Forced Liquidation Value Equipment Appraisal

Forced liquidation value (FLV) in equipment appraisal estimates the price of equipment sold quickly under compulsion, typically within 1–30 days. FLV assumes limited marketing, restricted buyer pools, and urgent sale conditions. This method produces the lowest value among appraisal types due to time pressure and reduced negotiation.

Forced liquidation value (FLV) is the most probable price a piece of equipment will bring when sold immediately, under compulsion, with no reasonable marketing period. FLV assumes the seller cannot wait, the buyer pool is limited to whoever shows up, and the transaction happens under conditions that favor the buyer.

Bankruptcy trustees, lenders modeling default scenarios, and court-appointed receivers rely on FLV because it reflects the actual recovery floor when time and leverage have been removed from the equation.

What Forced Liquidation Value Means

FLV assumes a seller who cannot wait and a market that knows it. 2 core assumptions define the standard: there is no meaningful marketing period, and the seller is under extreme compulsion to sell.

Both conditions must be present.

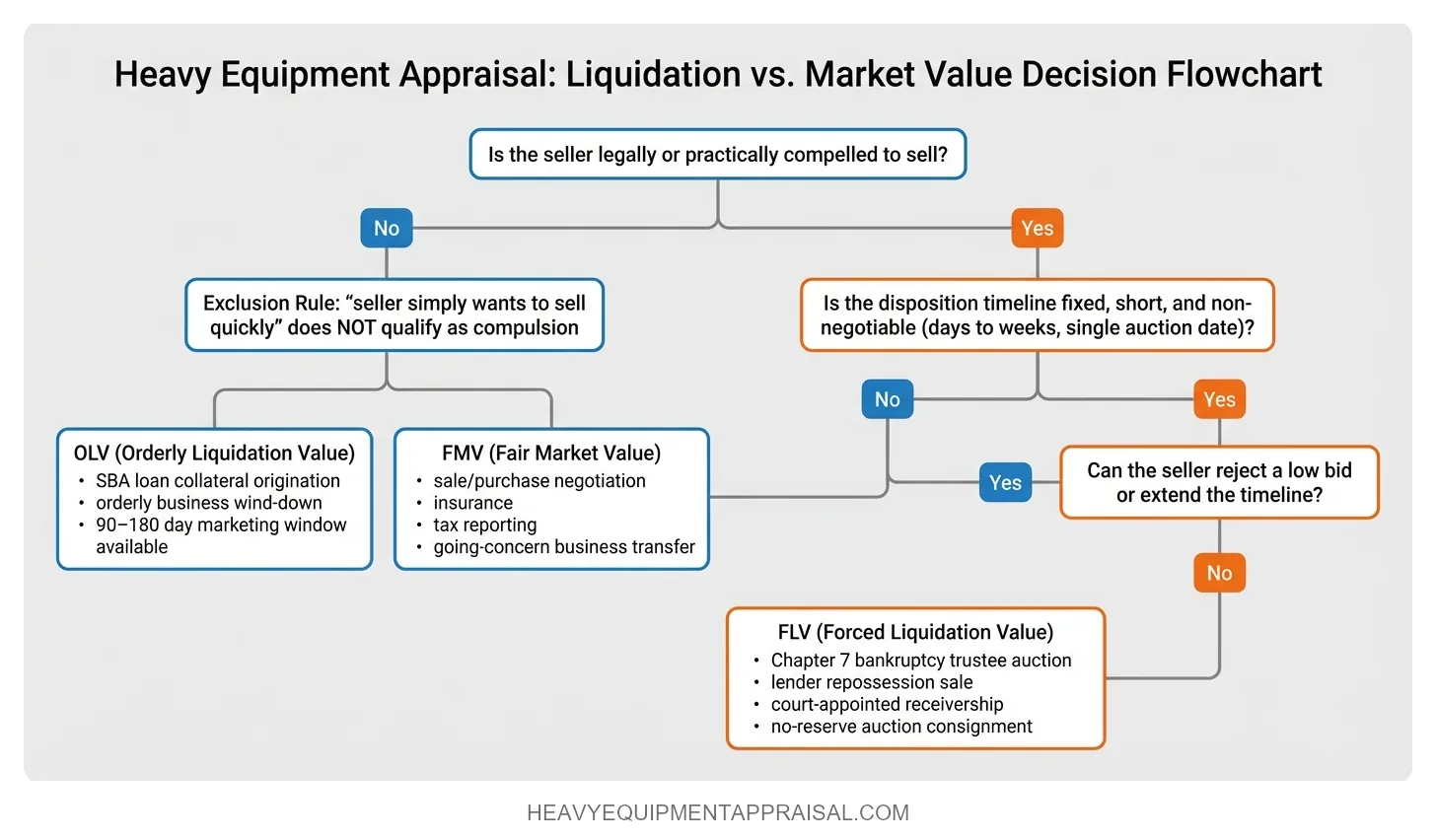

A seller who merely wants to sell quickly is not in a forced liquidation scenario. A seller who must sell by a court-ordered deadline, with no ability to reject a low bid, is.

Time compression changes the buyer pool fundamentally. When equipment goes to auction without a reserve price on a fixed date, the universe of potential buyers shrinks to cash-ready participants: dealers looking to flip, contractors hunting opportunistic adds, and professional auction buyers who make a living absorbing risk.

The retail end-user who would pay fair market value (FMV) after a 90-day search is absent from this pool. The remaining buyers know the seller’s constraints and price accordingly.

“Unfavorable market conditions” is not a vague qualifier, it refers to concrete realities:

- Seasonal oversupply (construction equipment liquidated in winter when contractors are not buying)

- Regional economic depression (oilfield equipment sold during a drilling downturn)

- The stigma of distressed assets (buyers assume undisclosed problems and discount preemptively)

These conditions are not hypothetical. They are documented in auction results every week.

FLV is a recognized premise of value in the appraisal profession, not a flaw or a penalty applied to a “real” number. It reflects a real transaction scenario with its own probability distribution, its own buyer pool, and its own market dynamics.

An FLV appraisal that is well-supported by distressed-sale comparable data is as methodologically rigorous as any FMV appraisal.

How FLV Differs from OLV and FMV

FLV returns the lowest of the 3 primary value standards because it compresses both the seller’s leverage and the available buyer pool to their minimum. The differences between FLV, orderly liquidation value (OLV), and fair market value (FMV) are not matters of degree. They reflect fundamentally different transaction scenarios with different assumptions about time, compulsion, and market access.

| Factor | FMV | OLV | FLV |

|---|---|---|---|

| Key Assumption | Willing buyer, willing seller, no compulsion | Seller obligated to sell, reasonable time allowed | Seller under extreme compulsion, no marketing period |

| Time Horizon | No artificial constraint | Weeks to months (typically 90–180 days) | Days to weeks, often a single auction date |

| Buyer Pool | Full market: end users, dealers, investors | Narrowed: dealers, opportunistic buyers, some end users | Minimal: cash buyers, auction flippers, dealers only |

| Typical Use Case | Sale/purchase negotiations, insurance, tax reporting | SBA loan collateral, orderly business wind-down | Bankruptcy, repossession, foreclosure, no-reserve auction |

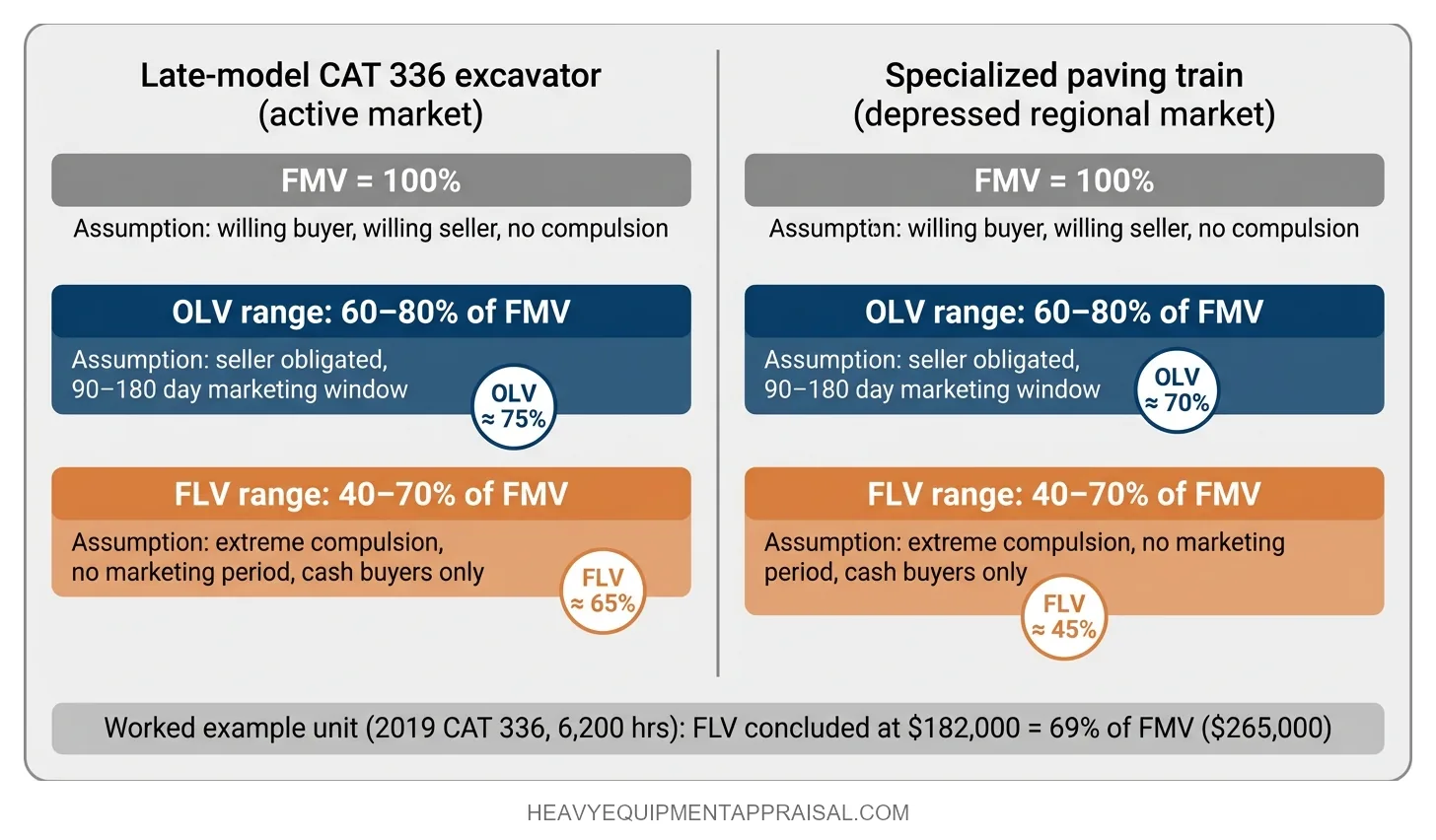

| Typical Range (vs. FMV) | Baseline (100%) | 60–80% of FMV | 40–70% of FMV |

These ranges are practitioner estimates for heavy construction equipment under normal-to-soft market conditions.

They are not universal rules.

High-demand commodity equipment (skid steers, backhoe loaders) in active markets sees FLV closer to the top of the range. Specialized or aged equipment in depressed regional markets can fall below the bottom.

The gap between OLV and FLV is often smaller than people expect for equipment with deep secondary markets. A late-model Caterpillar 336 excavator might appraise at 75% of FMV under OLV conditions and 65% under FLV conditions because dealer demand creates a floor.

A specialized paving train in a region with no active highway projects might appraise at 70% of FMV under OLV and 45% under FLV because the buyer pool for that asset collapses without a marketing period. For the full analysis of when each standard applies, see comparing all three value standards.

When FLV Is the Right Value Standard

FLV is the appropriate value standard when the disposition timeline is fixed, short, and non-negotiable. It is not the correct standard when a seller simply wants to move equipment fast. The distinction is compulsion: FLV applies when the seller has no legal or practical ability to wait for a better price.

Bankruptcy proceedings are the most common FLV scenario. In a Chapter 7 liquidation, the bankruptcy trustee must convert assets to cash for creditor distribution within a court-imposed timeline. FLV reflects what the estate will actually recover under that constraint. FLV is not mandated by the Bankruptcy Code by name. The trustee selects the value standard that matches the actual disposition scenario. When that scenario is a court-ordered auction on a fixed date, FLV is the appropriate standard.

Lender repossession and foreclosure generate the 2nd-largest category of FLV appraisals. When a borrower defaults, the lender’s recovery depends on what the collateral brings in an expedited sale. SBA lender collateral standards require OLV for origination underwriting, not FLV. FLV is the lender’s backstop: the number that answers “what do we recover if we have to repossess and auction this equipment next month?”

Court-appointed receivership imposes defined legal constraints on asset disposition. A receiver has fiduciary obligations to creditors and a court timeline to meet. FLV provides the defensible floor the receiver reports to the court.

Auction consignment without reserve is FLV in execution, whether or not anyone labels it that way. When equipment goes to auction with no reserve price, the seller has surrendered the ability to reject a disappointing bid. The resulting price is the market’s answer to the FLV question.

FLV is not the right standard when the seller has time to market properly (OLV or FMV applies), when the sale is part of a going-concern business transfer (FMV in continued use applies), or when a lender is sizing collateral for a new loan under normal conditions (OLV is the commercial and SBA standard).

Choosing the wrong value standard does not just produce the wrong number. It produces a report that fails to serve the intended use.

How Appraisers Determine FLV

FLV is derived from actual auction and distressed-sale transaction data, not from discounting FMV by a fixed percentage. The primary method is the sales comparison approach, applied with a critical filter: comparable sales must come from distressed-transaction channels.

General market sales (private party, brokered, dealer retail) are not valid FLV comparables because they reflect different seller leverage, marketing exposure, and buyer motivation.

Distressed-sale data sources include public auction results from Ritchie Bros. Auctioneers, IronPlanet, and Purple Wave, as well as receiver-managed disposition records, repossession sale results, and dealer liquidation purchase histories. The appraiser filters for transactions where the seller was under compulsion and the marketing period was absent or severely compressed.

A Caterpillar D6 dozer that sold at a Ritchie Bros. no-reserve auction is an FLV comparable. The same model sold through a dealer listing after 60 days on the market is not.

Applying a fixed percentage discount to FMV to arrive at FLV is not a valid appraisal methodology. This approach assumes a stable, universal relationship between FMV and FLV that does not exist. It ignores equipment-specific factors (condition, hours, model demand), market-cycle factors (buyer availability, seasonal patterns), and equipment-type factors (commodity versus specialized).

Federal lending standards confirm this: USDA Farm Service Agency appraisal guidelines explicitly require “comparables from other forced liquidation sales” as the evidentiary basis, not derived discounts from other value standards.

Worked Mini-Example: FLV for a 2019 Caterpillar 336 Excavator

A bankruptcy trustee needs an FLV appraisal for a 2019 CAT 336 excavator with 6,200 hours, located in the Southeast U.S. The court-ordered auction date is 21 days away.

Step 1: Identify distressed-sale comparables. The appraiser pulls 4 no-reserve auction results for 2018–2020 CAT 336 units sold in the past 12 months with 5,000–8,000 hours:

| Sale | Year/Hours | Auction House | Sale Price |

|---|---|---|---|

| Comp A | 2019 / 5,800 hrs | Ritchie Bros. | $185,000 |

| Comp B | 2020 / 6,500 hrs | Ritchie Bros. | $192,000 |

| Comp C | 2018 / 7,200 hrs | IronPlanet | $168,000 |

| Comp D | 2019 / 5,400 hrs | Purple Wave | $179,000 |

Step 2: Adjust for differences. The appraiser adjusts each comparable for year, hours, attachments, and condition. Comp C is adjusted upward by $8,000 for its older model year and higher hours. Comp D is adjusted downward by $4,000 for lower hours. Adjusted range: $175,000–$192,000.

Step 3: Reconcile to a value conclusion. The subject unit’s 6,200 hours and documented condition place it mid-range. The appraiser concludes an FLV of $182,000.

Step 4: Cross-check against FMV and OLV. Dealer retail listings for comparable units show FMV of approximately $265,000. The FLV of $182,000 represents roughly 69% of FMV, consistent with a late-model commodity excavator in an active secondary market. OLV for the same unit would likely fall near $210,000–$220,000 (about 80% of FMV), confirming the FLV sits appropriately below the orderly liquidation range.

This example illustrates why comp-based FLV is more defensible than a percentage haircut. If the appraiser had simply applied a generic 35% discount to FMV, the result would have been $172,000, understating recovery by $10,000 and potentially harming creditors.

Equipment condition interacts with FLV asymmetrically. In a distressed sale, poor condition is penalized more severely than in an orderly or open-market transaction because as-is, where-is terms shift all repair and uncertainty risk to the buyer. High-hour machines lose the ability to offset hours with verifiable maintenance records, which are often unavailable in forced dispositions. Late-model, well-maintained equipment in high-demand categories narrows the FLV-to-FMV gap because dealer demand provides a predictable acquisition floor.

USPAP reporting requirements mandate that the appraiser explicitly identify the type and definition of value, the premise of value, and the specific assumptions supporting the conclusion.

An FLV report must state that forced liquidation is the premise, define what that means in the assignment’s context (time horizon, assumed market conditions, transaction structure), and disclose any extraordinary assumptions.

A report that states a value without identifying the premise is non-compliant and can be rejected by lenders or challenged in court. FLV appraisals used in legal or lending contexts require a certified equipment appraiser to ensure both methodological rigor and report defensibility.

What FLV Means for the Parties Involved

FLV tells each party in a distressed transaction something different, and confusing those meanings leads to costly errors.

Lenders use FLV as the collateral coverage number in a default scenario. If FLV does not cover the outstanding loan balance, the position is undercollateralized on a worst-case basis. Most commercial lenders size collateral to OLV for origination and reserve FLV for stress-testing and workout analysis. When a lender orders an FLV appraisal during origination (not workout), it signals the credit committee is already skeptical about the borrower's ability to perform.

Borrowers and equipment owners receive FLV as the lowest number they will encounter in the appraisal process. The gap between FLV and FMV represents recoverable value, but recovering it requires time and marketing that a forced disposition does not allow. For an equipment owner facing financial pressure, the FLV number quantifies the cost of running out of time. Every week of additional marketing window can move the recovery from FLV toward OLV.

Attorneys and trustees rely on FLV as a legally defensible floor for asset distribution calculations in insolvency proceedings. Courts accept FLV when the report is produced by a credentialed appraiser, complies with USPAP, and explicitly defines the forced liquidation assumptions. An opposing expert can challenge a poorly documented FLV conclusion on methodology grounds.

Buyers at forced-sale auctions are acquiring at or near FLV, and the discount they receive is not free money. It is compensation for absorbing risk: unknown condition behind the cosmetics, no warranty, no recourse, potential title complications, and the cost of transport and reconditioning. The structural reason FLV is lower than OLV for identical equipment is that the buyer's risk premium in a forced sale is higher, and the auction format transfers that premium entirely to the seller's side of the ledger.

The Practical Weight of FLV

FLV is not a theoretical floor, it is the number that governs real outcomes in bankruptcy courts, lender workouts, and auction houses. The difference between FLV and FMV is not lost value. It is value that requires time, marketing, and disposition strategy to access.

Parties who understand that gap can make informed decisions: negotiate more time, pursue a structured wind-down instead of a fire sale, or accept the FLV outcome with clear eyes on the recovery. Parties who do not understand it leave recoverable dollars on the table.

For a detailed analysis of when each value standard applies and how the gaps between them affect real decisions, see comparing FMV, OLV, and FLV.