Heavy Equipment Appraisal for Tax Purposes

A certified equipment appraisal is required by the IRS for any noncash charitable contribution of equipment exceeding $5,000, and is the standard of proof for estate tax filings, cost segregation studies, and business personal property tax appeals.

What separates a tax-purpose appraisal from a commercial one is the compliance framework:

- The IRS defines who can perform it

- When it must be completed

- What the report must contain

An appraisal that fails any of those requirements can invalidate the deduction entirely, regardless of the accuracy of the value conclusion.

When a Tax Authority Requires a Certified Equipment Appraisal

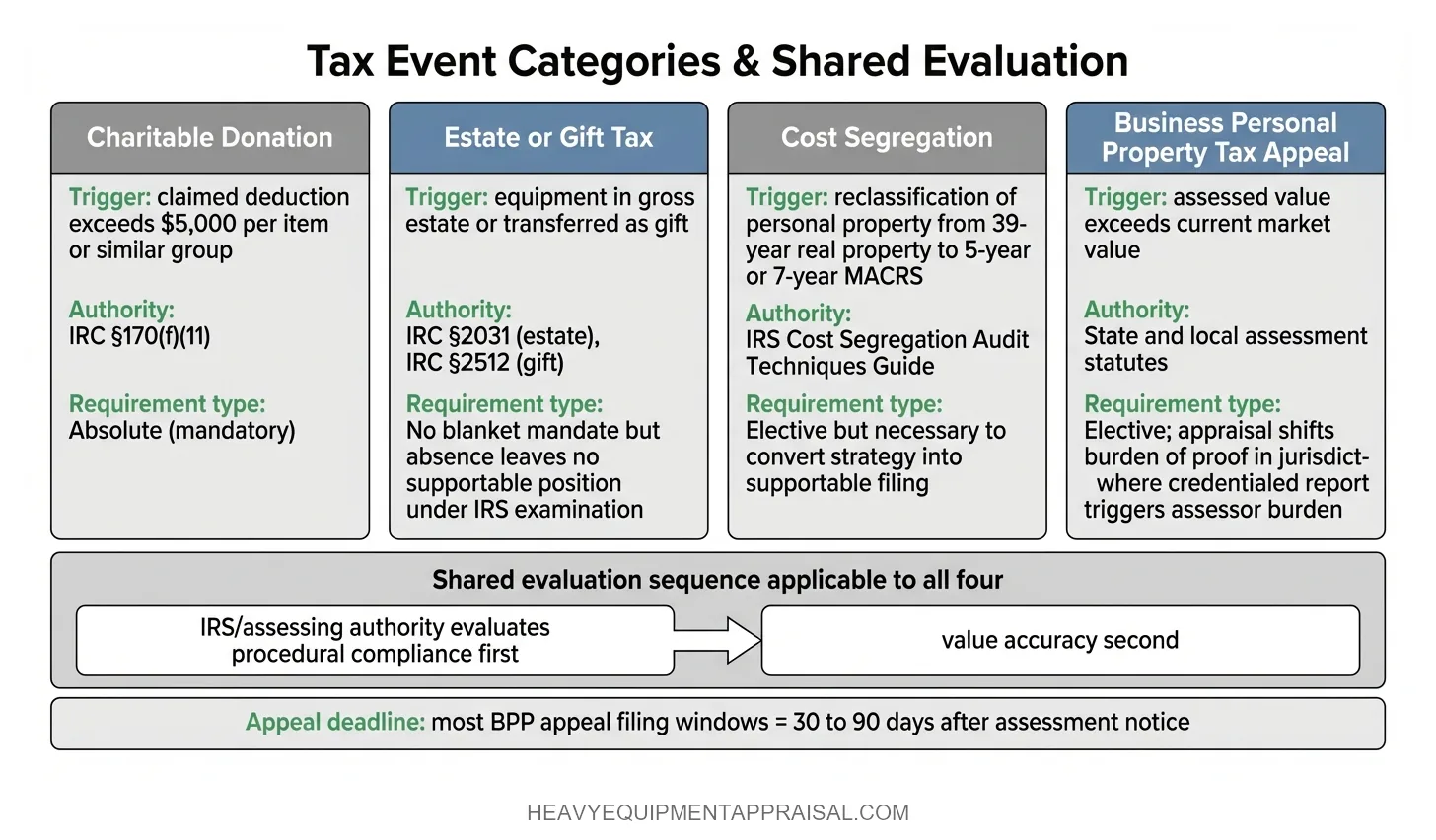

Four categories of tax events trigger a requirement or strong need for a certified equipment appraisal:

| Tax Event | Trigger | Authority |

|---|---|---|

| Charitable donation | Claimed deduction exceeds $5,000 per item or similar group | IRC §170(f)(11) |

| Estate or gift tax | Equipment is part of a gross estate or transferred as a gift | IRC §2031 (estate), IRC §2512 (gift) |

| Cost segregation | Personal property is reclassified from real property to accelerate depreciation | IRS Cost Segregation Audit Techniques Guide |

| Business personal property tax appeal | Assessed value exceeds current market value | State/local assessment statutes |

Charitable donations above the $5,000 threshold carry an absolute requirement for a qualified appraisal. Estate and gift tax situations do not impose a blanket appraisal mandate, but an IRS examination of an estate return without a credentialed appraisal backing the equipment values leaves the executor with no supportable position.

Cost segregation and property tax appeals are elective, but in both cases, the appraisal is the instrument that converts a tax strategy into a supportable filing.

The common thread across all four events is that the IRS or the assessing authority will evaluate the appraisal on procedural compliance first and value accuracy second. A report that gets the number right but violates the timing rule, credential requirement, or content standard is treated the same as no appraisal at all.

IRS Qualified Appraisal and Qualified Appraiser Standards

The IRS imposes two distinct requirements under IRC §170(f)(11) and Treasury Reg. §1.170A-17: the appraisal itself must be a qualified appraisal, and the person who performs it must be a qualified appraiser. Failing either one disqualifies the deduction.

Qualified Appraiser: Credential and Exclusion Requirements

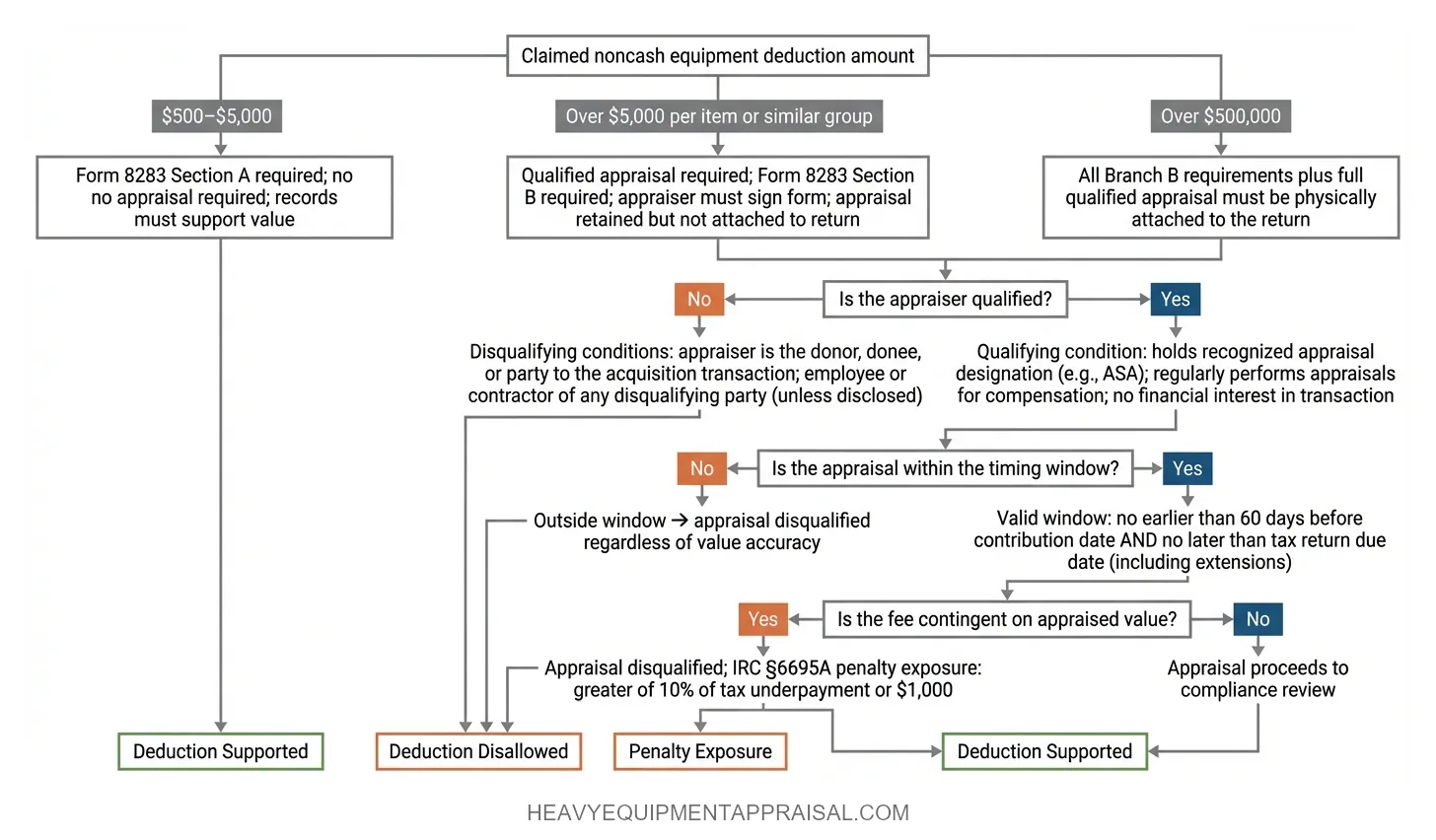

A qualified appraiser must hold an appraisal designation from a recognized professional appraisal organization, or otherwise meet minimum education and experience requirements under the regulation. The appraiser must regularly perform appraisals for compensation. Recognized designations include the ASA's accredited designations and comparable credentials from established appraisal organizations.

The exclusions are equally specific. An appraiser is disqualified from a specific transaction if the appraiser is the donor, the donee, or a party to the transaction in which the donor acquired the property.

Employees, partners, or independent contractors regularly engaged by any of those parties are also excluded unless the relationship is disclosed on Form 8283. These rules exist to ensure independence.

A qualified appraiser with appropriate credentials who has no financial relationship to the transaction is the only safe selection.

Qualified Appraisal: Timing and Content Requirements

A qualified appraisal must be conducted no earlier than 60 days before the date of the contribution and completed no later than the due date (including extensions) of the tax return on which the deduction is first claimed.

This timing window is absolute.

An appraisal completed 61 days before the donation, or one day after the return deadline, is disqualified regardless of the quality of the analysis.

The appraisal fee must not be contingent on the appraised value. A fee arrangement tied to a percentage of the value conclusion, or structured as a success fee, disqualifies the appraisal and exposes both the appraiser and the taxpayer to penalties.

IRC §6695A imposes a penalty on appraisers who produce appraisals resulting in a substantial or gross valuation misstatement. The penalty equals the greater of 10% of the tax underpayment attributable to the misstatement or $1,000.

Value Standard Used in Tax-Purpose Appraisals

Fair market value is the IRS-mandated value standard for charitable contributions, estate tax, gift tax, and most property tax contexts. The IRS defines FMV in Treasury Reg. §1.170A-1(c)(2) as

"The price at which the property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having reasonable knowledge of relevant facts."

This definition is substantially identical to the Uniform Standards of Professional Appraisal Practice (USPAP) definition and the American Society of Appraisers (ASA) definition.

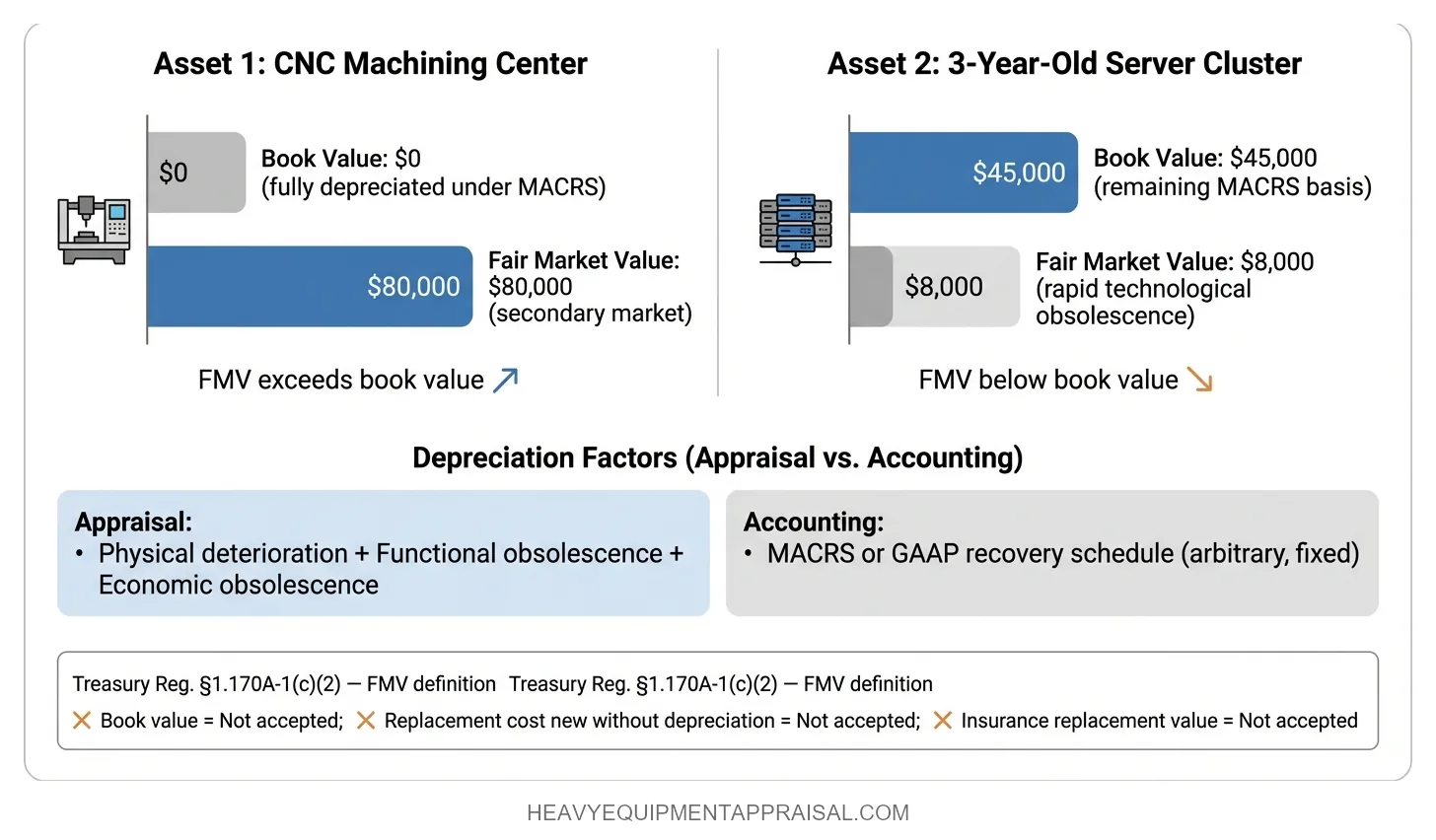

The IRS does not accept book value, replacement cost new (without depreciation), or insurance replacement value as substitutes for FMV. This is the single most common taxpayer error in equipment-related tax filings: substituting an accounting figure for a valuation conclusion.

Book value (the net depreciated cost on a balance sheet under GAAP or MACRS schedules) diverges from FMV in both directions and often dramatically. A CNC machining center fully depreciated on the books at $0 may retain $80,000 or more in FMV on the secondary market. A 3-year-old machine with a remaining book value of $45,000 may have an FMV of $8,000 due to rapid technological obsolescence.

Accounting depreciation follows arbitrary recovery schedules. Appraisal depreciation reflects actual physical deterioration, functional obsolescence, and economic obsolescence.

These two figures almost never align, and the IRS draws the distinction explicitly:

Charitable Donation of Equipment: Form 8283 Requirements

Donations of equipment with a claimed value above $5,000 require a qualified appraisal and a completed Form 8283, Section B. The threshold applies per item or per group of similar items donated to the same donee in the same tax year. Equipment items cannot be split across categories to stay below the threshold, and similar items donated to the same donee are aggregated.

The $5,000 Threshold and the $500,000 Rule

| Claimed Deduction | Filing Requirement |

|---|---|

| $500 – $5,000 | Form 8283, Section A (no appraisal required, but records must support value) |

| Over $5,000 per item or similar group | Qualified appraisal required. Form 8283, Section B. Appraiser signs the form |

| Over $500,000 | Full qualified appraisal must be attached to the return |

For donations between $5,000 and $500,000, the full appraisal does not need to be attached to the return, but it must be retained and produced upon IRS request. The appraiser must sign Section B of Form 8283, attesting to the appraised value and confirming the fee arrangement is not contingent on the result.

What Happens When Form 8283 Is Incomplete

An incomplete Form 8283, a missing appraiser signature, or an appraisal that omits any required element gives the IRS grounds to disallow the deduction in full.

The Tax Court has applied a "substantial compliance" doctrine in limited circumstances, allowing minor clerical defects to survive challenge. But circuit courts have taken stricter positions. In practice, relying on substantial compliance as a fallback strategy is a gamble that most tax advisors counsel against.

A blue book printout or broker opinion has no standing in this context, regardless of how plausible the number appears.

Cost Segregation and Equipment Appraisal

A cost segregation study accelerates depreciation by reclassifying tangible personal property and land improvements out of the 39-year nonresidential real property MACRS class and into 5-year or 7-year recovery periods. The net present value of the tax savings can be substantial for large commercial or industrial property acquisitions.

The equipment appraisal component of a cost segregation study identifies and values the personal property assets that are being reclassified. The appraiser's role is distinct from the engineer's. The engineer identifies whether an asset is a structural component of the building or separable personal property (the classification determination). The appraiser assigns values to the segregated personal property using the cost approach, typically replacement cost new less depreciation.

The IRS Cost Segregation Audit Techniques Guide rates engineering-based studies as producing the most reliable results but does not require a credentialed machinery and equipment appraiser for the equipment identification component.

In practice, cost segregation firms typically employ engineers. However, when a study is challenged on valuation grounds rather than classification grounds, the absence of a credentialed appraiser weakens the position significantly. The value allocation is, by definition, an appraisal function.

A credentialed appraiser's involvement transforms the study from an engineering exercise with estimated values into a USPAP-compliant valuation that survives IRS examination.

Estate and Gift Tax: Equipment as a Taxable Asset

Equipment included in a gross estate must be valued at FMV as of the date of death or the alternate valuation date (if elected under IRC §2032). Equipment transferred as a gift must be valued at FMV as of the date of transfer. The valuation determines the taxable value of the asset and directly affects the estate or gift tax liability.

Business equipment is frequently the most undervalued asset category in estate filings. Executors and estate attorneys default to book value or salvage estimates because equipment "looks old." A fleet of eight crawler excavators carried at $0 on a contractor's depreciation schedule may represent $600,000 or more in FMV. Understating values creates audit risk. Overstating values inflates the tax liability unnecessarily.

In either direction, a certified appraisal for estate purposes is what establishes the supportable number.

The appraisal must reflect the condition and market at the valuation date, not the date the appraiser inspects the equipment. For estates, this distinction matters when months pass between the date of death and the appraisal engagement. The appraiser must reconstruct the value as of the effective date, documented with market data contemporaneous to that date. This retroactive valuation requirement adds complexity and is a common deficiency in estate appraisals that face IRS examination.

Property Tax Appeals and Equipment Valuation

Assessed value on business personal property (BPP) tax rolls is frequently overstated because assessors rely on cost-schedule methods that do not account for functional or economic obsolescence. The assessor applies a published depreciation factor to the original acquisition cost, producing a value that may bear little relationship to actual market value.

A certified appraisal establishing FMV at the assessment date is the primary rebuttal instrument in a formal appeal. The appraiser's report provides asset-specific analysis including condition, remaining useful life, and observed obsolescence that the assessor's mass-appraisal methodology cannot capture. For equipment with active secondary markets, the sales comparison approach produces the most persuasive evidence. For specialized or process-integrated equipment, a market-derived cost approach incorporating observed depreciation is the standard method.

Most jurisdictions impose short filing windows for BPP appeals, commonly 30 to 90 days after the assessment notice. The appraisal must be commissioned and completed within that window to be admissible. In jurisdictions where the burden of proof shifts to the assessor when a credentialed appraisal is presented, the report's existence alone changes the dynamic of the appeal. Without it, the assessor's cost-schedule figure stands unchallenged.

What a Tax-Purpose Appraisal Report Must Contain

A USPAP-compliant equipment appraisal for tax purposes must include specific elements to survive IRS or assessor scrutiny. Treasury Reg. §1.170A-17(a)(4) enumerates the required content for a qualified appraisal in the charitable donation context, but these elements represent the credibility floor for any tax-purpose appraisal.

Required Elements Under Treasury Reg. §1.170A-17

Property description: Sufficient detail to identify the equipment. Make, model, serial number, year of manufacture, and condition at the time of appraisal.

Contribution date: The date (or expected date) of the donation, transfer, or the effective valuation date for estate or property tax purposes.

Terms of agreement: Any restrictions, conditions, or agreements relating to the use, sale, or disposition of the property.

Appraiser identification: Name, address, and taxpayer identification number of the qualified appraiser.

Appraiser qualifications: Background, experience, education, and professional appraisal organization memberships.

Purpose statement: An explicit statement that the appraisal was prepared for income tax purposes (or estate tax, gift tax, or property tax purposes, as applicable).

Appraisal date: The date the property was appraised.

Value conclusion: The appraised FMV on the contribution or effective date.

Methodology: The valuation method used and the specific basis for the conclusion, including comparable sales data, cost calculations, or depreciation analysis.

Fee disclosure: Confirmation that the appraiser's fee is not contingent on the appraised value.

USPAP Compliance as the Credibility Floor

USPAP compliance is what separates a supportable appraisal from a document the IRS can dismiss on procedural grounds. USPAP requires the appraiser to identify the intended use, the intended user, the type and definition of value, the effective date, and the scope of work. It requires the appraiser to not mislead and to produce a credible result supported by relevant evidence.

An appraisal that satisfies the Treasury Regulation requirements but violates USPAP standards (for example, by omitting a scope of work discussion or failing to identify the applicable value premise) is vulnerable in an audit.

USPAP compliance is not a credential checkbox. It is the structural foundation that makes the appraisal admissible and the value conclusion withstand scrutiny.

FAQ

What is the IRS threshold that requires a qualified appraisal for donated equipment?

The IRS generally requires a qualified appraisal for donated equipment when the claimed noncash charitable deduction exceeds $5,000. The appraisal must usually be completed before filing the tax return, and the donor must attach Form 8283, Section B. Publicly traded securities are excluded, and higher-value categories can trigger additional IRS documentation rules.

Who qualifies as a qualified equipment appraiser under IRS rules for equipment donations?

A qualified appraiser under IRS rules is an individual with verifiable education and experience in valuing the type of donated equipment being appraised, who regularly performs paid appraisals and is not disqualified by relationship or prohibited status. The appraiser must meet Treasury regulations, prepare a qualified appraisal, and sign Form 8283 when required.

What is the timing window for completing an equipment appraisal before a charitable contribution?

The IRS timing window requires a qualified appraisal for donated equipment to be dated no earlier than 60 days before the contribution date and no later than the due date, including extensions, of the tax return that first claims the deduction. This timing rule applies when the donation requires a qualified appraisal under IRS charitable contribution rules.

Why does the IRS reject book value for equipment tax filings?

The IRS rejects book value for equipment tax filings because book value reflects accounting depreciation, not fair market value or qualified appraised value. Book value is based on cost minus scheduled depreciation under internal accounting or tax methods. That figure often differs from the equipment’s actual market worth, so the IRS does not treat book value as reliable proof of value for donations, gains, losses, or estate reporting.

What must be included in a qualified appraisal report under Treasury Reg. §1.170A-17?

A qualified appraisal report under Treasury Reg. §1.170A-17 must identify the donated equipment, state the contribution date, describe the property’s physical condition, and explain the valuation method used to determine fair market value. The report must also include the appraiser’s qualifications, declaration of independence, fee arrangement, valuation effective date, and the specific facts supporting the final value conclusion.

Does estate tax law require a certified appraisal for business equipment?

Estate tax law does not generally require a “certified appraisal” by that exact term for business equipment, but it does require credible fair market value support on Form 706. For closely held business assets, a qualified independent appraisal is often necessary to defend value, reduce IRS challenge risk, and support estate tax reporting.

What is the penalty for an appraiser who produces a valuation misstatement under IRC §6695A?

The penalty under IRC §6695A applies when an appraiser prepares an appraisal that results in a substantial or gross valuation misstatement for certain tax filings. The penalty is generally the lesser of 10% of the underpayment attributable to the misstatement, $1,000, or 125% of the appraisal fee. Gross misstatements can trigger higher IRS scrutiny and stronger penalty exposure.

How does a certified equipment appraisal support a business personal property tax appeal?

A certified equipment appraisal supports a business personal property tax appeal by documenting fair market value with defensible evidence, market comparables, and depreciation analysis. The appraisal helps prove that the assessor overstated cost, condition, or remaining life. Strong appraisals often address age, obsolescence, usage, and local market data to support a lower taxable value.

What is the role of a machinery and equipment appraiser in a cost segregation study?

A machinery and equipment appraiser in a cost segregation study identifies, classifies, and values tangible personal property separate from the building. The appraiser supports 5-, 7-, or 15-year asset lives by documenting equipment cost, condition, and function. This valuation helps allocate purchase price correctly and supports accelerated depreciation with defensible evidence.