Heavy Equipment Appraisal for Insurance

An equipment appraisal for insurance establishes the correct value basis for coverage, claims, and dispute resolution. Insurance policies do not default to fair market value. They use replacement cost new (RCN) or actual cash value (ACV), and the appraisal must match the policy’s defined standard.

Without a defensible appraisal aligned to the right value type, equipment owners face structural misalignment between what they’re covered for and what they’d actually receive at claim time.

Why Insurance Requires Its Own Valuation Standard

Insurance appraisals operate under value definitions that differ from those used in lending, sale transactions, or tax reporting. The FMV standard assumes a hypothetical transaction between a willing buyer and a willing seller, neither under compulsion, both with reasonable knowledge of relevant facts.

Insurance policies do not model a hypothetical sale. They model a restoration of function: what it costs to replace the lost or damaged asset with one of like kind and quality, or what the depreciated value of that asset was immediately before the loss.

This distinction produces materially different numbers. FMV for a 10-year-old motor grader reflects what a buyer would pay in the open market, which incorporates negotiation, market supply, and buyer alternatives. RCN for the same machine reflects what it costs to buy a new equivalent from the manufacturer, have it delivered, and put it into service.

For aging equipment with years of useful life remaining, RCN is almost always higher than FMV. An appraisal that applies FMV to an insurance context systematically undervalues the equipment, leaving the owner with a coverage gap that becomes visible only at the worst possible moment.

Policy language governs the value standard. The appraiser’s first task is to read the policy schedule and identify which value definition controls. An appraisal that uses the wrong basis produces a number that, however technically competent, cannot support the claim it was meant to anchor.

Replacement Cost New vs. Actual Cash Value

Replacement cost new (RCN) and actual cash value (ACV) are the two primary value bases for equipment insurance coverage, and the gap between them drives the most consequential coverage decisions equipment owners face.

RCN is the total cost to acquire, deliver, install, and commission a new asset of like kind and quality at current market prices. That figure includes freight, rigging, foundation work, and startup testing. It is not limited to the equipment purchase price alone. A $380,000 piece of processing equipment may carry an RCN of $430,000 once delivery, installation, and commissioning are factored in.

ACV is RCN minus depreciation.

Three categories of depreciation apply: physical depreciation (wear, corrosion, fatigue from use and age), functional obsolescence (design deficiencies or superadequacies compared to current models), and economic obsolescence (external factors like market contraction or regulatory changes that impair value regardless of the asset’s condition). The appraiser applies each category based on inspection findings and research, not from a generic schedule.

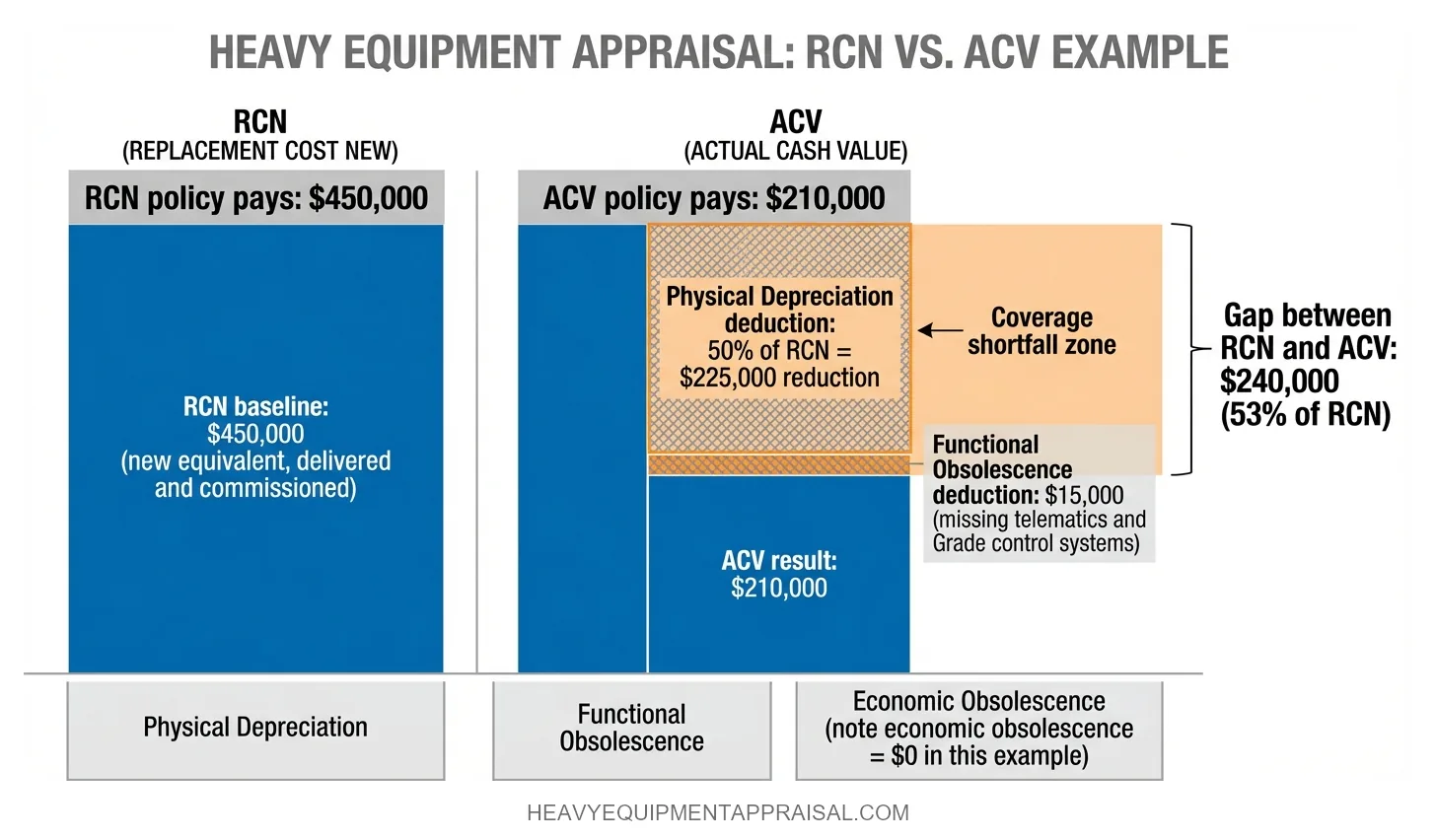

Consider a 10-year-old crawler excavator.

Current dealer pricing for a new equivalent, including delivery and commissioning, produces an RCN of $450,000. Total economic life for this class of equipment is 20 years. With normal wear and a documented maintenance history, the effective age matches the calendar age of 10 years. Physical depreciation is 50%, reducing the value to $225,000. The appraiser identifies functional obsolescence: the machine lacks current-spec telematics and Grade control systems that reduce operating efficiency relative to a new unit. That deficiency warrants a $15,000 deduction. The resulting ACV is $210,000.

The gap between $450,000 and $210,000 is 53%. An owner carrying ACV coverage on this machine will receive $210,000 at total loss. That is not enough to purchase a replacement. Owners who carry RCN coverage receive the full replacement cost regardless of the equipment’s age or depreciated condition. The choice between RCN and ACV coverage is the single largest determinant of whether a loss event creates a financial shortfall.

When Equipment Appraisals Are Required for Insurance

Three scenarios trigger a formal appraisal requirement in the insurance context: initial policy underwriting for high-value or specialized equipment, a claim dispute when the insurer and the insured disagree on value, and periodic re-appraisal as equipment values shift over time.

Insurance carriers writing policies on equipment above a certain value threshold frequently require a certified appraisal at policy inception. That threshold varies by carrier and line of coverage, but $100,000 per asset is a common benchmark for commercial property and inland marine policies. Specialized or custom-built equipment often triggers an appraisal requirement regardless of dollar value, because the carrier lacks published data to verify the owner’s stated coverage amount.

Claim disputes are the second trigger. When a total loss or significant damage event occurs, the insurer’s adjuster produces a value estimate. If the equipment owner disagrees, an independent appraisal becomes the evidentiary basis for negotiation or formal dispute resolution. Without a pre-loss appraisal on file, the owner enters this process without an independent baseline. The adjuster’s estimate becomes the starting point by default.

The third trigger is time. Equipment replacement costs change as manufacturers adjust pricing, supply chains shift, and new models replace discontinued ones. A pre-loss appraisal conducted 5 years ago may bear little resemblance to current RCN. Carriers and risk managers who recognize this require periodic re-appraisal to keep coverage limits aligned with actual replacement economics.

How Appraisers Determine Value for Insurance

The cost approach to equipment valuation is the dominant methodology for insurance appraisals. Its logic maps directly to the insurance question:

What does it cost to restore the lost function?

The appraiser establishes RCN using current manufacturer pricing, dealer quotes, or cost reference services such as Marshall Valuation Service. From that baseline, the appraiser applies physical depreciation, functional obsolescence, and economic obsolescence to arrive at ACV.

The sales comparison approach serves as a secondary method when the equipment has an active secondary market. Forklifts, skid steers, over-the-road trucks, and late-model construction equipment generate enough auction results and dealer transactions to support comparable sales analysis. When both approaches are viable, the sales comparison approach provides a useful cross-check against the cost approach conclusion.

For specialty or custom equipment with no comparable sales, the cost approach is the most credible method.

The appraiser cannot rely on automated valuation tools or pricing guides that lack coverage for the asset in question. Sourcing RCN for these assets requires direct manufacturer or fabricator quotes, component-level cost buildup, or documented reproduction cost analysis. The quality of that sourcing directly determines whether the appraisal will withstand scrutiny from an insurer’s claims department or an opposing appraiser in a dispute proceeding.

The Role of Appraisals in Claim Settlements

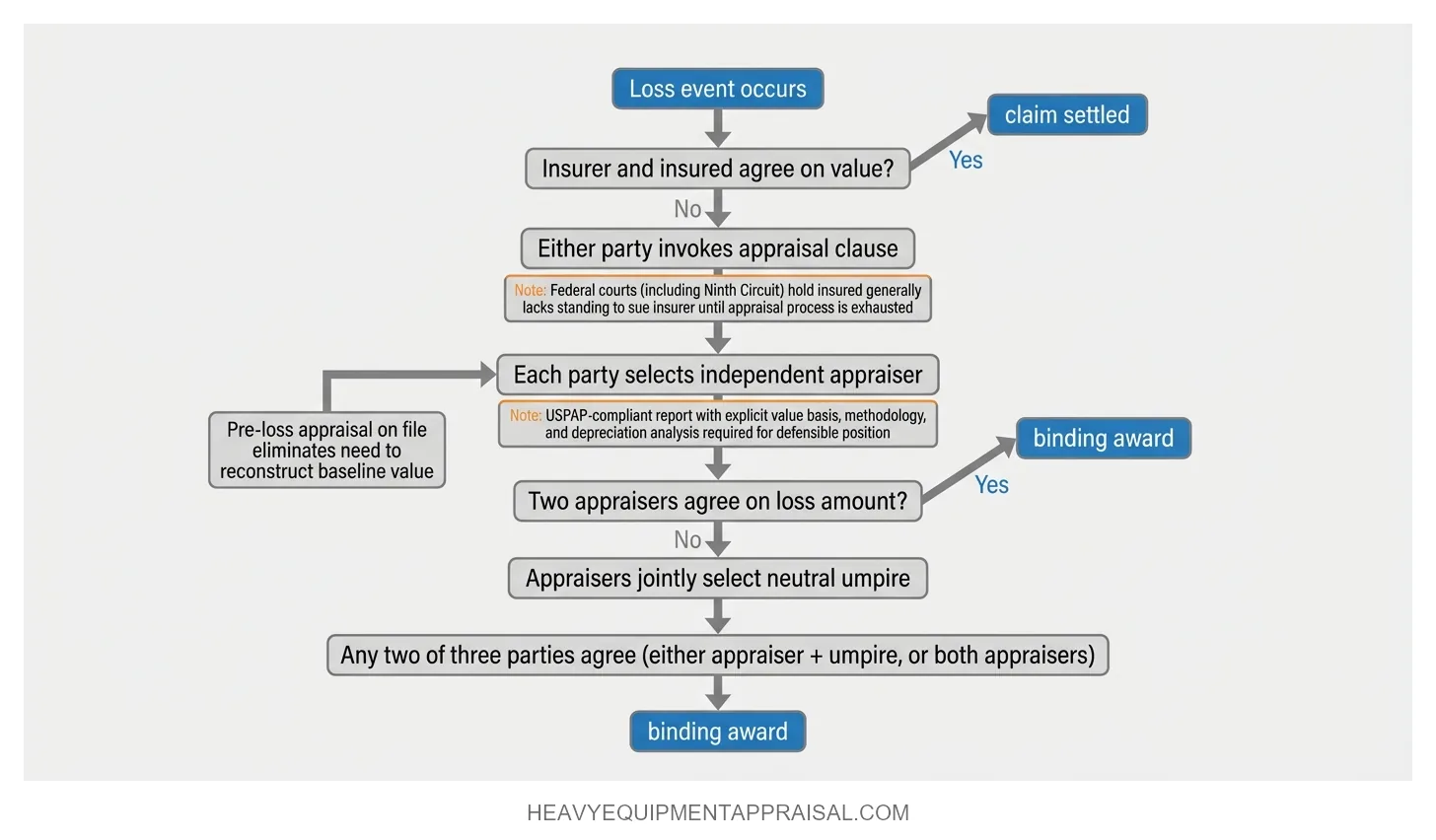

A certified appraisal is the primary instrument for resolving valuation disputes between equipment owners and insurers after a loss event. The mechanism for this resolution is built into most commercial property and inland marine policies through an appraisal clause.

The appraisal clause works as follows:

When the insured and the insurer cannot agree on the value of a loss, either party may invoke the clause. Each party then selects an independent, competent appraiser. The two appraisers attempt to agree on the loss amount. If they cannot, they jointly select a neutral umpire. Agreement of any two of the three parties (either appraiser and the umpire, or both appraisers) constitutes a binding award. Federal courts, including the Ninth Circuit, have held that an insured generally lacks standing to sue the insurer over a valuation dispute until the appraisal process has been exhausted.

This makes the quality of the appraiser and the appraisal report the decisive factors in claim outcomes. An appraisal that meets USPAP requirements and explicitly states the value basis, methodology, and assumptions is defensible in the appraisal clause process. A report that omits these elements, or applies the wrong value standard, undermines the insured’s position before the umpire is ever selected.

Two distinct appraisal events exist in the insurance lifecycle, and conflating them is a common source of confusion:

The pre-loss appraisal is conducted before any loss event occurs. It establishes RCN or ACV at a point in time and sets the coverage limit. The post-loss appraisal is conducted after damage or destruction has occurred. It assesses the extent of damage, determines the pre-loss value of the equipment, and may estimate repair costs.

Pre-loss appraisals are condition assessments and replacement cost analyses. Post-loss appraisals are damage assessments that often require the appraiser to reconstruct both the asset’s pre-loss condition and the cost to restore it. Having a pre-loss appraisal on file simplifies the post-loss process because the baseline value is already documented rather than reconstructed from memory and incomplete records.

Specialized and Custom Equipment

Standard equipment with active secondary markets can often be valued using published auction data and dealer transactions as cross-checks against the cost approach. Specialized or custom equipment has no such data. Purpose-built processing lines, custom-fabricated structures, OEM-discontinued machinery, and one-off industrial assets require a pure cost approach valuation.

The appraiser faces a threshold question with these assets: whether to use replacement cost (the cost to acquire a new asset of equivalent utility) or reproduction cost (the cost to construct an exact duplicate). For insurance purposes, replacement cost is generally the appropriate basis because insurers are restoring function, not recreating museum pieces. If a modern machine with equal or superior capability exists, RCN reflects that machine’s cost. Reproduction cost is reserved for situations where no functional equivalent is available and the only option is to rebuild the original.

For custom fabrications, the appraiser must reverse-engineer the build cost at current prices. That means documenting raw materials, machining, welding, assembly labor, engineering, and overhead. Then applying depreciation based on inspected condition, not on a generic age-life table. The research burden is substantially higher than for standard equipment, and the consequences of shortcuts are proportionally larger. An under-valued specialty asset at policy inception creates a coverage gap that may not surface for years, until a fire, flood, or equipment failure forces a claim that the coverage cannot fully satisfy.

Selecting an Appraiser for Insurance Purposes

Insurance appraisals require a credentialed appraiser who understands both equipment markets and the specific value definitions that govern insurance coverage. Two credentials signal relevant expertise: the Accredited Senior Appraiser (ASA) designation from the American Society of Appraisers, and the Certified Machinery and Equipment Appraiser (CMEA) designation from the American Machinery and Equipment Appraisers Association (AMEA). Both require demonstrated competency in machinery and equipment valuation. Additional detail on what these credentials require and how they differ is covered in HEA's appraiser qualifications guide.

The appraiser's report must be USPAP-compliant and must explicitly state the value basis used. This is where insurance appraisals diverge from general equipment appraisals in a consequential way. An appraiser who defaults to FMV without confirming the policy's value standard produces a report that is technically valid but functionally useless for insurance purposes. The report should name the value type (RCN, ACV, or both), identify the policy context, and describe the methodology and depreciation analysis in enough detail for a claims adjuster, an opposing appraiser, or an umpire to evaluate the conclusion.

Industry experience matters as much as credentials for specialty assets. An appraiser credentialed in machinery and equipment but unfamiliar with food processing lines, marine equipment, or mining machinery may lack the sourcing relationships and technical knowledge to produce defensible RCN figures for those categories. When selecting an appraiser for high-value or specialized equipment, verifying category experience is as important as verifying the designation after the name.

Policy Types and Their Appraisal Implications

Three common policy structures determine how an insurer pays a claim, and each one implies a different appraisal requirement. These distinctions are absent from most guidance on insurance appraisals, but they control downstream outcomes.

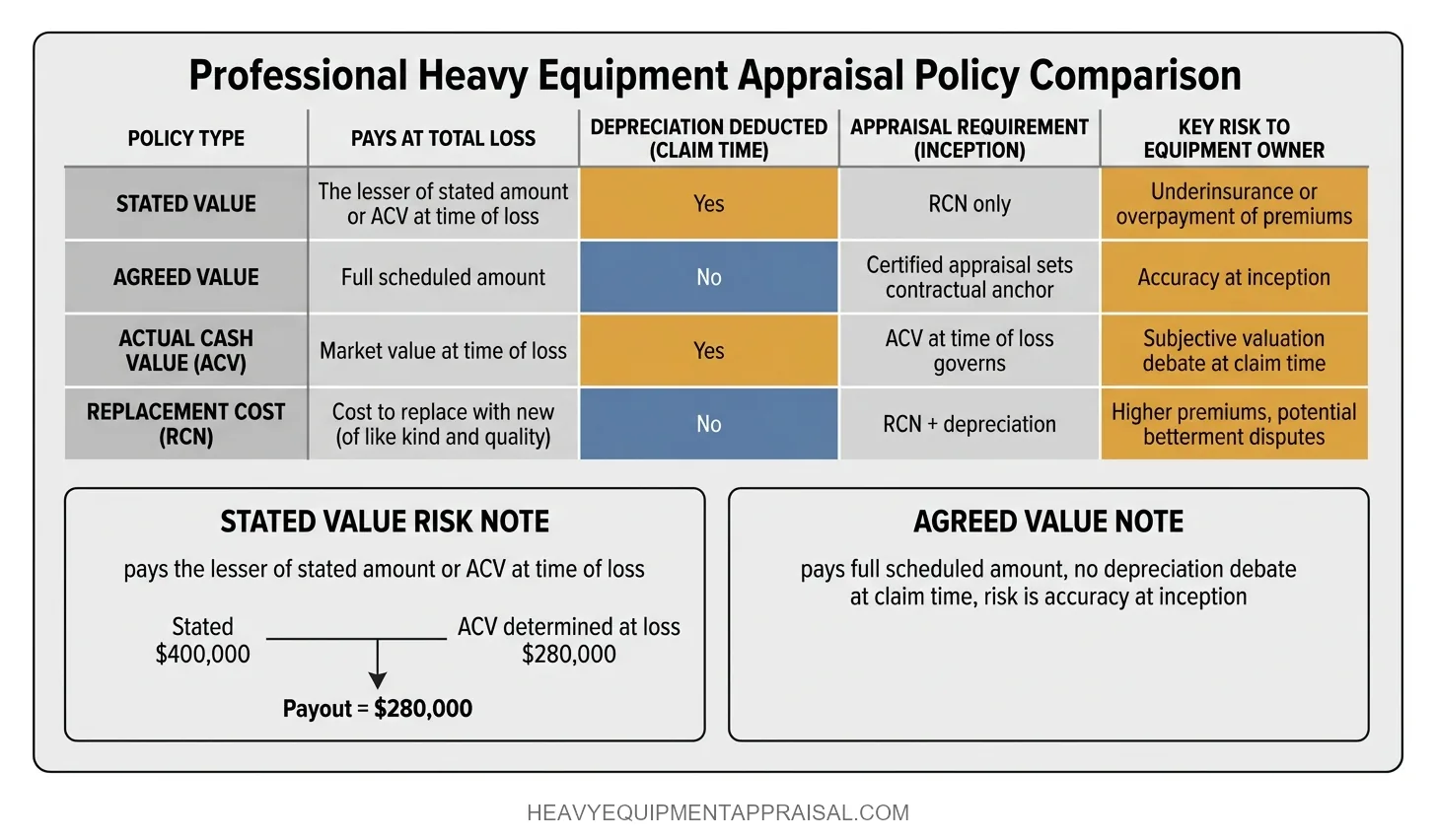

Replacement cost (RCN) policies pay the full cost to replace the equipment with a new item of like kind and quality. No depreciation is deducted from the claim payment. The appraisal task is to establish current RCN accurately. Overstating RCN inflates premiums. Understating it creates a coverage shortfall.

Actual cash value (ACV) policies pay RCN minus depreciation. The appraisal must establish both RCN and the appropriate depreciation, producing a net ACV figure. This is the more complex appraisal task because the depreciation analysis requires condition assessment, effective age determination, and judgment on functional and economic obsolescence.

Agreed value policies pay a scheduled amount that the insurer and insured have agreed upon in advance, typically supported by a certified appraisal at policy inception. No depreciation is applied at claim time. The appraisal serves as the contractual anchor. If the agreed value is $300,000 and a total loss occurs, the insurer pays $300,000 without further valuation debate. The risk shifts to accuracy at inception: if the agreed value is too low, the owner absorbs the gap. If too high, premiums are inflated for the policy term.

A fourth structure, the stated value policy, pays the lesser of the stated amount or the actual value at the time of loss. Stated value policies appear to offer a guaranteed payout but do not. If the stated amount is $400,000 but the insurer determines ACV at the time of loss is $280,000, the insurer pays $280,000. Stated value policies create a false sense of security for equipment owners who assume the stated figure is what they'll receive.

Each structure requires a different appraisal emphasis. RCN policies need accurate current replacement cost. ACV policies need accurate replacement cost and defensible depreciation. Agreed value policies need the appraisal to be right at inception because no adjustment happens at claim time. Stated value policies need the owner to understand that the appraisal determines actual payout, not the stated number on the schedule.

Keeping Coverage Current Through Periodic Re-Appraisal

Equipment replacement costs change as manufacturers adjust pricing, supply chains tighten, and new models supersede discontinued ones. An appraisal conducted at policy inception becomes progressively less accurate with each passing year.

For commonly traded construction and industrial equipment, a re-appraisal cycle of every 2–3 years for high-value assets reflects industry practice. The rationale is straightforward. New equipment list prices for major manufacturers have increased at rates exceeding general inflation in recent years. A crawler excavator that carried an RCN of $400,000 in 2020 may carry an RCN of $475,000 in 2024. If the coverage limit was set at the 2020 figure and never updated, the owner is underinsured by $75,000 at the moment of a total loss.

Specialty equipment may require more frequent review if the underlying cost inputs (custom fabrication labor rates, specialty steel or alloy pricing, engineering costs) are volatile. Conversely, stable commodity equipment in low-inflation environments may hold its RCN relatively flat for longer periods.

The re-appraisal also captures condition changes. Equipment that has been rebuilt, upgraded, or retrofitted may carry a higher ACV than the original appraisal reflected. Equipment that has been neglected or subjected to unusually harsh operating conditions may have depreciated faster than the original age-life projection assumed. Without periodic re-appraisal, these changes accumulate silently, widening the gap between the policy's coverage limit and the equipment's actual insurable value.

FAQ

What is the difference between replacement cost new and actual cash value in equipment insurance?

The main difference between replacement cost new and actual cash value is depreciation. Replacement cost new pays 100% of the cost to replace equipment with new equivalent equipment. Actual cash value pays the current depreciated value based on age, condition, and usage, often 20–60% lower than new cost.

When does an insurance carrier require a formal equipment appraisal?

An insurance carrier requires a formal equipment appraisal when equipment values are high, unique, disputed, or difficult to verify with invoices or market listings. Carriers often require appraisals for scheduled equipment, large fleets, renewals with value changes above 10–20%, and claims involving total loss, financing, or policy limit reviews.

How does the appraisal clause work in a commercial property or inland marine policy?

The appraisal clause resolves disputes over the amount of loss, not coverage. In a commercial property or inland marine policy, each side selects one appraiser, and the two appraisers choose an umpire. If they disagree, the umpire decides. A written agreement by any two usually sets the binding loss amount.

What credentials should an equipment appraiser have for insurance purposes?

An equipment appraiser for insurance purposes should hold recognized appraisal credentials, documented machinery valuation experience, and knowledge of insurance loss standards. Strong credentials include CMEA, ASA, AMEA, or other accredited appraisal designations, plus 5–10 years of equipment inspection experience, USPAP compliance, and the ability to produce defensible, insurer-ready reports.

How often should equipment appraisals be updated to keep insurance coverage current?

Update equipment appraisals every 12–24 months to keep insurance coverage current. High-value fleets, rapidly depreciating machines, and volatile resale markets often require annual updates. Stable equipment schedules may support a 24-month cycle. Also update an appraisal after major purchases, upgrades, losses, or market value changes above 10–15%.

Why is fair market value the wrong standard for equipment insurance appraisals?

Fair market value is the wrong standard for equipment insurance appraisals because insurance measures indemnity based on replacement cost or actual cash value, not open-market sale price. Fair market value reflects what a willing buyer would pay a willing seller, which can understate insured value by 15–40% for specialized, scarce, or revenue-critical equipment.

How is ACV calculated for specialized or custom-built heavy equipment?

ACV for specialized or custom-built heavy equipment is calculated by starting with replacement cost new, then subtracting depreciation for age, condition, usage hours, obsolescence, and limited market demand. Appraisers also adjust for custom features, rebuild history, and comparable sales. For specialized equipment, ACV often falls 25–50% below replacement cost new.

How does functional obsolescence affect equipment insurance value?

Functional obsolescence lowers equipment insurance value by reducing usefulness, efficiency, or productivity compared with newer equipment. Insurers and appraisers apply this loss when outdated design, slower output, or unsupported systems reduce value, even if the machine still works. Functional obsolescence can reduce ACV by 10–35% depending on severity, age, and market demand.