Cost Approach for Equipment Appraisal (Formula + Examples)

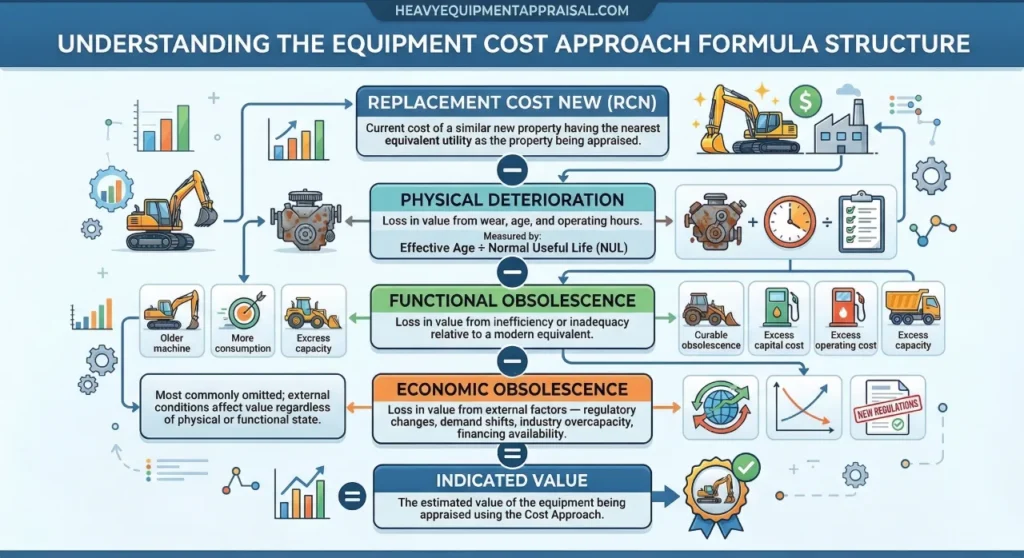

The cost approach determines equipment value by calculating replacement cost new (RCN) and subtracting all 3 forms of depreciation:

- Physical deterioration

- Functional obsolescence

- Economic obsolescence

It is 1 of 3 standard approaches to machinery and equipment appraisal, and the primary method when an asset has no active secondary market. Because the math always produces a number, credibility depends on whether all 3 forms of depreciation are applied rigorously, not just the ones easiest to quantify.

What Is the Cost Approach in Equipment Appraisal?

The cost approach is grounded in the principle of substitution:

A prudent buyer will not pay more for an asset than the cost of acquiring a substitute of equivalent utility. Applied to equipment appraisal, the structure is direct → start with what the asset would cost to replace new, subtract every form of value loss a buyer would recognize, and the result is the indicated value.

ASA training defines the starting point as replacement cost new (RCN). The current cost of a similar new property having the nearest equivalent utility as the property being appraised. RCN differs from reproduction cost new, which estimates the cost to recreate an exact copy using original materials and methods.

For most equipment, replacement cost is the correct starting point because it reflects what a buyer would spend to acquire equivalent utility today, not the cost of replicating an outdated design.

The 3 required deductions from RCN are physical deterioration, functional obsolescence, and economic obsolescence.

Each represents a distinct category of value loss, and a cost approach conclusion that applies only 1 or 2 of the 3 overstates what the market would pay. In the context of a complete machinery and equipment appraisal, the cost approach is 1 of 3 recognized methods, and the one most appropriate when market sales data is thin or absent.

The Three Types of Depreciation (and Why All Three Matter)

Cost approach depreciation is not a single calculation. It is 3 separate measurements, each accounting for a different source of value loss. ASA defines the combined result as the estimated loss in value of an asset when compared with a new asset of equivalent utility.

| Type | Definition | Equipment Example |

|---|---|---|

| Physical deterioration | Loss in value from wear, age, and operating hours | A motor grader with 12,000 hours and deferred maintenance carries more physical depreciation than a same-year unit with a documented service record |

| Functional obsolescence | Loss in value from inefficiency or inadequacy relative to a modern equivalent | A concrete pump that consumes 30% more fuel per cubic yard than current models suffers functional obsolescence from excess operating cost |

| Economic obsolescence | Loss in value from external factors: regulatory changes, demand shifts, industry overcapacity, financing availability | An asphalt paver operating in a region where road contracts have declined sharply faces economic obsolescence regardless of its physical condition |

Physical deterioration is most commonly measured using the age/life method. Per ASA’s 2024 Normal Useful Life Study, standard heavy mobile construction equipment (including excavators, crawler cranes, motor graders, dump trucks, and front-end loaders) carries a normal useful life (NUL) of 10–15 years.

The calculation: Physical Depreciation = Effective Age ÷ NUL. A crawler excavator with a 7-year effective age against a 12-year NUL carries approximately 58% physical depreciation before functional and economic factors are applied.

Functional obsolescence has 4 distinct forms:

- Curable obsolescence (fixable by component upgrade, measured by cost to cure)

- Obsolescence from excess capital cost (when a modern equivalent costs less to acquire than the original)

- Obsolescence from excess operating cost (measured by the present value of the operating penalty over remaining useful life)

- Obsolescence from excess capacity (when a single asset operates below rated output due to internal system constraints, not external demand).

Economic obsolescence is the most commonly dismissed of the 3 forms and the most consequential when missed. External conditions reduce value regardless of an asset’s physical or functional state, and excluding them without documented research produces a cost approach conclusion that overstates what the market would pay.

How to Calculate Replacement Cost New (RCN)

RCN can be established by 2 methods:

- Direct pricing, obtained from the manufacturer or dealer for an equivalent new asset

- Trending, which applies a published price index to the asset’s historical cost to estimate what it would cost new today.

Direct pricing is straightforward when the equipment is still in production. When the original model is discontinued, the appraiser identifies the modern equivalent (the asset providing the same functional utility) and prices that unit instead.

Trending applies when direct pricing is unavailable or when consistency with cost-based benchmarks is required.

The formula: Current RCN = (Current Index ÷ Base Year Index) × Historical Cost. Trending applies to the asset’s historical cost (what it cost when first placed into service by its original owner), not the price the current owner paid, which may reflect a used-market transaction.

The Bureau of Labor Statistics (BLS) Producer Price Index (PPI) program publishes equipment-specific index series for this purpose. The FRED database series WPU1168, which tracks PPI for service industry machinery, stood at 336.5 in January 2026 (base: June 1982 = 100). An appraiser trending a machine with a 2015 historical cost of $200,000 divides the current index by the 2015 index value and multiplies by $200,000 to arrive at today’s RCN.

A complete RCN extends beyond the purchase price. ASA training distinguishes direct costs (equipment price, freight, rigging, installation labor, electrical connections, foundations, and sales tax) from indirect costs such as engineering fees, permits, and insurance during installation. For heavy equipment requiring site preparation or specialized rigging, these additional costs can add 15–25% to the base purchase price.

The resulting RCN sets the ceiling of value in a cost approach analysis. No informed buyer pays more for a used asset than what an equivalent new one would cost to acquire and put in service.

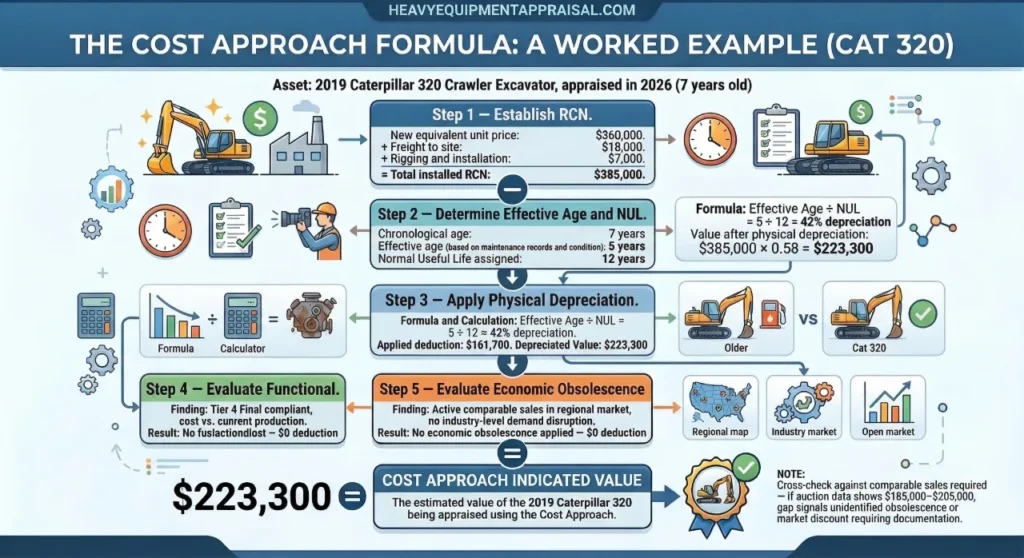

The Cost Approach Formula: A Worked Example

The following applies the cost approach to a 2019 Caterpillar 320 crawler excavator appraised in 2026, 7 years after manufacture:

- Establish RCN. The current price for a new equivalent unit is $360,000. Add freight to site ($18,000) and rigging and installation ($7,000). Total installed RCN: $385,000.

- Determine effective age and NUL. The excavator is 7 years old chronologically. Maintenance records are complete and wear is consistent with normal operating hours. Effective age is estimated at 5 years. Per ASA’s 2024 Normal Useful Life Study, crawler excavators fall within the standard heavy mobile construction equipment range of 10–15 years. NUL assigned: 12 years.

- Apply physical depreciation. Physical Depreciation = Effective Age ÷ NUL = 5 ÷ 12 = 42%. Value after physical depreciation: $385,000 × 0.58 = $223,300.

- Evaluate functional obsolescence. The unit is Tier 4 Final compliant and shows no excess operating cost relative to current production equivalents. No functional obsolescence applied.

- Evaluate economic obsolescence. Active comparable sales in the regional market and no identified industry-level demand disruption. No economic obsolescence applied.

- Cost approach indicated value: $223,300.

The appraiser cross-checks this result against comparable sales before issuing a final opinion. If auction data shows similar units transacting at $185,000–$205,000, the gap signals either unidentified obsolescence in the cost approach or a market discount that must be documented and explained.

Neither result is final until the cost approach conclusion and market evidence are reconciled.

When Appraisers Use the Cost Approach for Heavy Equipment

The cost approach is the primary valuation method when no active secondary market exists for the equipment being appraised.

Standard yellow iron (crawler excavators, motor graders, wheel loaders) trades frequently enough that the sales comparison approach is typically the lead method. Specialized or custom-fabricated equipment rarely does.

Equipment that commonly requires the cost approach includes custom-designed process machinery, specialized manufacturing equipment built to a single company’s specifications, one-off fabrications, and assets whose secondary market is too thin to produce reliable comparables. When the population of true comparables is too small to bracket the subject asset on age, condition, capacity, and configuration, the cost approach provides a methodologically grounded value indication that does not depend on finding a matching sale.

The cost approach also serves a normalizing function when secondary market data exists but is inconsistent. Auction prices for the same equipment type can vary widely based on sale conditions, bidder pool, and geographic market. Developing a cost approach indication alongside the sales comparison approach allows the appraiser to test whether market outliers are distorting the data or whether the cost approach itself is missing an obsolescence factor.

For insurance purposes, the cost approach takes a specific form: replacement cost new with no depreciation deduction applied. Insurers covering equipment against physical loss need to know what replacement would cost today, not what the asset’s depreciated market value is. This is a distinct assignment from a market value appraisal and requires the definition of value to be clearly stated in the engagement agreement and report.

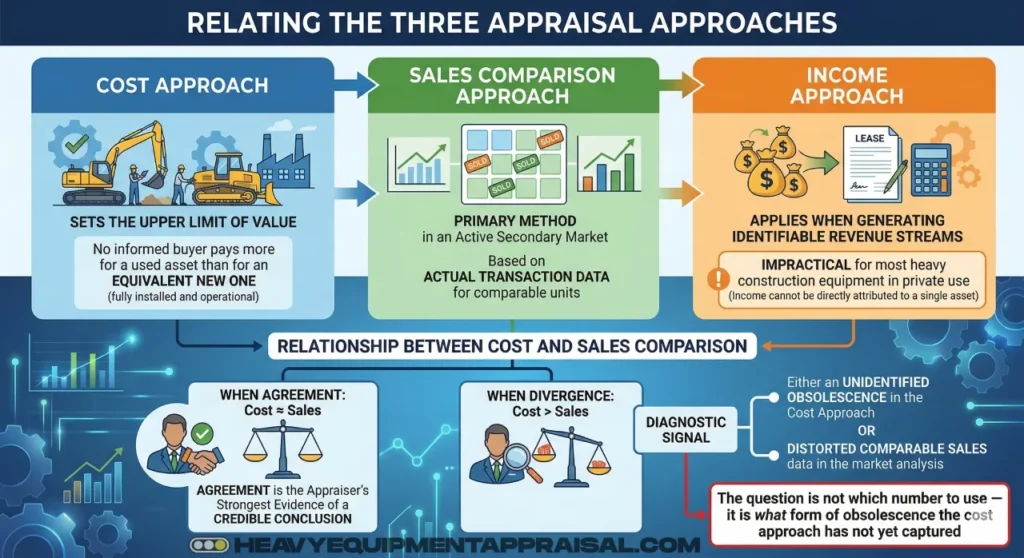

How the Cost Approach Relates to the Other Valuation Methods

The Uniform Standards of Professional Appraisal Practice (USPAP) require appraisers to consider all 3 approaches to value (cost, sales comparison, and income) and apply those that are credible given the assignment’s scope and available data.

The cost approach is not a fallback for when the other methods fail. It is a parallel analytical framework that models value from a different starting point.

NEBB training establishes a key principle: the cost approach sets the upper limit of value. No informed buyer pays more for a used asset than what it would cost to acquire an equivalent new one, fully installed and operational. When the cost approach and the sales comparison approach converge on similar values, that agreement is the appraiser’s strongest evidence of a credible conclusion. When they diverge significantly, the divergence is diagnostic. It points to either an unidentified obsolescence factor in the cost approach or distorted comparable sales data in the market analysis.

The income approach applies when equipment generates identifiable revenue streams: rental fleets, revenue-producing process lines, or assets in sale-leaseback arrangements. For most heavy construction equipment in private use, income cannot be directly attributed to a single asset, making the income approach impractical. The cost approach fills that gap.

In practice, a well-constructed equipment appraisal uses the cost approach result as a ceiling check. If market data shows the asset selling for significantly less than the cost approach indication, the question is not which number to use. It is what form of obsolescence the cost approach has not yet captured.

Common Mistakes That Produce Non-Credible Cost Approach Values

Most cost approach errors share a common root: the formula always produces a number, and a number that looks precise can obscure the judgment calls that determined it. Three patterns appear most frequently in non-credible cost approach conclusions.

Dismissing Economic Obsolescence Without Research

Economic obsolescence is the most commonly omitted depreciation factor, and it is often dismissed with a single unsupported assertion: “the company is profitable,” “the facility operates at high capacity,” or “management confirmed no obsolescence exists.”

None of these observations establishes the absence of economic obsolescence.

External factors operate at multiple levels: the broader economy, the specific industry, and the individual asset’s market position. Each level requires independent investigation and documented findings. Dismissal without research is not a conclusion. It is a gap in the analysis.

Accepting the Math Without Cross-Checking the Market

The cost approach formula always produces a result. That result is credible only when reconciled with what the market actually shows.

If an RCN calculation produces an indicated value of $280,000 and comparable units are transacting at $150,000–$175,000, the gap is not a rounding error. It is evidence that a depreciation factor has been underestimated or omitted. The appraiser’s responsibility is to explain the gap, not report the cost approach result without testing it.

Using Book Value as a Proxy for RCN

IRS Publication 946 governs how equipment is depreciated for tax purposes under the Modified Accelerated Cost Recovery System (MACRS). Most machinery falls under a 7-year MACRS recovery period. Contractor equipment may qualify as 5-year property. Once the recovery period ends, the asset carries zero book value on the owner’s tax records, regardless of its actual condition or market value. An appraiser who starts a cost approach analysis from a fully depreciated book value has answered the wrong question. Book value is a tax recovery record. RCN is a market cost estimate.

How Cost Approach Results Connect to Value Definitions (FMV, OLV, FLV)

The cost approach, as typically applied, produces an indication of fair market value (FMV): the price at which equipment would change hands between a willing buyer and a willing seller, neither under compulsion, both with reasonable knowledge of relevant facts. The underlying logic mirrors FMV assumptions: RCN represents what a knowledgeable buyer would pay for an equivalent new asset, and the depreciation deductions represent what that buyer would discount for age, inefficiency, and external conditions.

The premise of value (the transaction assumptions embedded in the conclusion) determines which cost approach inputs are appropriate. An FMV-in-continued-use conclusion assumes the asset remains installed and operational at its current location, so RCN includes freight and installation costs. An FMV-removed conclusion assumes the buyer bears relocation costs, so those amounts are excluded. The premise is not selected after the analysis. It is defined at the outset of the assignment.

Orderly liquidation value (OLV) and forced liquidation value (FLV) are not separate cost approach outputs. They are adjustments applied to an FMV indication to reflect different transaction conditions. OLV assumes a seller under time pressure with a limited but reasonable marketing period. FLV assumes immediate disposition, typically at public auction. Both sit below FMV because compulsion and compressed timelines reduce what the market will pay relative to an arm's-length transaction.

A lender sizing collateral, an insurer setting replacement coverage, and an IRS estate filing each require a different definition of value, and the cost approach inputs that produce a credible FMV conclusion are not the same inputs that produce a credible OLV conclusion. For a direct comparison of when each value type applies in equipment appraisal, see fair market value vs. OLV vs. FLV: when to use which.

What is replacement cost new (RCN) and how is it different from book value?

Replacement cost new (RCN) is the current cost to buy a new item with the same function and capacity as the existing equipment. Heavy equipment book value is the asset’s accounting value after depreciation. RCN measures what replacement costs today. Book value measures what remains on financial statements.

How do you calculate physical depreciation for heavy equipment using the age/life method?

Calculate physical depreciation for heavy equipment with the age/life method by dividing effective age by total economic life, then multiplying by 100. For example, equipment with an effective age of 6 years and a 15-year life has 40% physical depreciation. This method estimates wear based on age relative to expected service life.

What's the difference between functional obsolescence and economic obsolescence in equipment appraisal?

The main difference between functional obsolescence and economic obsolescence is that functional obsolescence results from internal equipment flaws, while economic obsolescence results from external market or environmental conditions.

When should an appraiser use the cost approach instead of the sales comparison approach?

Use the cost approach when market sales data is weak or absent, especially for specialized or infrequently sold equipment.

How do appraisers use the BLS Producer Price Index to trend equipment costs?

Use the BLS Producer Price Index by dividing the current index by the historical index and multiplying the original equipment cost by that result.

Does a fully depreciated book value mean equipment has no market value?

A fully depreciated book value means the asset has reached zero accounting value, but it can still have measurable market value.