Fair Market Value Equipment Appraisal: Definition, Requirements, and When It Applies

Fair market value (FMV) is the price at which equipment would change hands between a willing buyer and a willing seller, neither under compulsion, both with reasonable knowledge of relevant facts.

The IRS, SBA lenders, courts, and credentialed appraisal organizations all treat FMV as the controlling standard for tax, legal, and many transactional purposes. FMV assumes conditions that may not exist in the actual transaction being appraised, and applying it when those conditions are absent produces a number that will not survive regulatory review or legal challenge.

What Fair Market Value Means in Equipment Appraisal

Fair market value is a hypothetical construct, not a market observation. The definition originates from IRS Revenue Ruling 59-60:

The price property would command in an open, competitive market between a willing buyer and willing seller, with no compulsion on either party and both possessing reasonable knowledge of relevant facts.

The American Society of Appraisers (ASA) uses identical language and adds that FMV assumes payment in cash or cash equivalent.

The critical word is “hypothetical.”

An FMV opinion does not describe what a specific buyer would pay or what a specific seller would accept. It describes what an open market transaction would produce under idealized conditions. This makes FMV a legal and economic standard rather than a price prediction.

FMV also carries a premise distinction that most published definitions omit. FMV in continued use values equipment as installed, operational, and part of a going concern. FMV in exchange values the same equipment as moveable property the buyer must remove.

For installed process equipment or manufacturing lines with significant installation value, the difference between these 2 premises can be substantial. An appraisal report that states “fair market value” without specifying the premise leaves ambiguity that a reviewer, lender, or opposing expert can exploit.

A lender or attorney relying on an FMV opinion needs confirmation that the appraiser selected the correct premise and that the assumptions embedded in the definition actually fit the assignment’s context. If they do not, FMV is the wrong standard and a different value type applies.

When Fair Market Value Is the Required Standard

FMV is not always the appropriate value type for equipment, but several high-stakes contexts require it by regulation or statute.

1. IRS and Tax Purposes

The IRS requires FMV for charitable donations of equipment, estate tax, and gift tax valuations. IRC Section 170(f)(11) and IRS Notice 2006-96 impose specific requirements for equipment donations: the taxpayer must obtain a “qualified appraisal” from a “qualified appraiser” who holds a designation from a recognized professional organization (ASA or equivalent) or meets minimum education and experience thresholds.

The appraisal must be completed no earlier than 60 days before the donation and no later than the tax return due date. A report that fails these requirements does not reduce the deduction, it disqualifies it entirely.

2. Estate Settlement and Divorce

Courts require FMV for equitable distribution of equipment assets in divorce proceedings and for estate tax valuations under IRC Sections 2031 and 2512. Expert testimony on equipment FMV must be defensible under Daubert standards in federal court, which means the methodology must be reliable, peer-reviewed, and applied consistently.

An estate and divorce appraisal that cites a reference guide value without applying professional methodology will not survive a Daubert challenge.

3. M&A and Business Sale

Purchase price allocation under ASC 805 requires valuation of identifiable assets. A distinction matters here: ASC 805 applies “fair value” as defined under ASC 820, which is not the same as fair market value. Fair value under ASC 820 is an exit price using market participant assumptions.

FMV is a hypothetical transaction price between a willing buyer and willing seller. In practice, the concluded numbers for tangible equipment are often close, but a report that labels an ASC 820 analysis as “fair market value” (or vice versa) has a definitional error that creates audit exposure.

Appraisers handling M&A equipment valuations often prepare dual-purpose reports or explicitly state which standard applies.

4. SBA Loans

SBA SOP 50 10 references FMV for business acquisition transactions under the 7(a) and 504 programs. For collateral sizing, however, SBA equipment appraisal requirements typically call for orderly liquidation value (OLV) because the lender is estimating recovery under a default scenario.

The distinction is consequential: FMV for transaction value, OLV for collateral coverage. Using FMV to size collateral overstates what the lender would recover in liquidation.

The Assumptions Behind FMV and Why They Matter

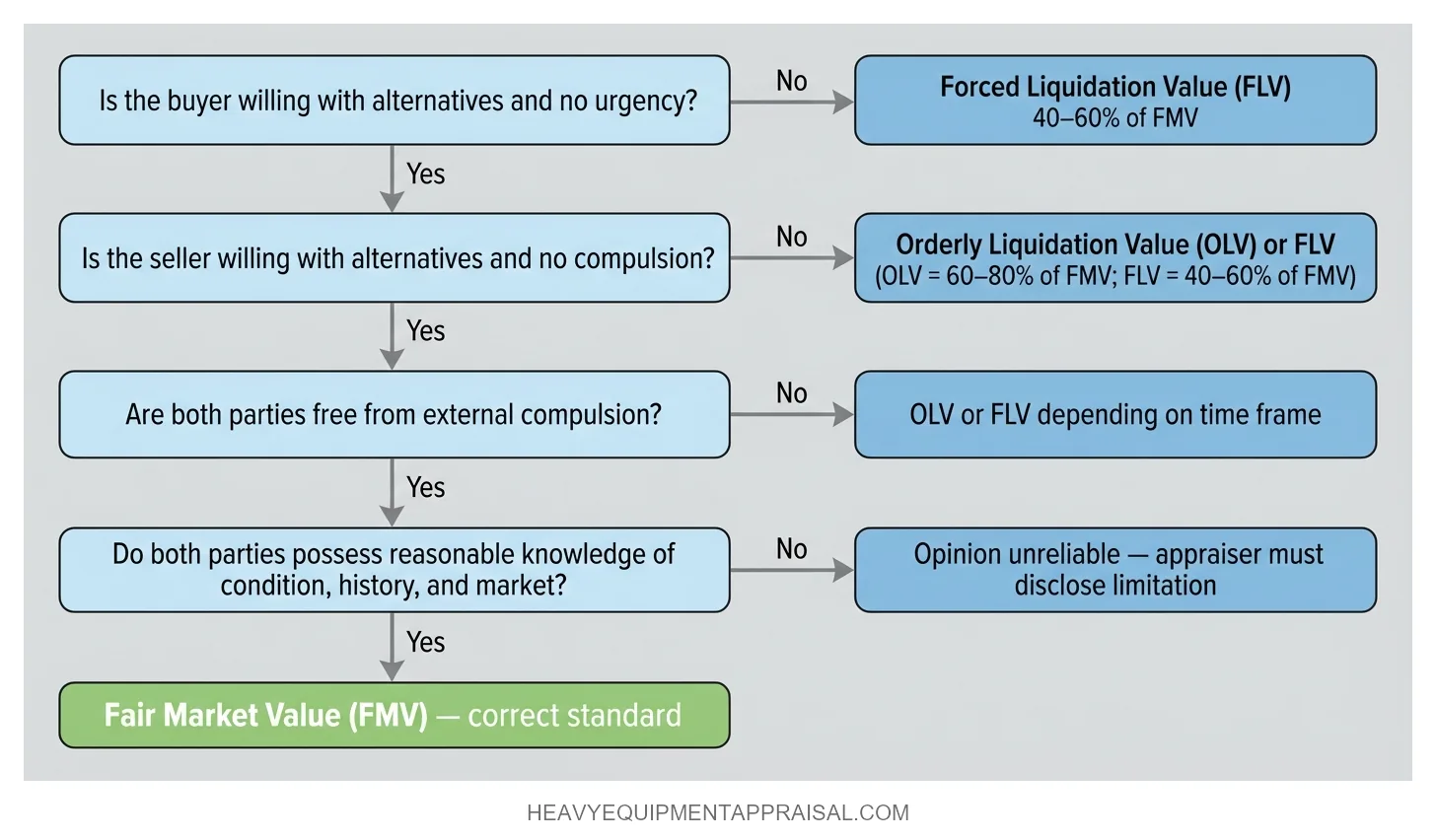

Every FMV opinion rests on 4 assumptions. When any assumption fails, FMV is no longer the appropriate standard, and a different value type describes the actual market conditions.

| FMV Assumption | What It Requires | What Breaks When It Fails | Resulting Value Type |

|---|---|---|---|

| Willing buyer | Buyer has alternatives, no urgency | Buyer has leverage over a distressed seller | Forced liquidation value (FLV) |

| Willing seller | Seller has alternatives, no compulsion | Court-ordered sale, bankruptcy, loan default | Orderly liquidation value (OLV) or FLV |

| Neither under compulsion | Both parties transact freely | Either party is compelled by external pressure | OLV or FLV depending on time frame |

| Reasonable knowledge | Both parties understand condition, history, market | Asymmetric information, concealed defects, limited inspection | Opinion becomes unreliable. The appraiser must disclose the limitation |

The practical spread between value types is equipment-dependent and market-dependent, but general ranges are instructive.

OLV typically returns 60–80% of FMV for construction and industrial equipment in normal market conditions. FLV runs lower, often 40–60% of FMV.

These are not fixed ratios. They shift with equipment type, age, condition, and current demand. The full comparison of these standards is covered at FMV vs. OLV vs. FLV.

The implication for any party relying on an FMV opinion: if the actual transaction or disposition will occur under conditions that violate 1 or more of these assumptions, FMV overstates the realizable price. Using FMV where OLV or FLV applies is not conservative. It is wrong.

How Appraisers Determine Fair Market Value for Equipment

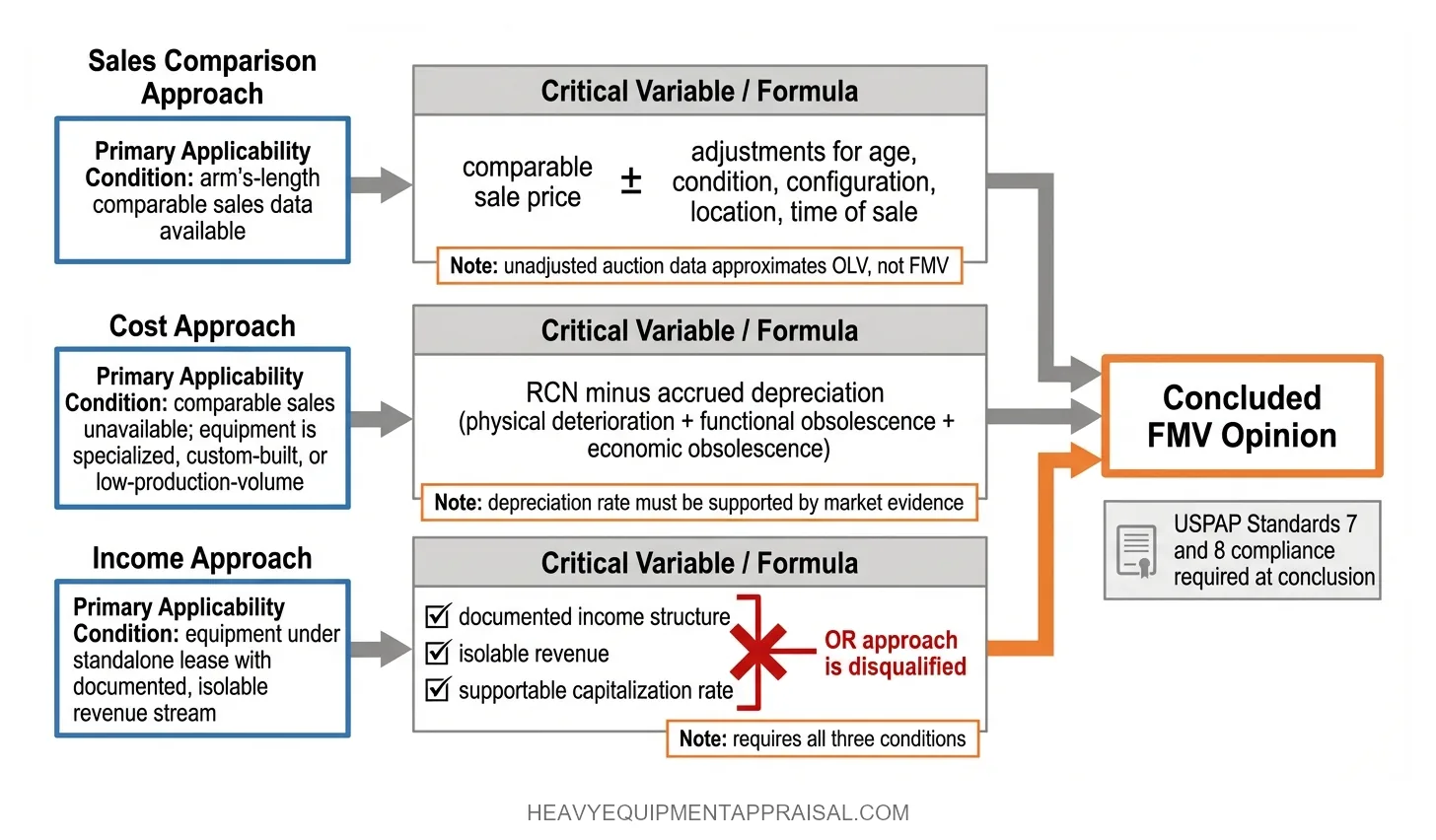

FMV for equipment is derived using 1 or more of 3 recognized methodologies. The methodology selected determines both the accuracy and the defensibility of the concluded value.

Sales comparison approach. This is the most credible methodology for FMV because it directly reflects market behavior. The appraiser identifies comparable equipment that has sold in arm's-length transactions and adjusts for differences in age, condition, configuration, location, and time of sale.

Data sources include auction results, dealer transaction records, and published price guides. One critical nuance: raw auction data reflects a compelled-seller environment.

Using unadjusted auction prices as FMV evidence produces a number closer to OLV than FMV. An appraiser must document adjustments that account for the difference between auction conditions and the open-market conditions FMV assumes. The full methodology is detailed at sales comparison approach.

Cost approach. Used when comparable sales data is unavailable, which is common for specialized, custom-built, or low-production-volume equipment.

The formula is replacement cost new (RCN) minus accrued depreciation for physical deterioration, functional obsolescence, and economic obsolescence. Credibility depends entirely on the depreciation analysis.

An appraiser applying a 40% depreciation rate to 10-year-old equipment without supporting that rate with market evidence has an assumption that an opposing expert or IRS reviewer can dismantle. The cost approach page covers the methodology in full.

Income approach. Rarely applicable to individual equipment items because most equipment does not generate identifiable, separable revenue independent of the business operation.

The exception is equipment under a standalone lease with documented income streams.

When the income structure is documented, the revenue stream is isolable, and the capitalization rate is supportable, direct capitalization or discounted cash flow analysis can produce a credible FMV. Without all 3 of those conditions, the income approach will not survive review.

What separates a credible FMV opinion from a reference-guide estimate is the combination of a USPAP-compliant report, a credentialed appraiser, and a methodology that can be defended under cross-examination or IRS audit.

Fair Market Value vs. Book Value, Blue Book, and Assessed Value

FMV is routinely confused with 3 other numbers that appear in financial records and reference tools. Each confusion produces a different kind of error.

Book value is an accounting construct. It reflects purchase price minus accumulated depreciation under a MACRS or straight-line schedule. It measures the tax or accounting treatment of the asset, not its market reality. A 2015 Cat 320 excavator fully depreciated on a 5-year MACRS schedule carries a book value of $0 by 2020. Its FMV may be $80,000–$120,000. Using book value as a proxy for FMV in a donation, estate, or divorce context produces a materially wrong number in either direction.

Assessed value is set by a taxing authority using mass appraisal methods calibrated for property tax purposes. Many jurisdictions assess personal property at a percentage of FMV, not at FMV itself. The assessment formula may lag market conditions by years. It is not an FMV opinion.

Blue Book and reference guide values (Equipment Watch, Rouse, Sandhills) provide market estimates based on aggregated listing and auction data. They are useful as a starting point for comparable analysis. They are not a concluded FMV. They do not account for specific condition, specific configuration, specific location, or actual transaction context.

A Blue Book estimate is not a substitute for a certified appraisal in any legal, tax, or lending context, and submitting one as such creates audit exposure or documentation deficiency.

USPAP Compliance and Fair Market Value Reporting

A defensible FMV opinion for equipment must comply with USPAP Standards 7 and 8, which govern personal property appraisal development and reporting. A report that omits required elements can be rejected on technical grounds before anyone evaluates the substance of the value conclusion.

A compliant FMV appraisal report must include:

- Identification of the client and intended users

- Statement of intended use

- The standard of value defined as used (fair market value, with the specific premise stated)

- The effective date of value

- Description of the subject property sufficient to identify it

- Scope of work performed (inspection method, data sources, methodology)

- Statement and rationale for approach(es) used and not used

- The appraiser's USPAP certification

- Statement of the appraiser's qualifications and competency

For charitable contribution deductions, IRS Notice 2006-96 imposes additional requirements: the date of contribution, the appraisal fee arrangement (contingent fees are prohibited), the appraiser's TIN, and a declaration that the appraisal was prepared for income tax purposes. An appraiser charging a fee based on the appraised value is disqualified under both USPAP ethics rules and IRS standards.

The consequences of non-compliance are binary, not graduated. The IRS can disallow an entire charitable deduction. An SBA lender can reject the report outright. A court can exclude the expert opinion under Daubert. Full USPAP compliance requirements are detailed on the standards page.

Getting FMV Right

FMV is not a generic label for "what the equipment is worth."

It is a legally defined standard with specific assumptions, specific methodology requirements, and specific reporting obligations. An opinion that misuses the term, applies the wrong premise, uses unsupported methodology, or omits required report elements is not an FMV appraisal. It is an unsupported estimate that creates liability for the party relying on it.

The starting point is confirming that the appraiser holds recognized credentials, understands the distinction between FMV and adjacent value types, and produces a report that meets the requirements of the context in which it will be used. Verifying appraiser qualifications before engagement, not after delivery, eliminates the most common source of FMV appraisal failure.