Income Approach for Equipment Appraisal

The income approach values equipment by calculating the present value of the future economic benefits that equipment is expected to generate. In heavy equipment appraisal, the method applies only when a piece of equipment produces revenue that can be isolated and quantified, a condition most assets fail to meet.

When those conditions are present, the income approach produces defensible value conclusions. When they are not, forcing the method produces numbers that do not survive scrutiny.

What the Income Approach Measures

The income approach converts anticipated future economic benefits of owning and operating an asset into a present value estimate. The underlying logic is that an asset’s value derives from what it earns, not what it costs to replace or what comparable assets sell for. 2 techniques accomplish this conversion: direct capitalization, which divides a single year’s stabilized net operating income (NOI) by a capitalization rate, and discounted cash flow (DCF), which projects annual cash flows over the asset’s remaining useful life and discounts them to present value at a risk-adjusted rate.

The Uniform Standards of Professional Appraisal Practice (USPAP) recognizes the income approach as 1 of 3 standard approaches to value alongside the cost approach and the sales comparison approach. The method is only as reliable as the income projection inputs. Inaccurate revenue forecasts, unsupported capitalization rates, or misattributed income streams produce value conclusions that appear precise but lack foundation.

When the Income Approach Applies to Equipment

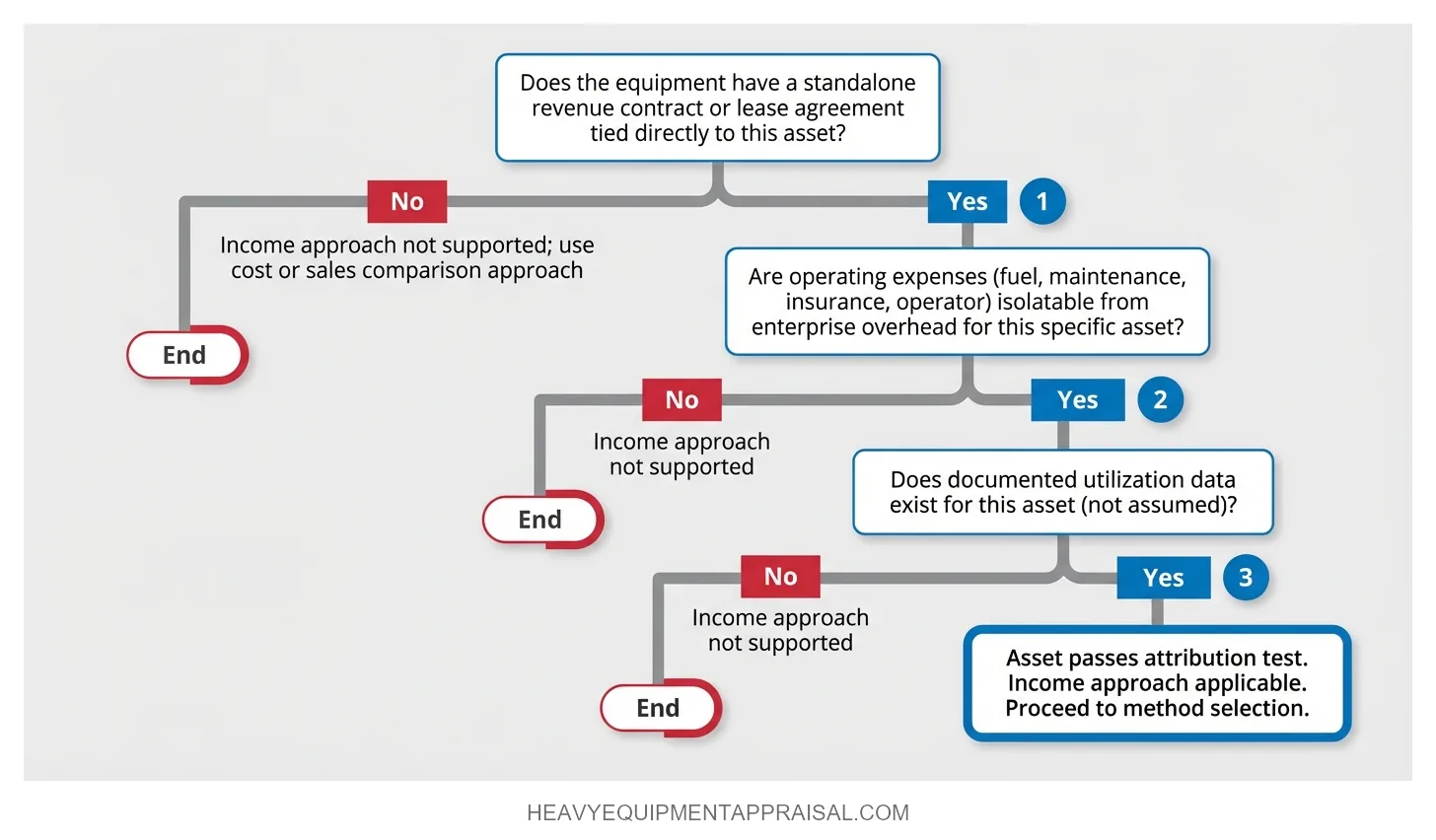

The income approach is appropriate for equipment only when the asset generates a discrete, quantifiable income stream that can be attributed to that asset alone. This is a documentation question, not an equipment-category question. A portable crushing plant operating under a fee-per-ton contract may qualify. The same model of crushing plant operating as part of an integrated quarry operation, where revenue depends on blasting, hauling, and sales functions, likely does not.

Equipment that satisfies the attribution test typically shares 3 characteristics:

- A standalone revenue contract or lease agreement ties income directly to the asset. Crane rental fleets under daily or monthly rate agreements, diesel generators under power purchase agreements, and portable light towers on long-term site contracts are common examples.

- Operating expenses are isolatable. Fuel, maintenance, insurance, and operator costs for that specific asset can be separated from broader enterprise overhead.

- Utilization data exists. The asset’s actual or projected utilization rate is documented, not assumed. A crane rented at 70% annual utilization generates different NOI than 1 at 90%.

Most heavy equipment fails this test. A bulldozer on a construction site does not generate revenue independently. Its output is embedded in a project contract that depends on labor, fuel, project management, and dozens of other inputs. The income belongs to the enterprise, not the machine. Appraisers who cannot trace income to a specific contract, lease, or rate structure for the asset in question do not have the evidentiary basis for an income approach conclusion.

How the Income Approach Is Applied in Practice

Appraisers use 2 income approach techniques for equipment: direct capitalization and discounted cash flow analysis. The choice between them depends on the income pattern and the asset’s remaining useful life.

Direct Capitalization

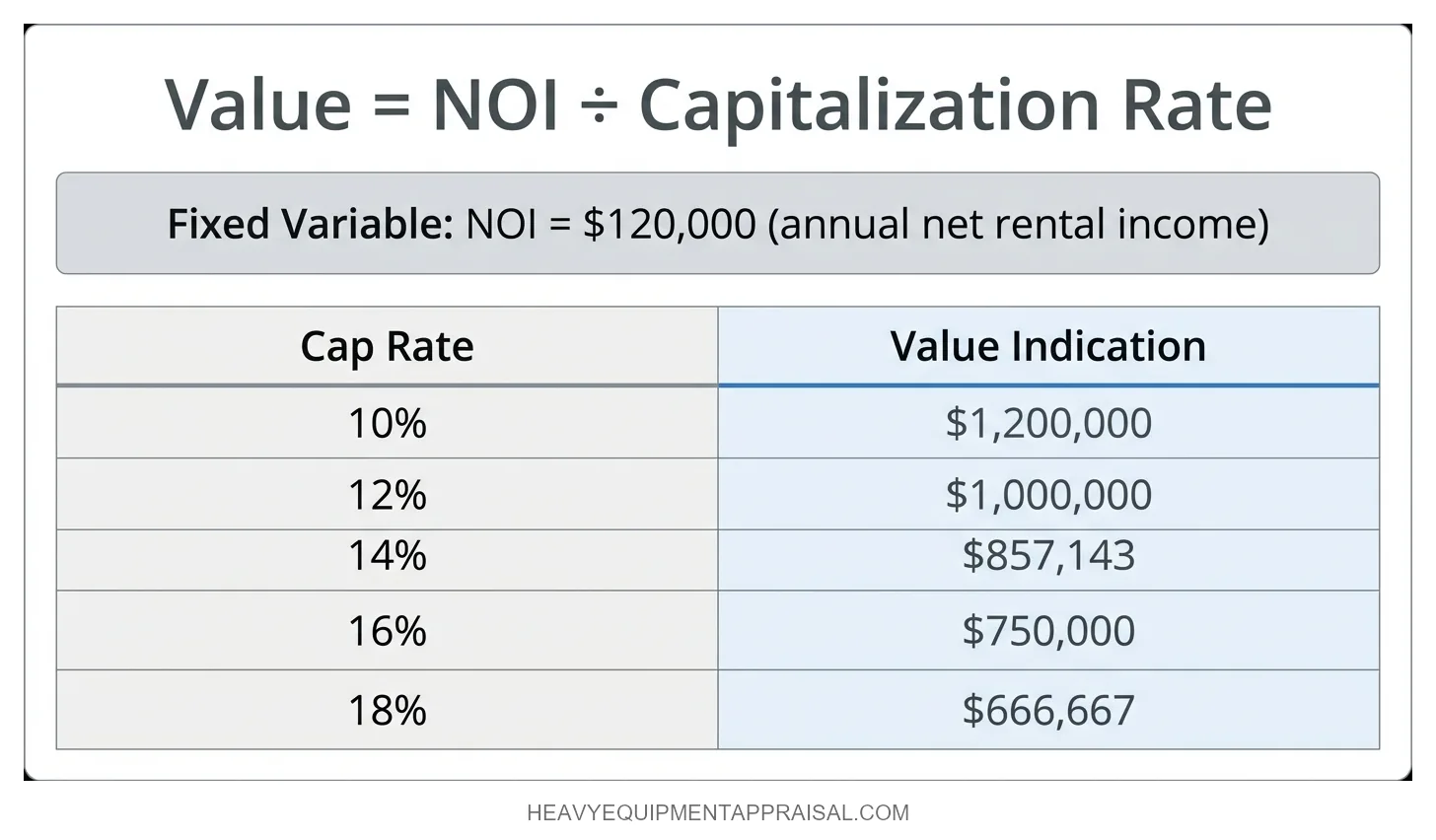

Direct capitalization applies the formula: Value = NOI / Capitalization Rate. The method assumes a stable, predictable income stream with no significant year-over-year variation. A crane generating $120,000 in annual net rental income at a 12% capitalization rate produces a value indication of $1,000,000. At a 14% rate, the same income stream indicates $857,143. That $142,857 gap illustrates why the capitalization rate is the single most consequential input in the formula.

Capitalization rate derivation for equipment is harder than for real estate. No standardized cap rate database exists for equipment categories. Real estate appraisers consult published benchmarks from organizations like CoStar or PWC. Equipment appraisers derive rates from comparable lease transactions, equipment investor return expectations, or leasing company yield requirements. Operating lease implicit rates for commercial equipment generally fall in the 12–18% range depending on asset type, useful life, and lessee creditworthiness. These rates function as market evidence, not as published benchmarks, and must be supported in the appraisal report.

Discounted Cash Flow (DCF)

DCF applies when income varies over the asset’s remaining useful life. Contract step-ups, declining utilization as the equipment ages, or a finite contract period all create cash flow patterns that direct capitalization cannot capture. The appraiser projects annual net cash flows for each year of remaining useful life, then discounts those flows to present value at a rate reflecting the asset’s risk profile.

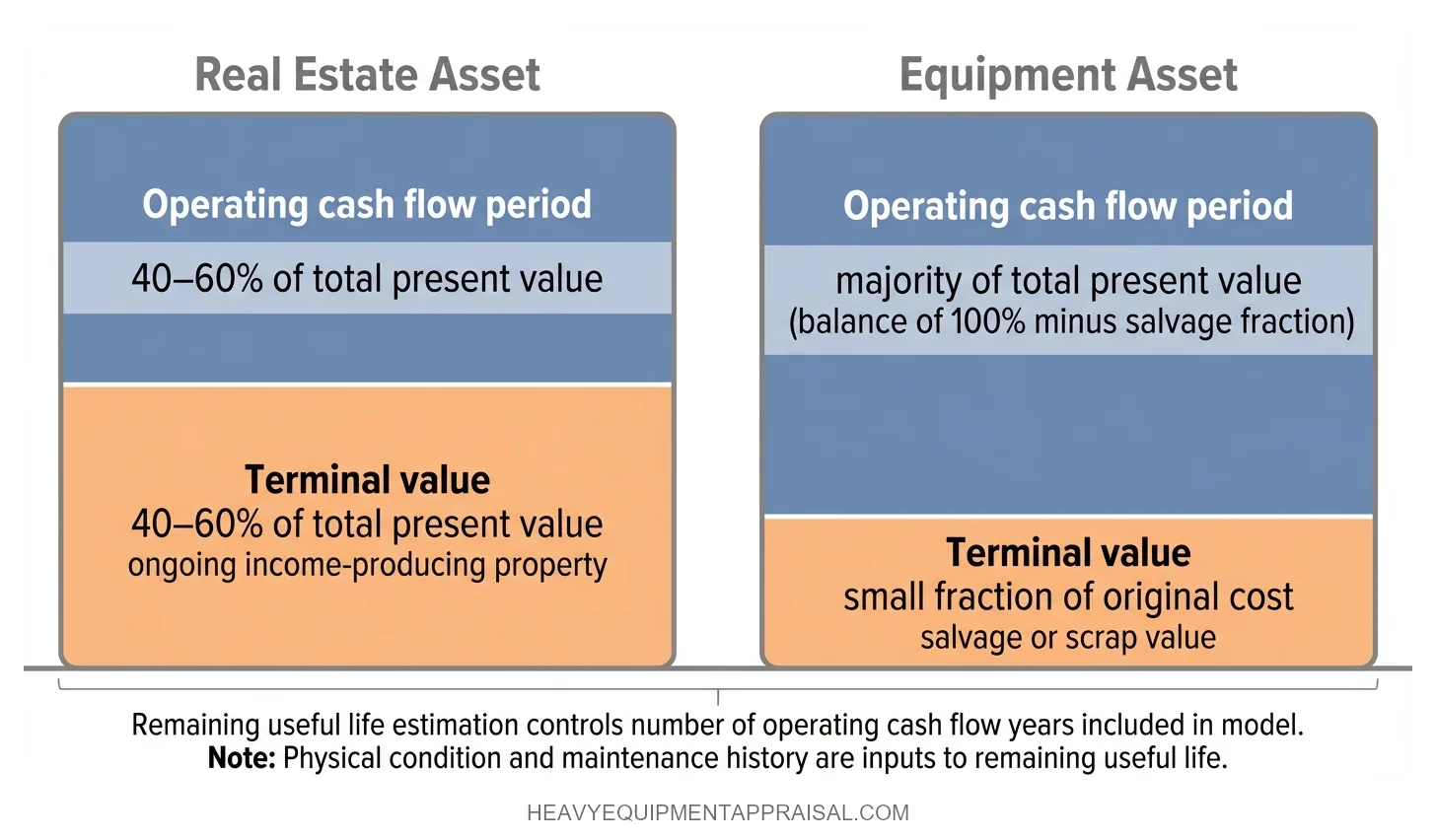

Terminal value treatment distinguishes equipment DCF from real estate DCF. In real estate, a property at the end of the projection period is typically still income-producing, and terminal value may represent 40–60% of total present value. For equipment, end-of-life value is typically salvage or scrap, often a small fraction of original cost. This means the bulk of an equipment asset’s value must be captured in the operating cash flow period, not the terminal period. Remaining useful life estimation, informed by physical condition and maintenance history, directly controls how many years of cash flow the model includes.

Limitations of the Income Approach for Heavy Equipment

The income approach produces unreliable results when the income stream cannot be isolated to the equipment itself. This describes most heavy equipment in most appraisal contexts.

The core limitation is the attribution problem. Most construction and industrial equipment operates as part of a multi-input production system. The income of a crane on a high-rise project is the project’s income, not the crane’s. A fleet of excavators working a pipeline contract generates contract revenue, but that revenue depends on operators, fuel, project coordination, permitting, and management overhead. Separating the excavator’s contribution from the enterprise’s contribution requires documented, asset-specific income data that most operations do not generate.

The cap rate derivation challenge compounds this. Real estate appraisers work from published market data. Equipment appraisers work from private lease transactions and investor yield expectations, which are less standardized and harder to verify. A capitalization rate that cannot be traced to comparable transactions is an assumption, not evidence.

The result: most equipment appraisals assign zero or minimal weight to the income approach in the final reconciliation. Its presence in a report signals a qualifying situation where income attribution is documented, not a general application of the method.

How the Income Approach Interacts with Other Methods

USPAP requires appraisers to consider all 3 approaches to value and explain any approach that is excluded or given no weight in the final reconciliation. The appraiser is not required to produce a value conclusion from every approach. The appraiser is required to document why an approach was inapplicable or unsupported for the specific assignment.

In practice, equipment appraisals rely primarily on the cost approach or the sales comparison approach. The income approach serves as a supporting method when applicable. When all 3 approaches are applied and produce different value indications, the appraiser reconciles them into a final value conclusion by weighing the quality and applicability of each method's data for the specific assignment. The income approach receives the most weight only when the income data is strong, the capitalization rate is well-supported, and the other approaches produce less reliable indications for that particular asset.

For equipment appraisals in M&A or litigation contexts, documenting all 3 approaches and their relative weight strengthens the report's defensibility. An opposing expert who sees only 1 approach applied will question whether the appraiser considered alternatives that might have produced a different result.

What This Means for Lenders, Owners, and Attorneys

Any income approach conclusion in an equipment appraisal report should be scrutinized for whether the income stream is genuinely attributable to the equipment or is borrowed from the broader business.

Lenders reviewing collateral appraisals for SBA loans or conventional equipment financing should expect the income approach to appear rarely. When it does appear, the report should document the specific income source: a lease agreement, a rental rate schedule, or a contract with identifiable revenue terms. An income approach conclusion without that documentation inflates collateral value on unsupported projections.

Business owners operating equipment that generates verifiable lease or contract income may see legitimately higher value indications under the income approach than under cost or sales comparison methods. That income stream represents value the other methods do not capture. Owners preparing for an appraisal should surface lease agreements, rental histories, and utilization records. This documentation gives the appraiser the inputs needed to apply the income approach credibly.

Attorneys in litigation, divorce, or estate proceedings can challenge income approach conclusions on attribution grounds. The strength of that challenge depends on whether the appraiser can identify the specific contract or lease generating the income attributed to the equipment. If the appraiser derived income from enterprise revenue rather than asset-specific documentation, the conclusion collapses under cross-examination. The income approach, when misapplied, produces numbers that feel authoritative but do not survive adversarial scrutiny. When correctly applied to qualifying assets, it captures economic value that cost and sales comparison methods miss entirely.