Heavy Equipment Appraisal Guide

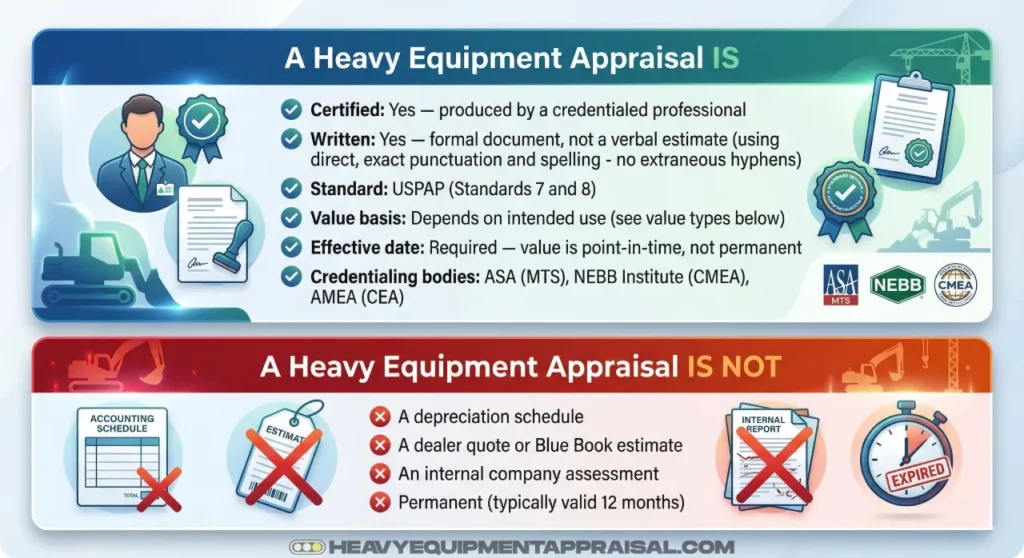

A heavy equipment appraisal is a certified, written opinion of the value of machinery used in construction, agriculture, transportation, or industry, produced by a credentialed professional following the Uniform Standards of Professional Appraisal Practice (USPAP).

The value an appraiser reports depends on the purpose: a lender sizing loan collateral needs a different value standard than an estate attorney dividing assets or an insurer settling a loss.

This heavy equipment appraisal guide covers what an appraisal is, which value type applies to each situation, what USPAP compliance requires, and how to evaluate an appraiser’s credentials.

What Is a Heavy Equipment Appraisal?

A heavy equipment appraisal is a formal, documented opinion of value for machinery and equipment assets. It is produced by a qualified appraiser, effective as of a specific date, and structured to meet the requirements of the intended user.

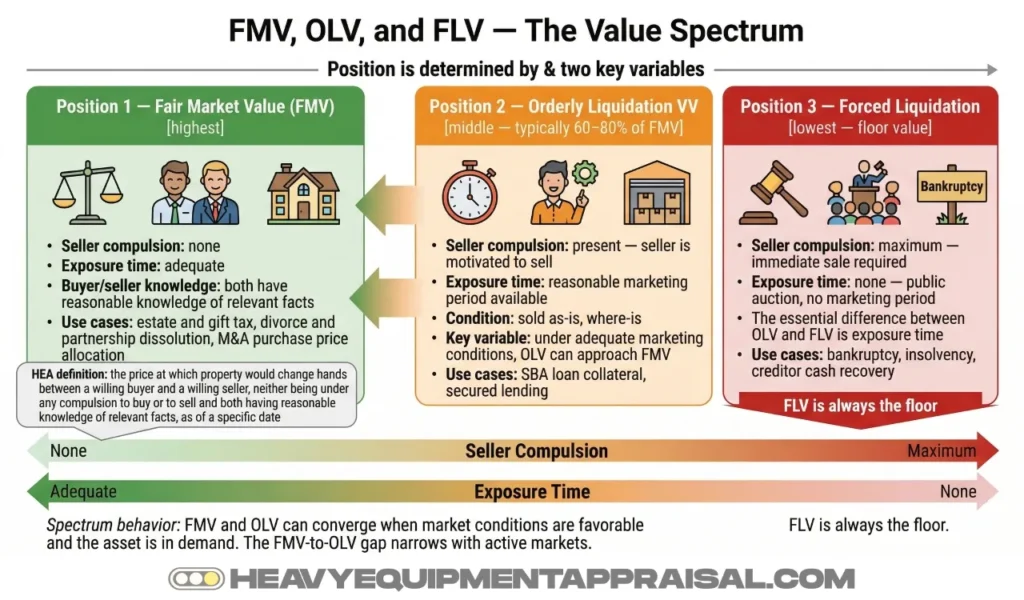

We define the underlying standard of value (fair market value (FMV)) as “an opinion expressed in terms of money, at which the property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or to sell and both having reasonable knowledge of relevant facts, as of a specific date.”

Every other value type used in equipment appraisal is a modification of that baseline, adjusted for the circumstances of the transaction.

Equipment appraisals cover construction machinery (excavators, motor graders, crawler dozers), agricultural equipment, industrial machinery, transportation fleets, and manufacturing assets. The clients are typically business owners, lenders, attorneys, accountants, and insurers, each with a different intended use for the resulting report.

The effective date matters as much as the value itself. Equipment markets shift with economic conditions, auction trends, and supply cycles. An appraisal is a snapshot, not a permanent record, which is why the SBA, IRS, and most lenders require appraisals to be current, typically within 12 months of the transaction.

Why You Need One: Common Use Cases

Equipment appraisals are required across a wide range of business and legal situations, and each one calls for a specific type of value, which is why the purpose must be defined before the appraiser begins work.

According to ASA’s Valuing Machinery and Equipment, common appraisal purposes include: financing and collateral support, insurance coverage and loss settlement, mergers and acquisitions, purchase price allocation, bankruptcy and insolvency proceedings, dissolutions of partnerships and marriages, estate and gift tax filings, income and property tax purposes, litigation support, and condemnation.

In practice, these fall into 4 categories:

Financing: Lenders require an appraisal to size collateral. Under SBA SOP 50 10 7.1, used machinery valued with a certified orderly liquidation value appraisal can support up to 80% of appraised value toward the fully-secured calculation, compared to 50% of net book value without one.

Legal and tax proceedings: Estate settlements, divorce, and gift tax filings generally require fair market value. Bankruptcy appraisals typically require a liquidation standard because creditors want to know cash recovery, not going-concern value.

Insurance: Coverage appraisals establish replacement cost new or actual cash value depending on the policy structure.

Sale and M&A: Purchase price allocations under IRS and accounting standards (ASC 805) are generally done at FMV or fair value.

The Three Approaches to Value

Equipment appraisers use 3 methodological frameworks to develop an opinion of value: the sales comparison approach, the cost approach, and the income approach. USPAP Standards Rule 7-4 requires appraisers to consider all 3 for every assignment and apply whichever are relevant to the facts at hand.

The sales comparison approach establishes value by analyzing recent sales of comparable equipment, matching the subject asset by make, model, age, condition, and hours, then adjusting for differences. It is the most commonly applied approach for standard construction and agricultural equipment because auction results and dealer transactions generate sufficient comparable data.

The cost approach estimates value by calculating what it would cost to replace the equipment with a new equivalent, then subtracting for physical deterioration, functional obsolescence, and economic obsolescence. It is most reliable for specialized or custom machinery with few market comparables.

The income approach values equipment based on the income it is expected to generate over its remaining useful life, using direct capitalization or discounted cash flow analysis. It applies when equipment is directly tied to a measurable revenue stream and market data alone is insufficient to support a value conclusion.

An appraiser who applies only 1 approach without documenting why the others don’t apply is not meeting USPAP standards. That matters when the report is reviewed by a lender, the IRS, or a court.

Types of Value: FMV, OLV, and FLV (and When Each Applies)

The value type an appraiser reports is not a choice the appraiser makes unilaterally. It is determined by the intended use of the report, and selecting the wrong one produces a number that fails the purpose entirely.

Fair market value (FMV) is the foundational standard: the price at which property would change hands between a willing buyer and a willing seller, neither under compulsion, both with reasonable knowledge of the facts. It assumes an open market, adequate exposure time, and no external pressure on either party. Estate and gift tax filings, divorce and partnership dissolutions, and most purchase price allocations default to FMV because those situations require an arm’s-length, market-reflective number.

Orderly liquidation value (OLV) assumes the seller is compelled to sell but has a reasonable period of time to find a buyer. The equipment is sold as-is, where-is. Under adequate marketing conditions, OLV can approach FMV. The gap narrows when the market is active and the asset is in demand. Lenders and SBA financing scenarios typically require OLV because it reflects recoverable collateral value, not going-concern value.

Forced liquidation value (FLV) assumes immediacy. The seller must convert the asset to cash at a public auction with no time for market exposure. The essential difference between OLV and FLV is exposure time, and that difference typically translates to a meaningfully lower number. FLV is the standard in bankruptcy proceedings where creditors need to know the floor.

| Situation | Value Standard |

|---|---|

| SBA loan collateral | OLV |

| Bankruptcy / insolvency | FLV |

| Estate or gift tax | FMV |

| Divorce / dissolution | FMV |

| Insurance coverage | Replacement cost new or actual cash value |

| M&A / purchase price allocation | FMV or fair value (ASC 805) |

For a detailed comparison of when each standard applies, see the full breakdown of FMV, OLV, and FLV.

USPAP: The Standard Every Appraisal Must Meet

USPAP is the national framework governing how appraisals are developed and reported. Established by the Appraisal Foundation and updated every 2 years, it sets the minimum requirements that any defensible equipment appraisal must satisfy.

For machinery and equipment appraisals, 2 standards apply:

Standard 7 governs development: it defines what the appraiser must do during the assignment, including identifying the client and all intended users, defining the value type, establishing the effective date, and considering all applicable approaches to value.

Standard 8 governs reporting: it defines what the written report must contain. A key requirement of Standard 8 is that "an appraiser must communicate each analysis, opinion, and conclusion in a manner that is not misleading."

That requirement has practical consequences.

A USPAP-compliant report must identify the client, state the value type and its definition, describe the property being appraised, document the methodology applied, and include the appraiser's signed certification. A report that omits those elements will not hold up to scrutiny from an SBA lender, the IRS, or opposing counsel in litigation.

But USPAP compliance is NOT self-certifying.

An appraiser who claims USPAP compliance should be able to identify which standards apply to the assignment and explain how their report satisfies them.

For a full treatment of what USPAP requires in equipment appraisal contexts, see the dedicated resource on USPAP standards for equipment appraisal.

What Credentials to Look For in an Appraiser

A qualified equipment appraiser holds a designation from a recognized credentialing body, has passed a competency examination, and produces reports that comply with USPAP. Without that baseline, the appraiser's opinion may not be accepted by a lender, the IRS, or a court.

3 organizations issue the primary designations for machinery and equipment appraisers, and the SBA recognizes all 3 as sources of qualified appraisers for equipment collateral assignments:

| Organization | Designation | Minimum Requirements | SBA Recognized |

|---|---|---|---|

| American Society of Appraisers (ASA) | AM (Accredited Member) | ASA MTS curriculum + examination + 2 years relevant experience | Yes |

| American Society of Appraisers (ASA) | ASA (senior designation) | 5 years full-time appraisal experience + peer-reviewed demonstration report + continuing education | Yes |

| NEBB Institute | CMEA (Certified Machinery and Equipment Appraiser) | 2-day training class + 100-question examination + demonstration appraisal report + ethics agreement | Yes |

| Association of Machinery and Equipment Appraisers (AMEA) | CEA (Certified Equipment Appraiser) | AMEA education and examination requirements | Yes |

An appraiser who holds one of these designations has met education, examination, and ethics requirements set by a third party. An auctioneer, dealer, or internal company employee appraising equipment they have a financial interest in does not meet the independence standard that USPAP and most lenders require. For a full breakdown of what each designation requires, see the resource on appraiser credentials and designations.

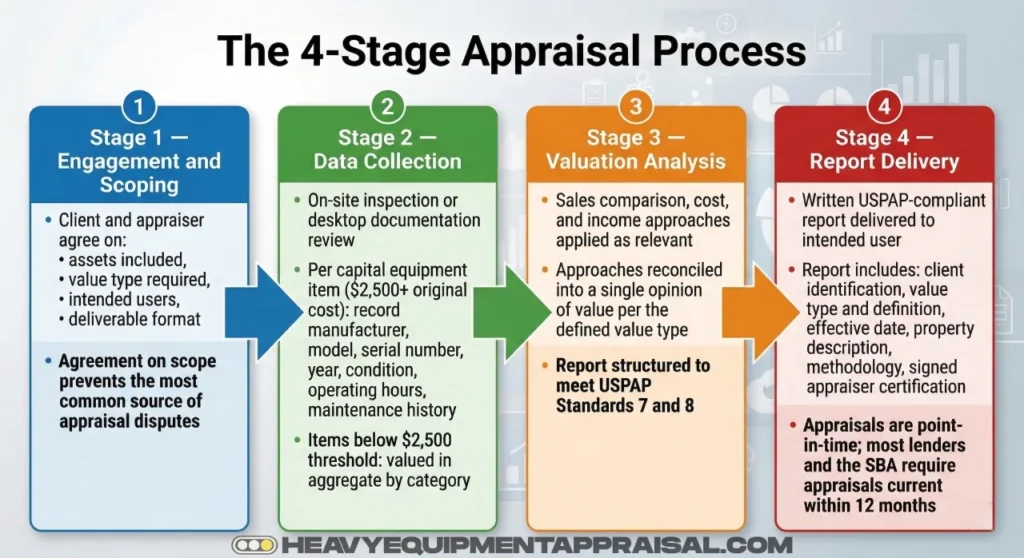

How the Appraisal Process Works

A machinery and equipment appraisal moves through 4 stages: engagement and scoping, on-site data collection, valuation analysis, and report delivery.

The engagement stage defines the scope of work before any inspection occurs. The appraiser and client agree on which assets are included, which value type is required, who the intended users are, and what the deliverable will be. That agreement prevents the most common source of appraisal disputes: a client who expected one thing and received another.

Data collection is where most of the appraisal's accuracy is built or lost. For each piece of capital equipment (assets with an original cost new of $2,500 or more), the appraiser records manufacturer, model, serial number, year, condition, operating hours, and maintenance history. Items below the $2,500 threshold are valued in aggregate by category rather than individually. Having maintenance records and operator access ready before the appraiser arrives reduces both the time on-site and the likelihood of condition disputes later.

Valuation analysis applies the sales comparison, cost, and income approaches as relevant, then reconciles them into a final opinion of value per the defined value type. The report is then structured to meet USPAP Standards 7 and 8.

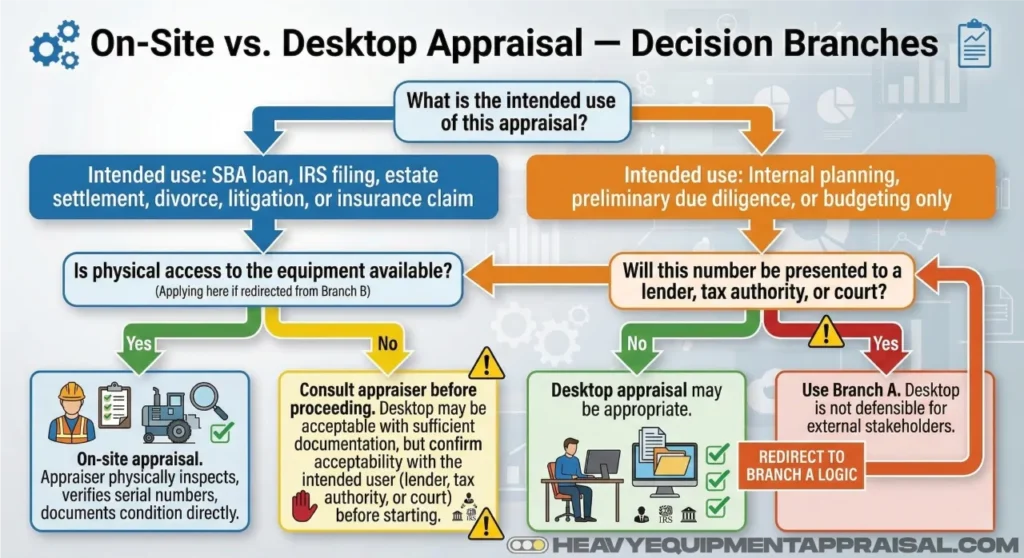

Whether the inspection happens on-site or via desktop review changes what the appraiser can certify.

For a full breakdown of what to prepare and expect, see the step-by-step appraisal process guide and the documents needed for an appraisal resource.

Book Value Is Not Market Value

A piece of construction equipment that appears at $0 on a company's balance sheet can still command six figures at auction. Book value and market value are different calculations serving different purposes, and confusing them is one of the most common and costly errors in equipment-related financial decisions.

Net book value is an accounting figure derived by subtracting accumulated depreciation from the asset's original cost. Under the IRS Modified Accelerated Cost Recovery System (MACRS), most equipment is depreciated over 5 to 7 years depending on classification, per IRS Publication 946, Table B-1. Once that recovery period ends, the book value reaches zero, regardless of the asset's actual condition or market demand.

Appraisal depreciation measures something fundamentally different: the loss in value relative to a new equivalent, caused by physical deterioration, functional obsolescence, and economic obsolescence. As ASA's Valuing Machinery and Equipment states directly, "accounting depreciation is a mathematical convention for recovering an asset's cost," while appraisal depreciation measures actual value inferiority. The same manual notes that net book value "is typically derived through a cost allocation process, not a valuation process" and that it approximates market value only by chance.

A lender who sizes a loan against a depreciation schedule instead of a certified appraisal is making a collateral decision based on accounting convention, not market reality.

Getting the Right Appraisal

The cost of a heavy equipment appraisal depends on the number of assets, the inspection method, the value types required, and how the report will be used. A litigation-grade on-site appraisal costs more than a desktop review for internal planning purposes. For a full breakdown of what drives appraisal fees and what to expect, see the resource on equipment appraisal cost.

The inspection method matters beyond cost. An on-site appraisal allows the appraiser to physically inspect condition, verify serial numbers, and document the asset directly. A desktop appraisal relies on provided documentation and market data without a site visit. Whether a desktop report will satisfy the intended user depends on the assignment's scope and the standard of value required.

The dedicated comparison of desktop vs. on-site equipment appraisal covers when each is defensible.

A certified appraisal from a credentialed appraiser, scoped to the right value type, produced under USPAP Standards 7 and 8, is a document that holds up. It supports a loan, satisfies a tax authority, withstands a legal challenge, and gives a buyer or seller a defensible number to negotiate from. The alternative (a depreciation schedule, a dealer quote, or an online pricing tool) produces a figure that none of those parties will accept.

FAQ

What is the difference between a heavy equipment appraisal and a Blue Book value?

The main difference between a heavy equipment appraisal and a Blue Book value is that an appraisal is a professional opinion of value for a specific machine, while a Blue Book value is a general pricing estimate based on market data. An appraisal considers condition, hours, attachments, location, and demand. Blue Book values provide a benchmark, not a certified valuation.

How long is a certified heavy equipment appraisal valid?

A certified heavy equipment appraisal is valid only as of its effective date. Most lenders, courts, insurers, and tax authorities treat an appraisal as current for 30 to 180 days, depending on market conditions, equipment type, and purpose. Fast-moving markets, high-use machines, or liquidation cases often require a newer appraisal within 30 to 90 days.

What does USPAP-compliant mean for an equipment appraisal?

USPAP-compliant means the equipment appraisal follows the Uniform Standards of Professional Appraisal Practice. It requires the appraiser to define the appraisal’s purpose, scope, effective date, and value standard, then support the opinion with credible market data, analysis, and reporting. A USPAP-compliant appraisal also requires independence, impartiality, and proper documentation.

When is a certified appraisal required for an SBA equipment loan?

A certified appraisal is generally required for an SBA equipment loan when the lender cannot support the equipment’s value with reliable market data, invoices, or orderly liquidation evidence. In general SBA practice, appraisals become more likely for used equipment, specialized equipment, large-dollar collateral, or liquidation-value analysis. The lender’s credit policy and the current SBA SOP control the final requirement.

Can net book value be used instead of an appraisal for loan collateral?

Net book value can be used instead of an appraisal for loan collateral only in limited cases. Lenders may accept net book value for newer equipment, strong financial borrowers, or smaller loans when purchase records and depreciation schedules are reliable. Most lenders require an appraisal when equipment is used, specialized, high-value, or difficult to price in the secondary market.

What is the difference between orderly liquidation value and forced liquidation value?

The main difference between orderly liquidation value and forced liquidation value is that orderly liquidation value assumes a marketed sale over 60 to 180 days, while forced liquidation value assumes an immediate sale under distress and produces a lower value.