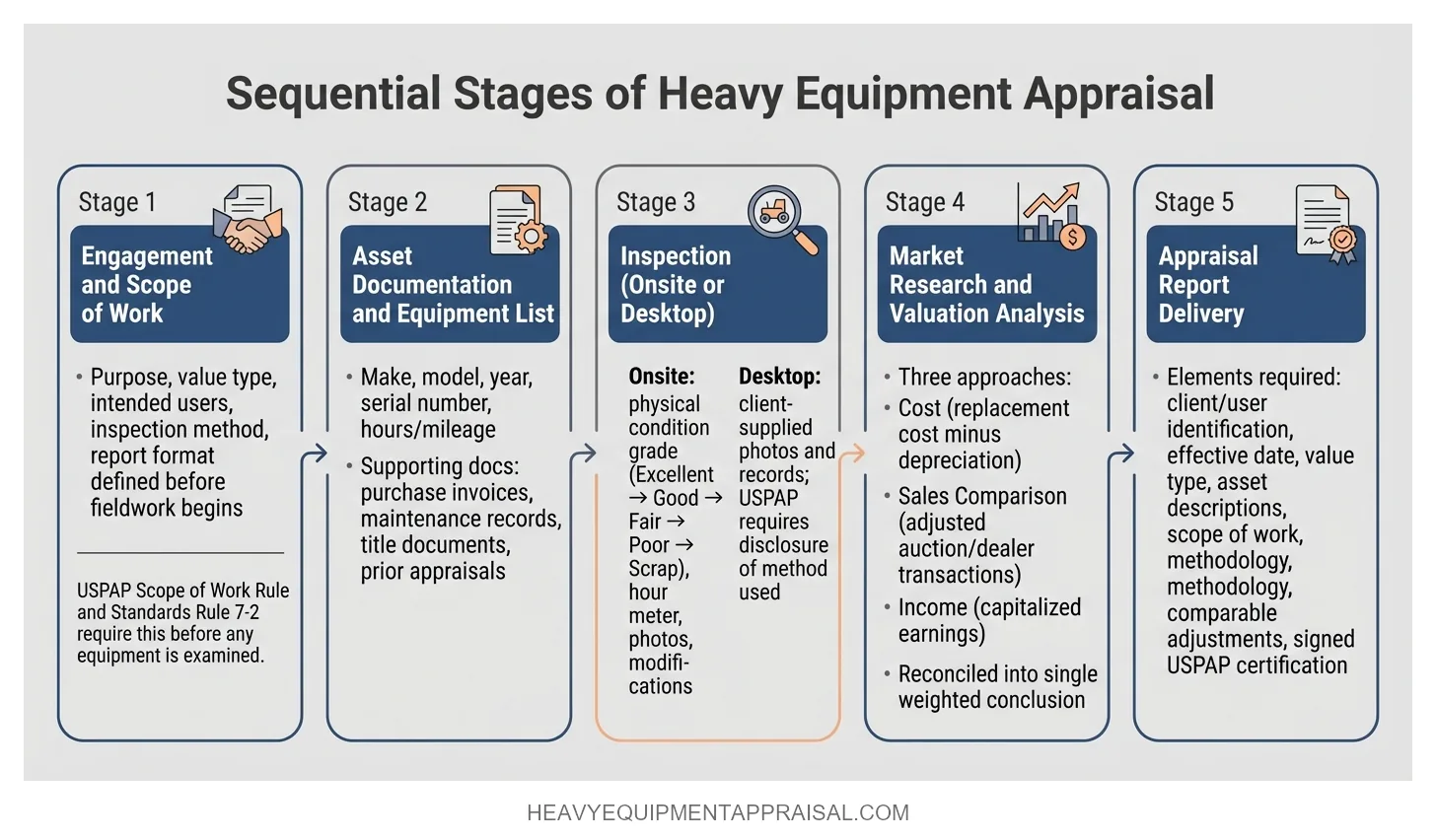

Equipment Appraisal Process (Step-by-Step)

A certified equipment appraisal follows five defined stages:

- Engagement and scope of work

- Asset documentation

- Inspection

- Valuation analysis

- Report delivery

Lenders, attorneys, and business owners all depend on this sequence producing a defensible value conclusion. USPAP requires the scope of work to be established before any fieldwork begins, a structural requirement that governs every decision in the process and one most guides fail to mention.

Step 1: Engagement and Scope of Work

Every equipment appraisal begins with a formal scope-of-work agreement that defines the assignment’s purpose, value type, intended use, intended users, inspection method, and report format before any equipment is examined.

USPAP’s Scope of Work Rule and Standards Rule 7-2 (governing personal property appraisal development) make this a compliance requirement, not a scheduling formality. An appraiser who begins fieldwork without a defined scope is operating outside professional standards.

The scope-of-work agreement governs every downstream decision.

It determines which value type the appraiser will conclude: fair market value for a business sale, orderly liquidation value for SBA loan collateral, or forced liquidation value for a bankruptcy filing. Starting with the wrong value definition does not produce a conservative or aggressive number. It produces a wrong number, one that a lender will reject or a court will exclude.

At engagement, the appraiser identifies the client, all intended users (the lender, an attorney, the IRS), and the intended use of the report. These identifications are not administrative. A report prepared for internal planning cannot be repurposed for SBA financing without a new scope-of-work agreement and a new appraisal. The effective date of value is also established here, because equipment values shift with market conditions, and a report dated six months after the transaction it supports loses defensibility.

The engagement letter also specifies the deliverable format.

A restricted appraisal report may suffice for an internal asset review, but most lenders and courts require a full appraisal report under USPAP standards. Choosing the wrong format at engagement means the final deliverable fails at the point of use, after the work and cost are already incurred.

Clients sometimes request a scope change mid-engagement, such as shifting from fair market value to orderly liquidation value after learning the intended lender’s requirements. This is allowable, but it requires a revised scope-of-work agreement. The original scope governs the original deliverable. A clearly defined engagement protects both the client’s investment and the report’s admissibility wherever it needs to stand up to scrutiny.

Asset Documentation and Equipment List

Before inspection begins, the appraiser needs a documented asset list containing the make, model, year, serial number, and current hours or mileage for each piece of equipment in the assignment. This list is the foundation of every subsequent step. Without it, the appraiser spends billable inspection time identifying assets that the client could have documented in advance, and the resulting report carries wider value ranges to account for unverified data.

The asset list alone is not sufficient. Supporting documents sharpen the appraisal’s precision. Purchase invoices establish original cost and acquisition date, both of which feed the cost approach. Maintenance records demonstrate whether a machine has been kept to OEM specifications or deferred into accelerated wear. Title documents confirm ownership and lien status. Prior appraisals provide historical value benchmarks that help the appraiser identify trends or anomalies. Each document reduces the number of assumptions the appraiser must make, and fewer assumptions produce tighter value conclusions.

Most client submissions are incomplete. A typical gap: the client provides a fixed asset register from accounting software, which lists acquisition cost and book value but omits serial numbers, hour meter readings, and maintenance history. Book value reflects accounting depreciation schedules, not market conditions. An asset register showing a $0 book value on a 10-year-old CNC machining center tells the appraiser nothing about what that machine would sell for in an orderly liquidation scenario.

The cost of incomplete documentation is not a delayed timeline. It is a wider value range in the final report. When an appraiser cannot verify hours, confirm maintenance history, or establish original specifications, the condition assessment relies more heavily on visual inspection and less on operational evidence. A lender reviewing two appraisals of the same equipment will give more weight to the report backed by complete documentation, because its conclusions rest on verifiable inputs rather than professional judgment filling gaps.

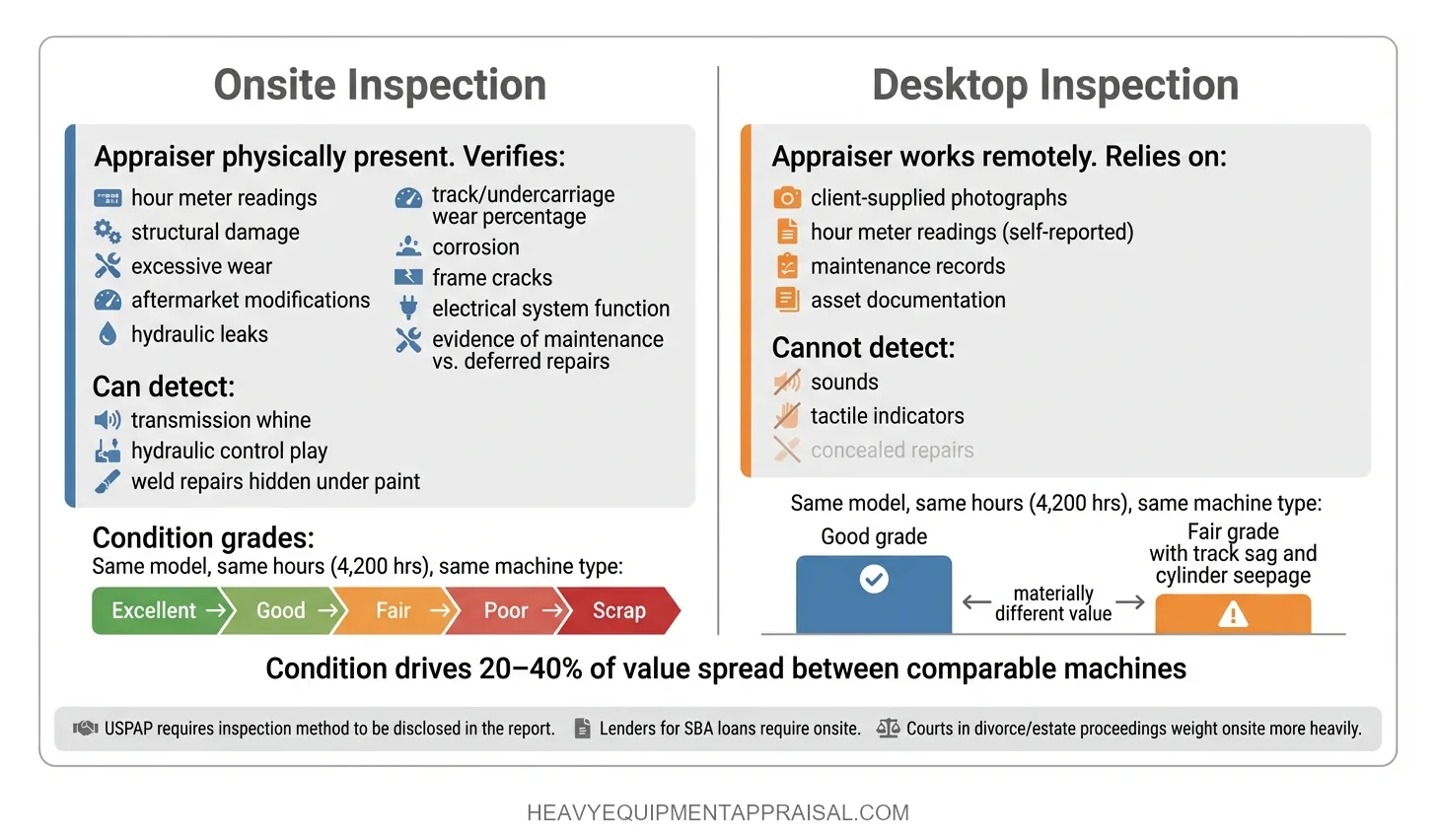

Inspection: Onsite vs. Desktop

An onsite inspection is the default standard for equipment appraisal because it allows the appraiser to verify condition, configuration, and operational status firsthand. During an onsite visit, the appraiser physically examines each asset: recording hour meter readings, checking for structural damage or excessive wear, noting aftermarket modifications, photographing the equipment from multiple angles, and assessing whether the machine matches the description on the asset list. This direct observation produces the condition grade that anchors the valuation analysis.

Condition grading follows a structured scale, typically ranging from Excellent (like-new, minimal use) through Good, Fair, and Poor, down to Scrap (no remaining utility beyond material recovery). The grade is not subjective opinion. It reflects specific, observable indicators: hydraulic leaks, tire or undercarriage wear percentages, corrosion, frame cracks, electrical system function, and evidence of regular maintenance versus deferred repairs. A crawler excavator graded “Good” with 4,200 hours returns a materially different value than the same model graded “Fair” with 4,200 hours but visible track sag and cylinder seepage. The condition assessment is where the appraiser converts physical evidence into valuation input.

Desktop appraisals skip the physical inspection entirely. The appraiser relies on client-supplied photographs, hour meter readings, maintenance records, and the asset documentation gathered in the prior stage. Desktop appraisals are acceptable under USPAP when the scope of work discloses the inspection limitation and the intended user agrees to it. Common scenarios include insurance renewals for large fleets where annual onsite visits are impractical, preliminary valuations for deal screening, and situations where equipment is located at remote or inaccessible job sites.

The critical compliance point: USPAP requires the appraisal report to disclose the inspection method used. A report that omits whether the appraiser conducted an onsite or desktop inspection is non-compliant. A party reading that report reasonably assumes onsite inspection occurred, and the undisclosed limitation undermines the report’s credibility if challenged. Lenders ordering appraisals for SBA loans almost always require onsite inspection, and courts reviewing appraisals in divorce or estate proceedings weigh onsite reports more heavily than desktop conclusions.

The gap between an onsite and desktop appraisal is not procedural preference. It is an accuracy gap. An appraiser working from photographs cannot hear a transmission whine, feel excessive play in hydraulic controls, or detect a weld repair hidden under fresh paint. When condition drives 20–40% of the value spread between comparable machines, the inspection method directly determines how much confidence the final number can carry in front of an auditor, a judge, or an underwriter.

Market Research and Valuation Analysis

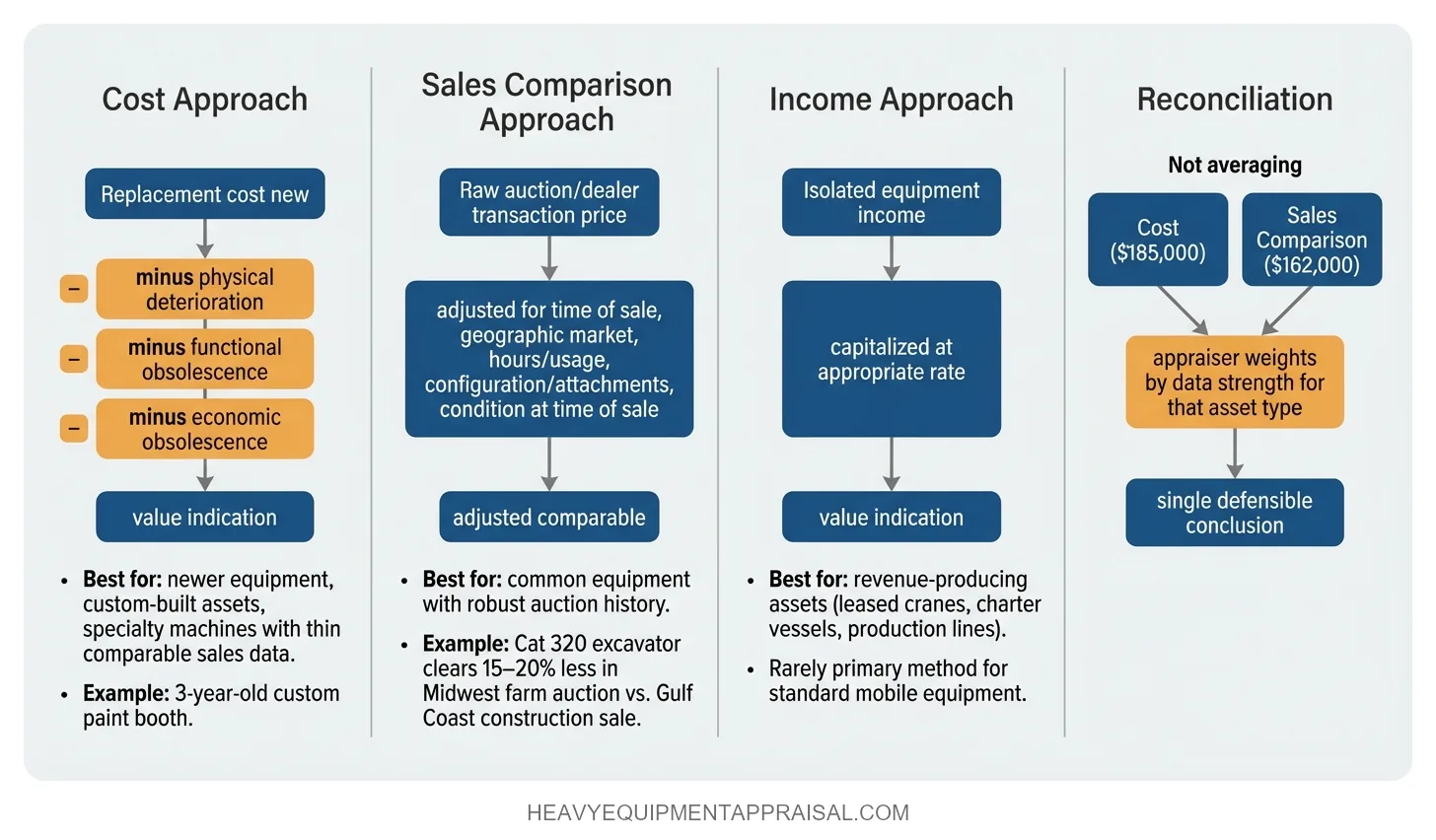

The appraiser develops a value conclusion by applying one or more of three recognized approaches: the cost approach, the sales comparison approach, and the income approach. Each approach uses different data and different logic to arrive at a value indication. The appraiser then reconciles these indications into a single weighted conclusion, giving the most weight to the approach best supported by available data for that specific asset.

The cost approach starts with what it would cost to replace the equipment new, then deducts for physical deterioration, functional obsolescence, and economic obsolescence. This approach is strongest for newer equipment, custom-built assets, and specialty machines where comparable sales data is thin. A 3-year-old custom paint booth with no auction history may have robust replacement cost data from manufacturers but zero comparable transactions to analyze.

The sales comparison approach relies on actual transaction data from auctions, dealer sales, and private-party exchanges. Sources like Ritchie Bros., IronPlanet, and Purple Wave publish realized sale prices, but these are raw transaction records, not valuations. The appraiser must adjust each comparable for differences between the sold machine and the subject asset. Five factors require adjustment on nearly every comparable: time of sale (market conditions shift), geographic market (a Cat 320 excavator clears 15–20% less in a Midwest farm auction than at a Gulf Coast construction sale), hours or usage, configuration and attachments, and condition at time of sale. A comparable pulled without these adjustments is a data point, not evidence.

The income approach capitalizes the economic benefit the equipment generates. It applies most often to revenue-producing assets like leased cranes, charter vessels, or production lines where income can be isolated to specific equipment. For standard mobile equipment, the income approach is rarely the primary method because isolating a single machine’s contribution to business revenue requires assumptions that weaken the conclusion.

Reconciliation is not averaging. If the cost approach indicates $185,000, the sales comparison approach indicates $162,000, and the income approach was not applicable, the appraiser does not split the difference at $173,500. The appraiser evaluates which approach rests on the strongest data for that asset type in that market and weights accordingly. For a common piece of heavy equipment with eight adjusted comparables, the sales comparison approach typically carries more weight than a cost approach built on estimated depreciation rates.

The rigor of this analysis is what separates a certified appraisal from an equipment blue book lookup. Automated tools apply generic depreciation curves without adjusting for geographic market, actual condition, or sale context. An appraisal that documents its comparable adjustments and reconciliation logic can withstand cross-examination in litigation or audit review. One that cannot explain how it moved from raw data to final number will not.

Appraisal Report: What It Contains and What Makes It Defensible

A defensible equipment appraisal report contains a defined set of elements: identification of the client and intended users, the intended use, the effective date of value, the value type and its source definition, a description of each appraised asset, the scope of work performed, the methodology applied, the data and reasoning supporting the value conclusion, and a signed certification by the appraiser disclosing credentials, independence, and USPAP compliance. Omitting any of these elements does not make a report incomplete. It makes it non-compliant.

USPAP distinguishes between two report formats. A full appraisal report presents sufficient detail for the intended user to understand the appraiser's reasoning without needing additional information from the appraiser. A restricted appraisal report abbreviates the analysis and limits distribution to the client only. Most lenders, courts, and regulatory bodies require the full format. A restricted report used in SBA loan underwriting or litigation will be rejected on form alone, regardless of the quality of the underlying analysis. The format decision is made at engagement for this reason.

The effective date is one of the most consequential elements in the report. It anchors the value conclusion to a specific point in time. Equipment markets shift with commodity prices, seasonal demand, and economic cycles. A report with an effective date six months before the transaction it supports invites challenge because the opposing party or the lender can argue the value has changed. In litigation, a report whose effective date does not align with the date of loss, date of death, or date of separation may be excluded entirely.

Reports fail legal or lender review for predictable reasons. The most common: the value type used does not match the intended use (fair market value delivered when the lender required orderly liquidation value). Others include missing or undisclosed appraiser qualifications, failure to disclose the inspection method, absence of comparable adjustment documentation, and an effective date misaligned with the transaction timeline. Each of these failures traces back to either a scope-of-work error at engagement or an omission during report compilation.

The report is where every prior stage (documentation, inspection, analysis) either holds together or falls apart. A value conclusion backed by disclosed methodology, adjusted comparables, and a clearly stated effective date can survive cross-examination, audit, and underwriter review. A report missing any of these structural elements gives the opposing party grounds for exclusion before the value itself is ever debated.

Timeline and Cost Expectations

A single-machine appraisal typically takes 3–7 business days from engagement to delivered report, while a fleet of 50+ assets requires 2–4 weeks. The spread within those ranges depends on four factors: assignment complexity, equipment accessibility, documentation readiness, and report format.

| Factor | Faster / Lower Cost | Slower / Higher Cost |

|---|---|---|

| Asset count | Single machine | Fleet of 50+ across multiple sites |

| Equipment type | Common (e.g., Cat D6 dozer with robust auction data) | Custom or specialty (process equipment, shop-built assets) |

| Client documentation | Complete asset list, maintenance records, serial numbers provided before engagement | Appraiser must identify and verify assets onsite |

| Report format | Restricted appraisal report | Full appraisal report under USPAP |

| Inspection method | Desktop | Onsite, especially at multiple locations |

Report format is the cost driver clients most often underestimate.

A restricted appraisal report requires less narrative detail and limits distribution to the client. A full appraisal report, which most lenders and courts require, demands documented comparable adjustments, disclosed methodology, and a complete certification. The additional drafting and review time for a full report can add 30–50% to the cost of a restricted engagement with identical equipment.

Appraiser designation level also affects pricing.

An appraiser holding an ASA or senior CMEA credential commands higher fees than a newly certified practitioner, but the credential signals litigation-tested methodology and report defensibility that lower-cost alternatives may not provide.

Rush timelines compress the research phase.

An appraiser meeting a 24-hour deadline may pull three comparables instead of 12, increasing exposure to outlier data. That compression does not just affect turnaround. It narrows the evidentiary foundation beneath the value conclusion, which determines whether the number holds when a lender's underwriter or a tax auditor tests it against independent market data.

FAQ

What is the first step in the equipment appraisal process?

The first step in the equipment appraisal process is engagement and scope of work. This step defines the assignment’s purpose, value type, intended use, intended users, inspection method, and report format before any equipment is examined. USPAP requires the scope of work to be established before fieldwork begins.

What documents should I prepare before an equipment appraisal?

Prepare asset documentation before an equipment appraisal by providing a complete equipment list and supporting records. Include make, model, year, serial number, and usage data for each asset. Add purchase invoices, maintenance records, title documents, and prior appraisals to improve valuation accuracy and reduce assumptions.

What is the difference between an onsite and desktop equipment appraisal?

The main difference between onsite and desktop equipment appraisal is that onsite appraisal involves physical inspection, while desktop appraisal relies on provided data. Onsite appraisal verifies condition, configuration, and operation firsthand. Desktop appraisal uses photos and records, which reduces accuracy and requires disclosure of inspection limits under USPAP.

How do appraisers determine the value of equipment?

Appraisers determine equipment value by selecting the most appropriate valuation approach based on available data. They use the sales comparison approach when sufficient market comps exist, the cost approach for newer or specialized equipment, and the income approach for revenue-generating assets. They then weight the strongest method to reach a defensible value conclusion.

Why would a lender reject an equipment appraisal report?

A lender would reject an equipment appraisal report when the report’s value type, scope, or format does not match the lending requirement. Common failures include using fair market value instead of orderly liquidation value, omitting the inspection method, missing comparable adjustments, or using a restricted report where a full USPAP-compliant report is required.

How long does an equipment appraisal take from start to finish?

An equipment appraisal usually takes 3–7 business days for a single machine and 2–4 weeks for a fleet of 50 or more assets. Timeline depends on documentation, inspection access, and report format. Full USPAP-compliant reports and onsite inspections increase turnaround time. Rush appraisals can be completed faster, but compressed research reduces the depth of comparable support.

What is the difference between a full appraisal report and a restricted appraisal report?

The main difference between a full appraisal report and a restricted appraisal report is that a full report supports lender underwriting with complete reasoning, data, and methodology. A restricted report limits analysis detail and distribution to the client only. Lenders, courts, and regulators usually require the full format and reject restricted reports on form alone.

What does USPAP require in an equipment appraisal?

USPAP requires an equipment appraisal to define the scope of work before fieldwork begins and to disclose the inspection method used. The report must identify the client, intended users, intended use, effective date, value type, appraised assets, methodology, supporting data, and signed certification. Missing any required element makes the report non-compliant.

Can I use the same equipment appraisal for a different lender or purpose?

You cannot use the same equipment appraisal for a different lender or purpose if the intended use or users change. USPAP requires a new scope of work for each assignment. A report prepared for internal use cannot be reused for lending without a new appraisal that matches the lender’s requirements.

How does condition grading affect equipment value?

Condition grading directly affects equipment value by determining where an asset falls within the market price range. Appraisers assign grades based on observable wear, damage, and maintenance. A lower grade can reduce value by 20–40% compared to similar equipment with better condition and identical usage.