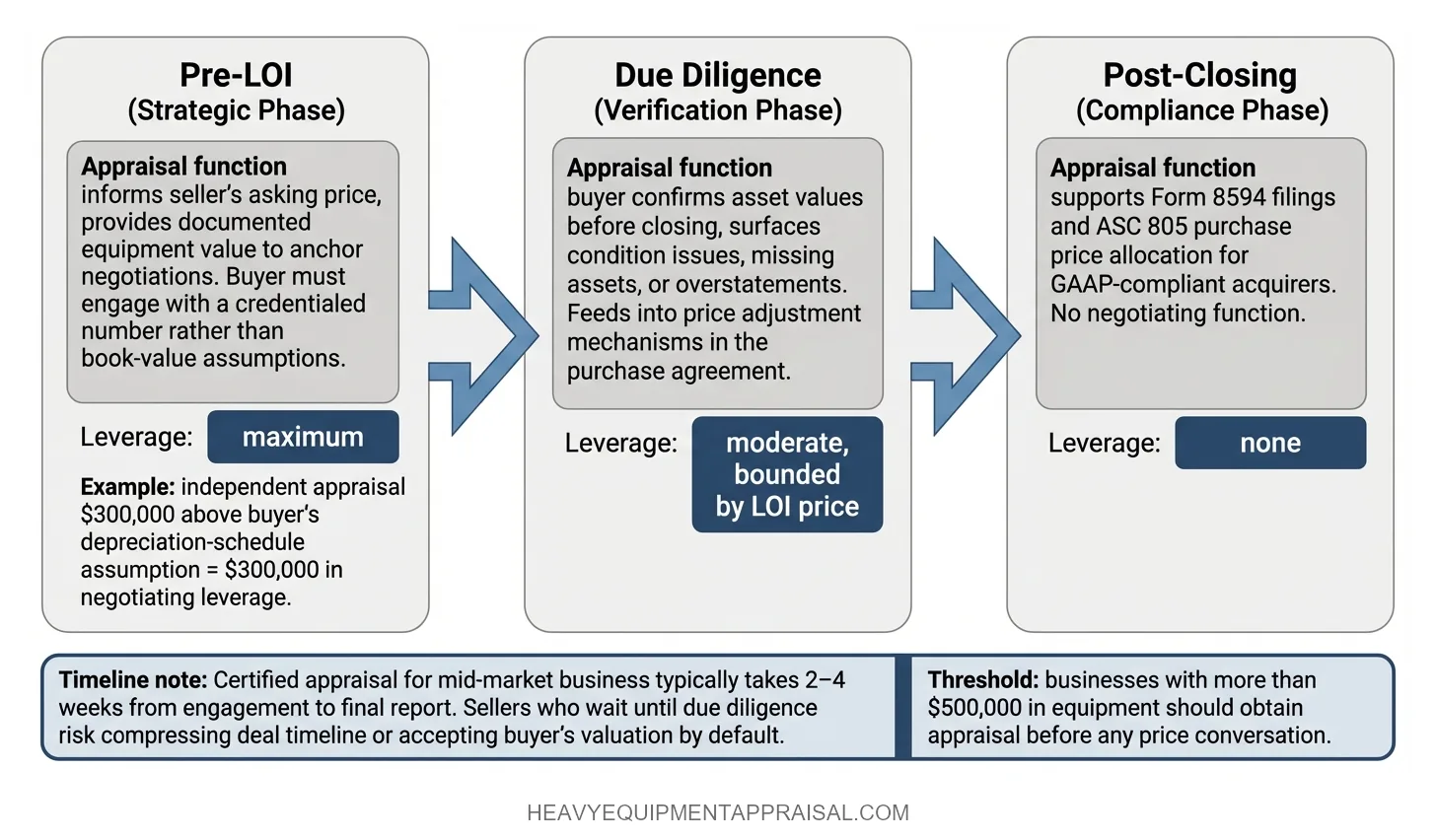

Equipment appraisals in a business sale should be ordered before a letter of intent (LOI) is finalized, not after the purchase price is agreed and not as a post-closing compliance exercise.

The distinction is strategic.

Before the LOI, an independent appraisal gives the seller a documented, credentialed asset value to anchor negotiations. The buyer must engage with a specific, well-supported number rather than relying on book-value assumptions or informal estimates.

After the LOI is signed, the purchase price is typically fixed (or narrowly bounded), and the appraisal becomes a confirmation exercise. It may document that the equipment is worth more than the agreed price, but the seller has already committed to a number and often faces a no-shop provision that prevents renegotiation.

Three deal stages carry distinct appraisal implications:

- Pre-LOI (strategic phase). The appraisal informs the seller's asking price and provides a factual basis for the equipment component. Maximum leverage.

- Due diligence (verification phase). The buyer orders an appraisal (or reviews the seller's) to confirm asset values before closing. The appraisal may surface condition issues, missing assets, or overstatements that affect the purchase price through adjustment mechanisms.

- Post-closing (compliance phase). The appraisal supports Form 8594 filings and, for GAAP-compliant acquirers, ASC 805 purchase price allocation. At this stage, the appraisal is purely a tax and accounting document with no negotiating function.

A certified equipment appraisal for a mid-market business typically takes 2 to 4 weeks from engagement to final report, depending on asset volume and site complexity. Sellers who wait until due diligence to engage an appraiser risk compressing the deal timeline or accepting the buyer's valuation by default.

What Buyers and Sellers Each Need From the Appraisal

Buyers and sellers have structurally different interests in equipment value within a transaction, and a single appraisal can serve both parties only if it is genuinely independent and uses the correct value standard.

The seller's interest centers on maximizing the supportable equipment value. A higher documented FMV justifies a higher asking price and shifts the purchase price allocation toward Class V assets, which may produce favorable tax treatment depending on the seller's basis and depreciation recapture exposure. The seller also needs the appraisal to be credible enough that the buyer's advisors accept it rather than ordering a competing report.

The buyer's interest is more layered. The buyer may want to allocate more value to equipment (Class V) to accelerate post-acquisition depreciation deductions. At the same time, the buyer's lender may require a separate appraisal using OLV for collateral purposes. In deals financed through SBA lending or conventional acquisition financing, the lender's collateral sizing is based on OLV, not FMV. This creates a dual-appraisal dynamic: one report at FMV for purchase price allocation and one at OLV for the lender's collateral coverage ratio.

An independent appraiser engaged by mutual agreement produces a report that neither party controls.

The appraiser's obligation is to the methodology and the standard of value, not to either party's negotiating position. This is why a single independent appraisal is generally preferable to dueling reports. If the buyer and seller each hire their own appraiser using the same value standard and the same effective date, the reports should converge within a reasonable range. When they diverge significantly, the divergence usually traces to different premises of value, different condition assessments, or different data sources, all of which are identifiable and resolvable.

Equipment Appraisal in Asset Sales vs. Stock Sales

Equipment appraisal is legally required for tax compliance in asset sales and is not required in pure stock sales, though exceptions make the distinction less clean than it appears.

Asset sale: The buyer acquires specific assets, not the entity's shares. IRC Section 1060 applies. Both parties file Form 8594. The buyer receives a stepped-up basis in the acquired assets equal to the allocated purchase price. Equipment appraisal is the mechanism for establishing the Class V allocation. The seller recognizes ordinary income on depreciation recapture under Section 1245, plus capital gains on any amount exceeding original cost.

Stock sale: The buyer acquires the entity's shares. Section 1060 does not apply. Form 8594 is not required. The underlying assets retain their existing tax basis, and the buyer does not receive a step-up. Equipment appraisal is not mandated for tax purposes.

However, three scenarios bring equipment appraisal back into stock sales.

First, when the purchase agreement includes representations and warranties regarding asset condition and value, the buyer may require an appraisal to verify those representations and establish a baseline for post-closing adjustment claims.

Second, when the acquirer is GAAP-compliant (public companies, private companies with GAAP-reporting lenders), ASC 805 (Business Combinations) requires fair value measurement of all identifiable tangible assets at the acquisition date, regardless of whether the deal was structured as a stock or asset purchase.

Third, and most consequentially, a Section 338(h)(10) election allows both parties to treat a stock sale as a deemed asset sale for tax purposes. When this election is made, Form 8594 is required and equipment appraisal becomes necessary. Section 338(h)(10) elections are common in private equity acquisitions of S-corporations.

Most small- and mid-market business sales are structured as asset sales. The equipment appraisal requirement applies broadly across that market segment.

How the Appraiser Establishes Value in an M&A Context

Equipment appraisers in M&A transactions rely primarily on the sales comparison approach and the cost approach, with method selection driven by available market data, equipment type, and the stated premise of value.

Sales comparison approach. The appraiser identifies recent transactions for comparable equipment (auction results, dealer sales, private transactions) and adjusts for differences in age, condition, configuration, and location. This is the preferred method when active secondary markets exist for the equipment class in question. Standard industrial equipment, construction machinery, transportation assets, and material-handling equipment typically have sufficient transaction data to support a sales comparison analysis.

Cost approach. When comparable sales data is thin or nonexistent, the appraiser calculates replacement cost new (RCN) and subtracts physical deterioration, functional obsolescence, and economic obsolescence. The result is replacement cost new less depreciation (RCNLD). This method is appropriate for custom-built machinery, specialized production lines, and recently manufactured equipment where the original cost is well documented. In M&A contexts, functional obsolescence is particularly relevant: aging equipment in the target company may require significant capital investment post-acquisition, and the cost approach quantifies that gap.

Income approach. This method is less common for individual equipment items but applies when specific assets generate isolable, documentable income streams. Fleet vehicles under lease contracts or revenue-producing production lines with identifiable cash flows are candidates. The methodology requires supportable capitalization or discount rates tied to the asset class.

For M&A transactions involving operating facilities, equipment is often appraised as a group rather than strictly unit by unit. An integrated production line may carry higher value as a functioning system than the sum of its individual components would suggest.

An appraiser applying FMV in continued use captures that system value.

An appraiser valuing the same equipment unit by unit on an exchange basis does not.

The premise of value and the grouping methodology must align with the transaction structure.

A lender, buyer, or IRS auditor reviewing the appraisal report will examine whether the chosen approach is appropriate for the equipment type and whether the methodology section justifies the selection with market evidence.

What Makes an Equipment Appraisal Hold Up in a Transaction

A rigorous M&A equipment appraisal is compliant with USPAP Standards 7 and 8, produced by a credentialed appraiser, and documented thoroughly enough to withstand review by the IRS, a lender, or opposing counsel.

USPAP Standard 7 governs the development of the appraisal. It requires the appraiser to identify the problem, determine the scope of work, and apply recognized methodology. Standard 8 governs reporting.

A compliant report must include:

- The clearly stated scope of work

- Identification of the property appraised

- The value standard applied (FMV, OLV, or ASC 820 fair value)

- The effective date

- A description of methodology with supporting market data

- A condition assessment

- Limiting conditions

- A signed USPAP certification statement

An appraisal that omits the USPAP certification is non-compliant by definition and vulnerable to challenge.

Credentials matter. An appraiser holding the American Society of Appraisers (ASA) designation, the Accredited Member of the Equipment Appraisers Association (AMEA), or the Certified Machinery and Equipment Appraiser (CMEA) designation has demonstrated competency through examination, experience requirements, and peer review.

Verifiable credentials and documented methodology are the two factors that most directly determine whether a report survives scrutiny.

The most common deficiency in M&A equipment appraisals is the use of book-value depreciation schedules as a proxy for market value.

An accountant's depreciation schedule reflects tax policy and GAAP conventions. It does not reflect condition, market demand, technological obsolescence, or installation value. A report built on book-value inputs rather than market evidence will not survive an IRS challenge, a lender's review, or a post-closing dispute between buyer and seller.

Deals stall or produce post-closing litigation when equipment appraisals lack independence, credentials, or methodological rigor. A USPAP-compliant report signed by a credentialed appraiser with documented market data is the standard that every other party in the transaction (attorneys, CPAs, lenders, and the IRS) expects to see.

FAQ

Is an equipment appraisal legally required when selling a business?

An equipment appraisal is not legally required when selling a business in most cases. Sellers use appraisals to establish fair market value, support negotiations, and satisfy lenders or buyers. Legal requirements arise only in specific situations such as SBA financing, tax reporting, or court-ordered valuations.

What IRS form requires equipment values to be reported in a business sale?

IRS Form 8594 requires equipment values to be reported in a business sale. Form 8594, Asset Acquisition Statement, allocates the total purchase price across asset classes, including machinery and equipment. Both buyer and seller must file this form with their tax returns in the year of sale.

What is the difference between FMV in continued use and orderly liquidation value for equipment?

The main difference between FMV in continued use and orderly liquidation value is that FMV in continued use assumes the equipment remains in operation, while orderly liquidation value assumes a planned sale over 60–180 days. FMV reflects higher value due to ongoing utility, while liquidation value reflects reduced pricing due to sale conditions.

When should a seller order an equipment appraisal during the deal process?

A seller should order an equipment appraisal before listing the business or during early negotiations, typically 30–90 days before going to market. Early appraisals establish accurate pricing, support buyer due diligence, and prevent delays during financing, especially in SBA-backed transactions.

Does a stock sale require an equipment appraisal?

A stock sale does not require an equipment appraisal because ownership transfers through shares, not individual assets. Buyers may still request an appraisal to assess asset value, support financing, or evaluate risk. Appraisals become common when lenders, investors, or internal due diligence require asset-level verification.

What triggers a Form 8594 filing requirement in a business acquisition?

A Form 8594 filing requirement is triggered when a business acquisition qualifies as an asset sale for tax purposes under IRC Section 1060. This applies when buyers acquire a group of assets that constitute a trade or business and allocate the purchase price across asset classes.

How does a Section 338(h)(10) election affect equipment appraisal requirements?

A Section 338(h)(10) election treats a stock sale as an asset sale for tax purposes, which triggers purchase price allocation under IRC Section 1060. This treatment increases the need for an equipment appraisal to support fair market value, IRS Form 8594 reporting, and buyer depreciation schedules.

What credentials should an equipment appraiser have for an M&A transaction?

An equipment appraiser for an M&A transaction should hold recognized machinery valuation credentials such as ASA, CMEA, or AM. ASA stands for Accredited Senior Appraiser. CMEA stands for Certified Machinery and Equipment Appraiser. Appraisers should follow USPAP standards, have 5–10 years of valuation experience, and show direct expertise in purchase price allocation, fair market value, and equipment appraisals used in transactions.

What is the difference between a Class V and Class VII asset allocation under IRC Section 1060?

The main difference between Class V and Class VII asset allocation under IRC Section 1060 is that Class V includes tangible personal property such as equipment and machinery, while Class VII includes goodwill and going concern value. Class V assets depreciate over defined schedules, while Class VII assets amortize over 15 years.